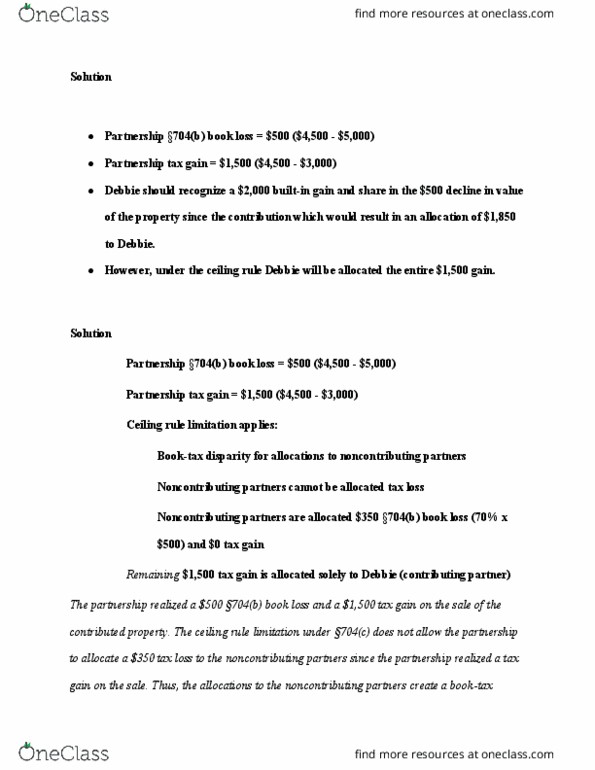

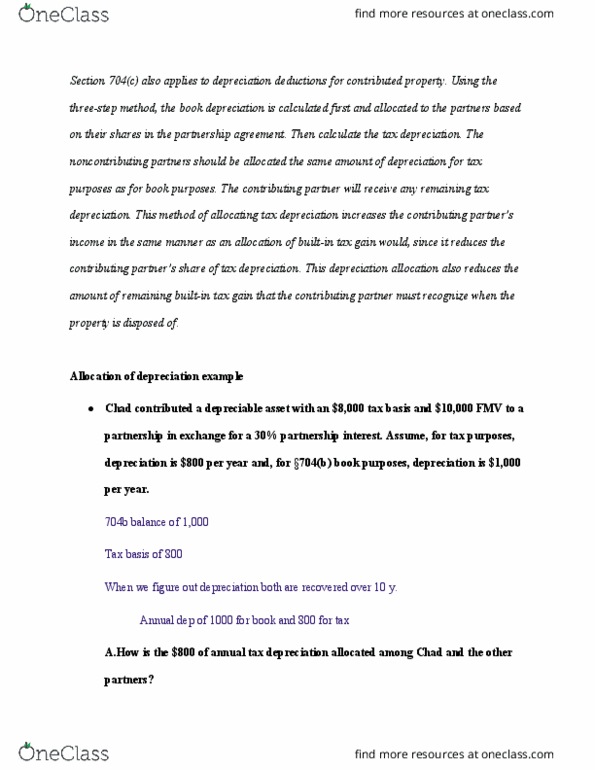

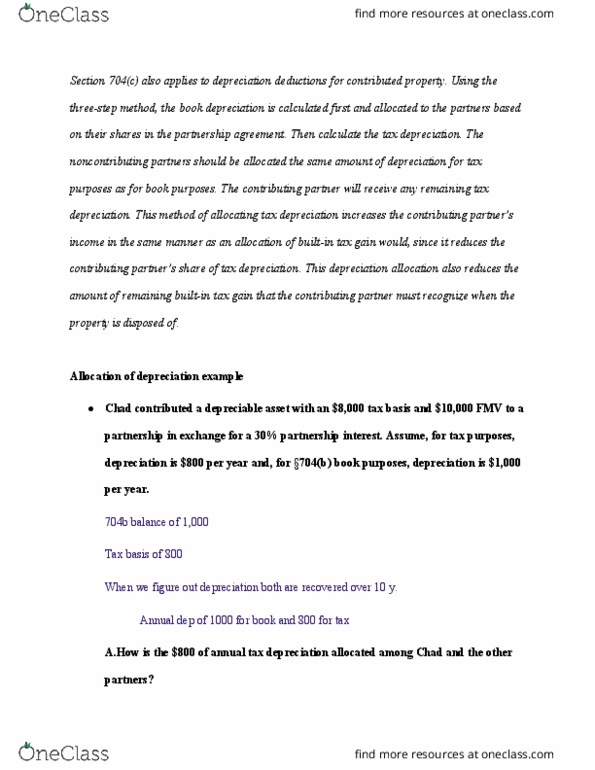

TAX 9900 Lecture 39: class39

Document Summary

Get access

Related Documents

Related Questions

Bryan and Cody each contributed $120,000 to the newly formed BC Partnership in exchange for a 50% interest. The partnership used the available funds to acquire equipment costing $200,000 and to fund current operating expenses. The partnership agreement provides that depreciation will be allocated 80% to Bryan and 20% to Cody. All other items of income and loss will be allocated equally between the partners.

Upon liquidation of the partnership, property will be distributed to the partners in accordance with their capital account balances. Any partner with a negative capital account must contribute cash in the amount of the negative balance to restore the capital account to $0.

In its first year, the partnership reported an ordinary loss (before depreciation) of $80,000 and depreciation expense of $36,000. In its second year, the partnership reported $40,000 of income from operations (before depreciation), and it reported depreciation expense of $57,600.

a. Calculate the partners' bases in their partnership interests at the end of the first and second tax years.

|

Are any losses suspended for either partner?

No/Yes

b. Does the allocation provided in the partnership agreement have an "economic effect"?

No/Yes , because (1) gains, income, loss, etc., allocations are/are not reflected in capital account balances, (2) liquidating distributions are in accordance with average/beginning/end capital account balances, and (3) deficit capital accounts/outstanding loan balances must be restored.