BUS 295 Lecture Notes - Lecture 18: Capital Asset Pricing Model, Market Risk, Systematic Risk

Document Summary

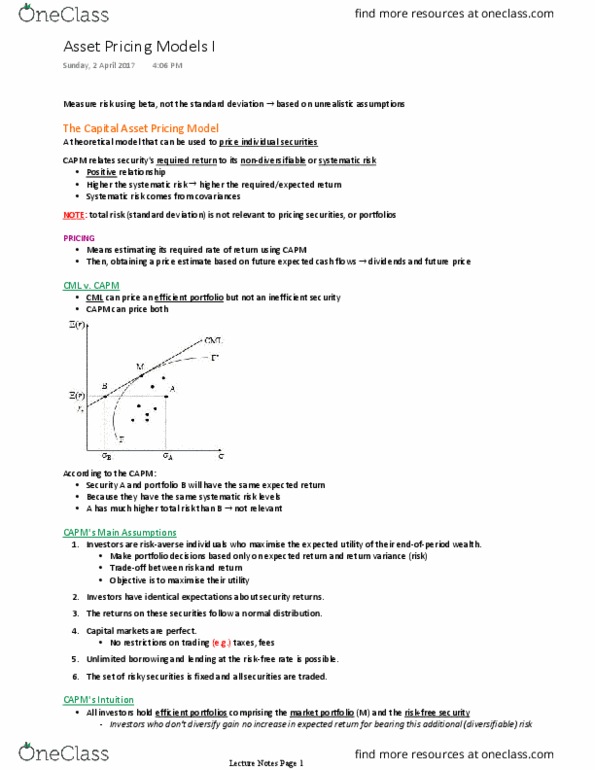

The of a portfolio is the weighted average of the "s of the individual assets in the portfolio. You collect or compute the following information for a firm. The historical market risk premium, calculated over the last 15 years, is 7%. The company"s next dividend is expected to be sh. 10. Analysts" consensus is that the dividends will grow at a rate of 6% per year forever. The firm"s stock returns have a correlation with the market of around 0. 5, while the standard deviation of the market is 0. 1, and the standard deviation of the firm is 0. 25. Higher risk (beta) should be associated with higher return. No added return for bearing non-market risk in standard capm, intercept should be risk free rate. Formulated in expected returns, all we observe are realized returns. Results are important for the portfolio process even if capm isn"t true. Risk and return appear to be linearly related when risk is defined as systematic risk.