ACC 344 Lecture Notes - Lecture 2: Adjusted Gross Income, Health Savings Account, Standard Deduction

1

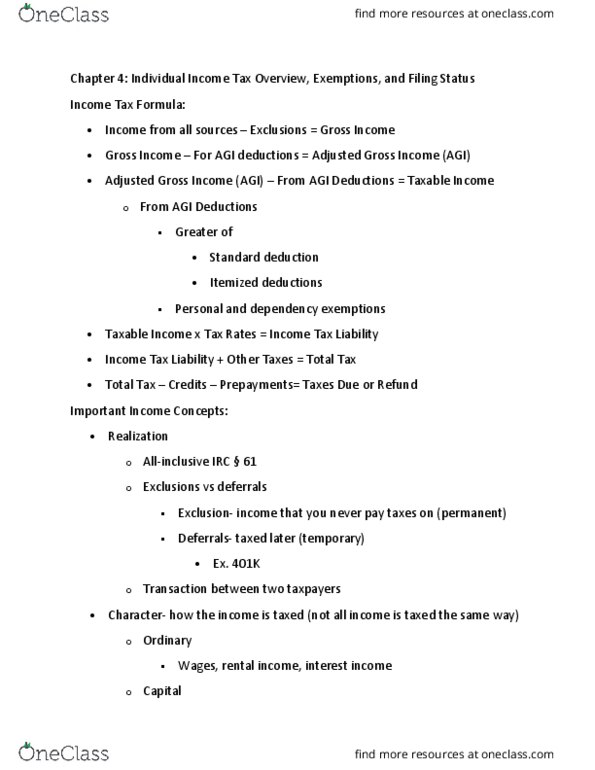

Tax formula for individuals: Table I: 2-1 on page 2-2

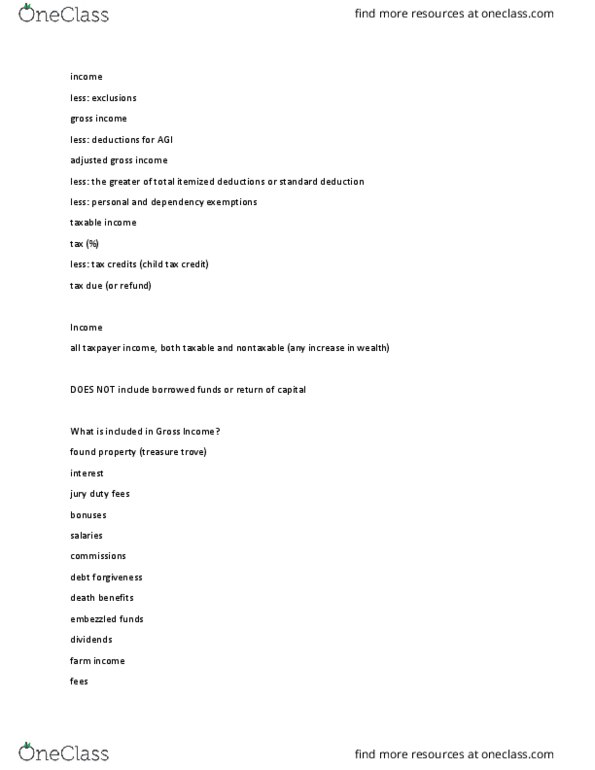

Income

Ioe, roadl oeied, iludes all the tapaer’s ioe, oth taale ad

nontaxable.

• It is not specifically defined in the tax code

• It does not include a return of capital or receipt of borrowed funds

o Example: Bob sells a piece of property for $1,000. He has a cost basis of

$700. Bob will include $300, not $1,000, in total income.

Income (from all sources) $xx,xxx

Less: Exclusions (x,xxx)

Gross income $xx,xxx

Less: Certain deductions for AGI (x,xxx)

Adjusted Gross Income $xx,xxx

Less: The greater of:

Itemized deductions, or

The standard deduction (x,xxx)

Less: Personal and dependency exemptions (x,xxx)

Taxable income $xx,xxx

Tax on taxable income (see Tax Rate

Schedules)

$ x,xxx

Less: Tax credits (including Federal income

tax withheld and other prepayments of

Federal income taxes)

(xxx)

Tax due (or refund) $ xxx

find more resources at oneclass.com

find more resources at oneclass.com

2

Exclusions

Not all income is taxable. A bunch of stuff does not count.

Listed in Table I: 2-2 on page 2-3. These do NOT have to be disclosed on the tax

return.

Gifts Life Insurance Welfare Certain

Scholarships

Certain Pmts

for Injury

Certain

Employee

Benefits

Certain

Foreign

Income

Tax-Exempt

Interest

Series EE Bond

Interest

Leasehold

Improvements

Meritorious

Achievement

Awards

Certain

Divorce

Payments

Gain from Sale

of Home

Roth IRA

Distributions SS Benefits

find more resources at oneclass.com

find more resources at oneclass.com

3

Gross Income = Income – Exclusions

Stuff that must be included on the tax return:

Section 61 of the IRS code has a partial list of what counts.

Therefore, even stuff not on the list has to count.

Example: Income from illegal activities is not on the list, but needs to go on the tax return

Table I: 2-3 on page 2-4 lists what counts

Life insurance is on the exclusion and inclusion list:

In general, proceeds received from a policy due to the death of the insured do not count.

However, if you sell the life insurance policy before death, then those proceeds will be

taxable.

Wages Business

Gross Inc.

Gains from

Property

Sales

Interest

Rents Royalties Dividends Alimony

Annuities

Life

Insurance

Proceeds

Pensions COD Income

P’ship

Income IRD Trust/Estate

Income

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Tax formula for individuals: table i: 2-1 on page 2-2. Less: tax credits (including federal income tax withheld and other prepayments of. I(cid:374)(cid:272)o(cid:373)e, (cid:271)roadl(cid:455) (cid:272)o(cid:374)(cid:272)ei(cid:448)ed, i(cid:374)(cid:272)ludes all the ta(cid:454)pa(cid:455)er"s i(cid:374)(cid:272)o(cid:373)e, (cid:271)oth ta(cid:454)a(cid:271)le a(cid:374)d nontaxable. (xxx) $ x,xxx: it is not specifically defined in the tax code, it does not include a return of capital or receipt of borrowed funds, example: bob sells a piece of property for ,000. Bob will include , not ,000, in total income. Listed in table i: 2-2 on page 2-3. These do not have to be disclosed on the tax return. Stuff that must be included on the tax return: Section 61 of the irs code has a partial list of what counts. Therefore, even stuff not on the list has to count. Example: income from illegal activities is not on the list, but needs to go on the tax return. Table i: 2-3 on page 2-4 lists what counts.