AC 211 Lecture 11: Fraud, Internal Control, and Cash (Part 3)

148 views2 pages

Document Summary

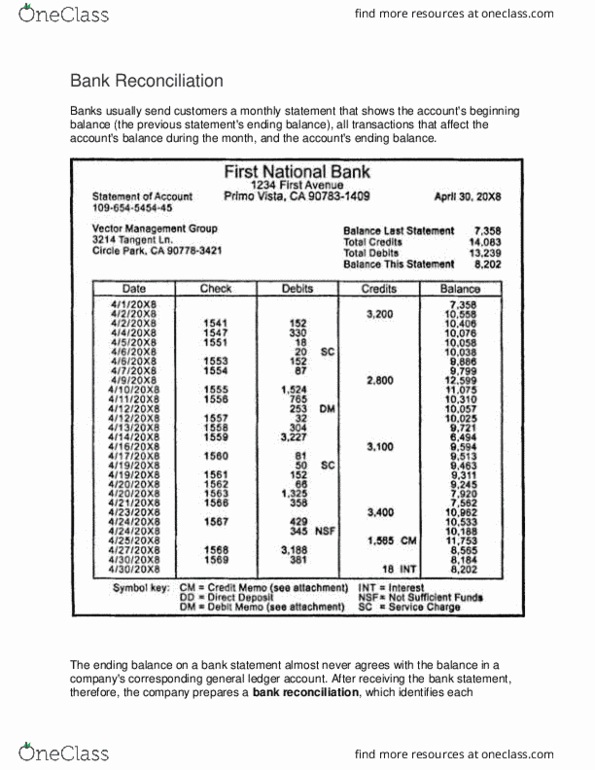

Bank reconciliation: process of using both the bank statement and the cash accounts of a business to determine the appropriate amount of cash in a bank account, after taking into consideration delays or errors in processing cash transactions. Key internal control because it provides independent verification of all cash transactions that the bank has processed for the company. Check is cleared when financial institution contacts the check writer"s bank, which in turn withdraws the amount of the check from the check writer"s account and reports it as a deduction on the bank statement. Deposits are listed on the bank statement in the order in which the bank processes them. Other transactions the bank statement is presented from the bank"s point of view. Banks typically explain the reasons for these increases (credits) and decreases (debits) with symbols or in a short memo, appropriately called a credit memo or debit memo.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers

Related Documents

Related Questions

Problem 7-5A (Part Level Submission)

Ivanhoe Company of Emporia, Kansas, spreads herbicides andapplies liquid fertilizer for local farmers. On May 31, 2017, thecompanyâs Cash account per its general ledger showed a balance of$6,858.90.

The bank statement from Emporia State Bank on that date showed thefollowing balance.

EMPORIA STATE BANK | ||||

|---|---|---|---|---|

Checks and Debits | Deposits and Credits | Daily Balance | ||

| XXX | XXX | 5-31 7,088.00 | ||

A comparison of the details on the bank statement with the detailsin the Cash account revealed the following facts.

| 1. | The statement included a debit memo of $64.00 for the printingof additional company checks. | |

| 2. | Cash sales of $907.15 on May 12 were deposited in the bank. Thecash receipts journal entry and the deposit slip were incorrectlymade for $957.15. The bank credited Ivanhoe Company for the correctamount. | |

| 3. | Outstanding checks at May 31 totaled $267.25, and deposits intransit were $1,904.15. | |

| 4. | On May 18, the company issued check No. 1181 for $686.00 to H.Moses, on account. The check, which cleared the bank in May, wasincorrectly journalized and posted by Ivanhoe Company for$668.00. | |

| 5. | A $2,834.00 note receivable was collected by the bank forIvanhoe Company on May 31 through electronic funds transfer. | |

| 6. | Included with the canceled checks was a check issued by TominsCompany to C. Pernod for $336.00 that was incorrectly charged toIvanhoe Company by the bank. | |

| 7. | On May 31, the bank statement showed an NSF charge of $500.00for a check issued by Sara Ballard, a customer, to Ivanhoe Companyon account. |

a.)Prepare the bank reconciliation at May 31, 2017

b.) Prepare the necessary adjusting entries for Blossom Companyat May 31, 2017. (Credit account titles areautomatically indented when amount is entered. Do not indentmanually.)

