ECON 3411 Lecture Notes - Lecture 35: Perfect Competition, Marginal Cost, Takers

19 Jan 2018

School

Department

Course

Professor

Document Summary

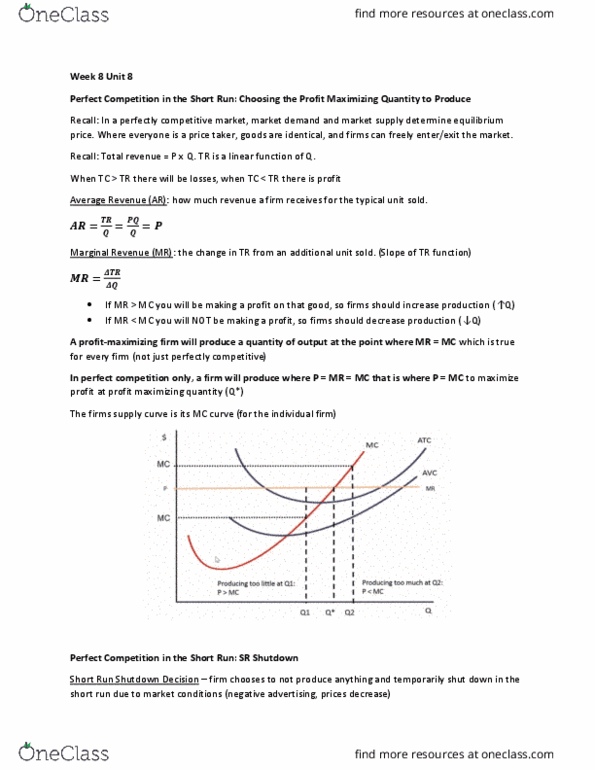

Topic: firm"s short-run supply: a profit-maximizing firm should continue to operate (sustain short-run losses) if its operating loss is less than its fixed costs. Operating results in a smaller loss than ceasing operations: decision rule: A firm should shut down when p < min avc. Co(cid:374)ti(cid:374)ue operati(cid:374)g as lo(cid:374)g as p (cid:373)i(cid:374) avc. Firm"s short-run supply curve: mc above min avc. Fir(cid:373)"s hort-run supply curve: the short-run supply curve for a perfectly competitive firm is its marginal cost curve above the minimum point on the curve. The (cid:373)arket supply curve is the su(cid:373)(cid:373)atio(cid:374) of each i(cid:374)dividual fir(cid:373)"s supply at each price. P firm 1 p firm 2 p market. 10 15 q 20 25 q 30 40 q. If firms are price takers but there are barriers to entry, profits will persist. If the industry is perfectly competitive, firms are not only price takers but there is free entry.