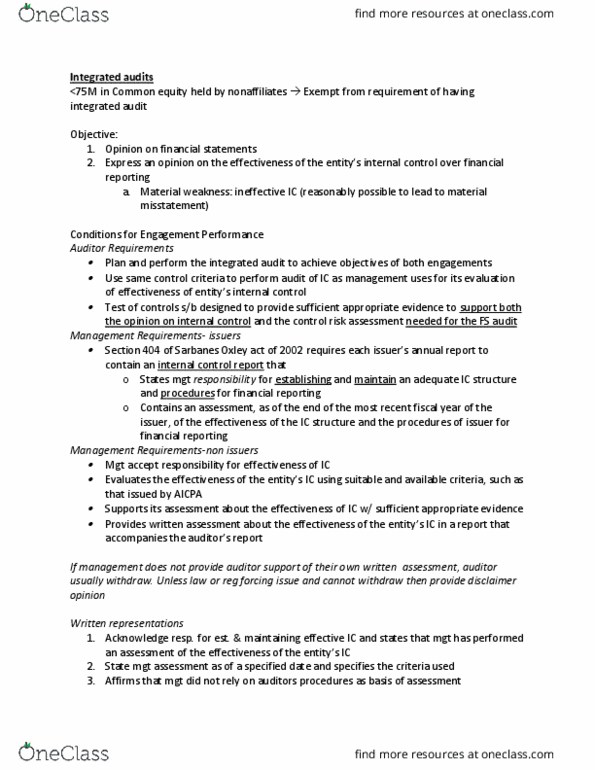

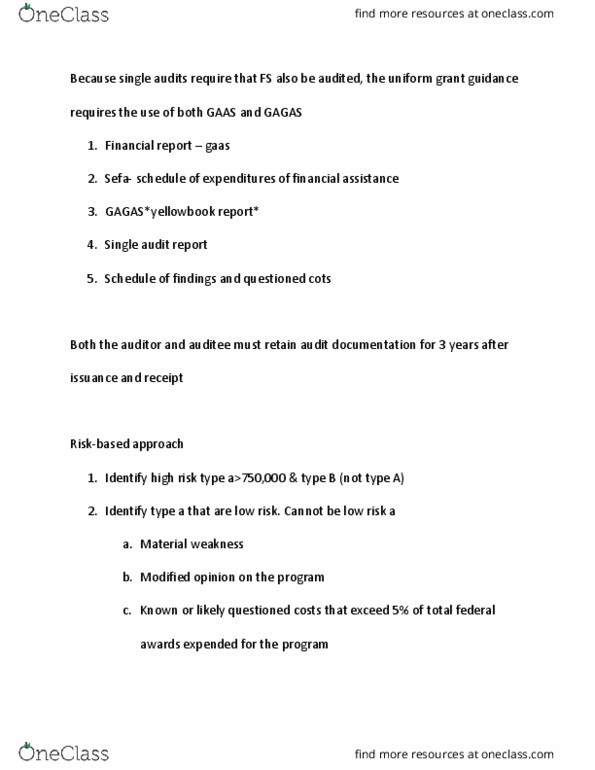

You are an audit accountant and you boss asks you the followingquestions

answer For financial audits, generally accepted governmentauditing standards (GAGAS) incorporate AICPA standards. GAGASprescribe additional requirements for reporting on Laws,Regulations, Reporting on Contracts, and Grants InternalControl

Yes No

No No

No Yes

Yes Yes

When reporting on an entityâs internal control over financialreporting in compliance with generally accepted government auditingstandards, an auditor should issue a written report that includesa

Statement of positive assurance that the results of testsindicate that internal control either can, or cannot, be relied onto reduce control risk to an acceptable level.

Statement of negative assurance that nothing came to theauditorâs attention that caused the auditor to believe significantdeficiencies were present.

Description of the scope of the auditorâs testing of internalcontrol.

Description of the material weaknesses and the strengths thatthe auditor can rely on in reducing the extent of substantivetesting.

Reporting standards for financial audits under GovernmentAuditing Standards differ from reporting standards undergenerally accepted auditing standards in that GovernmentAuditing Standards require the auditor to

Present the results of the auditorâs tests of economy andefficiency regarding the use of the entityâs resources.

Describe the scope of the auditorâs tests of compliance withlaws and regulations.

Provide negative assurance that the auditor discoveredno transactions that were indicative of illegalacts.

Provide positive assurance that the entityâs audit committee isadequately informed about the effects of any illegal acts.

An auditor determines that a client who received a federal grantfraudulently reported information to the federal government. Theclientâs management refuses to acknowledge the fraud. Which of thefollowing parties should the auditor contact first?

The recipients of the clientâs services.

The state attorney generalâs office.

The agency that provided the grant.

The state accountancy board.