| The following Bankinformation is available for Cooter's Garage for March, 2002 | ||||||

| BANK STATEMENT | ||||||

| HAZARD COUNTY STATE BANK | ||||||

| 215 Main Street | ||||||

| Hazard, GA 30321 | ||||||

| Cooter's Garage | Account Number | |||||

| 629 Main Street | 62-00062 | |||||

| Hazard, GA 30321 | March 31, 2002 | |||||

| BeginningBalance 3/1/2002 | $ 15,000.00 | |||||

| TotalDeposits and Other Credits | 7,050.00 | |||||

| Total Checksand Other Debits | 6,005.00 | |||||

| EndingBalance 3/31/2002 | $ 16,045.00 | |||||

| Checks and Debits | Deposits and Credits | |||||

| Date | Check No. | Amount of Check | Date | |||

| 03/01/02 | 1462 | $ 1,163.00 | 3/1/2002 | $ 1,000.00 | ||

| 03/05/02 | 1463 | 62.00 | 3/2/2002 | 1,340.00 | ||

| 03/06/02 | 1464 | 1,235.00 | 3/6/2002 | 210.00 | ||

| 03/09/02 | 1465 | 750.00 | 3/12/2002 | 1,940.00 | ||

| 03/10/02 | 1466 | 1,111.00 | 3/17/2002 | 855.00 | ||

| 03/14/02 | 1467 | 964.00 | 3/22/2002 | 1,480.00 | ||

| 03/19/02 | Debit Memo | 20.00 | Credit Memo | 225.00 | ||

| 03/28/02 | 1468 | 700.00 | ||||

| The following is a list ofchecks and deposits recorded on the books of Cooter's Garagefor | ||||||

| March, 2002 | ||||||

| Date | Check Number | Amount of Check | Date | Amount of Deposit | ||

| 3/1/2002 | 1463 | $ 62.00 | 3/1/2002 | $ 1,340.00 | ||

| 3/5/2002 | 1464 | 1,235.00 | 3/5/2002 | 210.00 | ||

| 3/6/2002 | 1465 | 750.00 | ||||

| 3/9/2002 | 1466 | 1,111.00 | 3/10/2002 | 1,940.00 | ||

| 3/10/2002 | 1467 | 964.00 | ||||

| 3/14/2002 | 1468 | 70.00 | 3/16/2002 | 855.00 | ||

| 3/19/2002 | 1469 | 1,500.00 | 3/19/2002 | 1,480.00 | ||

| 3/28/2002 | 1470 | 102.00 | 3/29/2002 | 1,500.00 | ||

| Other Information | ||||||

| 1 | Check no. 1462 was outstanding from February.(Hint: Not Applicable to current month.) | |||||

| 2 | A credit memo for collection of accounts receivablewas included in the bank statement. | |||||

| 3 | All checks were paid by the bank at the correctamount. | |||||

| 4 | The bank statement included a debit memo forservice charges. | |||||

| 5 | The February 28 bank reconciliation showed adeposit in transit of $1,000. | |||||

| 6 | Check no. 1468 was for the purchase ofequipment. | |||||

| 7 | The unadjusted Cash account balance at March 31 was$16,368. | |||||

| Required | ||||||

| a. | Prepare the bank reconciliation for Cooters Garageat the end of March. | |||||

| b. | Record in general journal form any necessaryentries to the Cash account to adjust it to | |||||

| the true cash balance. | ||||||

| COOTER'S GARAGE TAccounts | ||||||||||

| Cash | COOTER'S BANK RECONCILIATION | |||||||||

| Ending Bank Balance | ||||||||||

| Add: | ||||||||||

| Less: | ||||||||||

| True Cash Balance | - | |||||||||

| Accounts Receivable | ||||||||||

| Book Balance | ||||||||||

| Add: | ||||||||||

| Less: | ||||||||||

| Bank Charges | ||||||||||

| True Cash Balance | - | |||||||||

| Equipment Expense | ||||||||||

| Horizontal Model | ||||||||||

| Cash | Acct Rec | Bank Chg | Equip Exp | |||||||