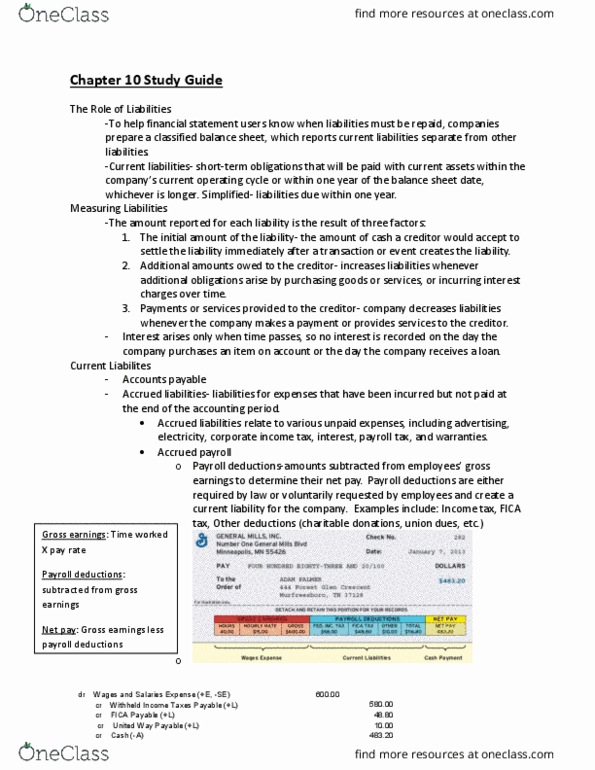

ACC 377 Lecture Notes - Lecture 2: Deferred Tax, Pay-As-You-Earn Tax

Quarterly - with two installments paid in year and two after. Thus creating liability

When CT has been over or under estimated, what adjustment do you make in the following year?

Take through P/L -

Dr P/L Taxation

Cr Bank

Dr Bank

Cr P/L Taxation

Exam tip - Often don't include bank but incorrectly debit/credit payable. Just Replace bank with payable.

When correcting PY Tax, don't forget to workout and Jr CY

...

If there is a tax loss and company makes claim

Dr Other Receivables

Cr P/L Taxation

What is income tax?

When a company pays bond, loan, royalties interest to an individual, they must deduct that persons tax

at source. Like PAYE.

What are the two main journals for for recording income tax?

Interest paid-

Dr P/L Finance Costs (gross)

Cr Bank (Net)

Cr Current tax payable (Tax withheld)

find more resources at oneclass.com

find more resources at oneclass.com

IT Paid-

Dr Current Tax Payable

Cr Bank

Deferred Tax - Pension liability

Pension liability @ YE £300,000.

This means they will make a future contribution to meet liability. This contribution is tax deductible,

therefore entity should recognise asset!

(300,000x17%) 51,000

Dr Deferred Tax Asset

Cr P/L - taxation

Deferred Tax - Gained rolled over

£2m Taxable gain was rolled over to another asset. This gain isn't realised until 2 years down the line.

(2m x 17%) 340,000

Dr P/L Taxation

Cr Deferred Tax Liability

Temporary differences

Difference between carry amount in SoFP and tax base.

Taxable TD - Rolled over gain

Deductible TD - Pension Liability

Deductible Temporary Difference - Assets

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Quarterly - with two installments paid in year and two after. Exam tip - often don"t include bank but incorrectly debit/credit payable. When correcting py tax, don"t forget to workout and jr cy. If there is a tax loss and company makes claim. When a company pays bond, loan, royalties interest to an individual, they must deduct that persons tax at source. This means they will make a future contribution to meet liability. This contribution is tax deductible, therefore entity should recognise asset! (300,000x17%) 51,000. 2m taxable gain was rolled over to another asset. This gain isn"t realised until 2 years down the line. (2m x 17%) 340,000. Difference between carry amount in sofp and tax base. Twdv exceeds nbv, deductible td and deferred tax asset. Nbv exceed twdv, taxable td and deferred tax liability. Td exam tip - you may have to adjust for additions, dep, and capital allowances in exam.