ADMS 4503 Lecture Notes - Bull Spread, Risk-Free Interest Rate, Alphabet Inc.

Document Summary

Get access

Related Documents

Related Questions

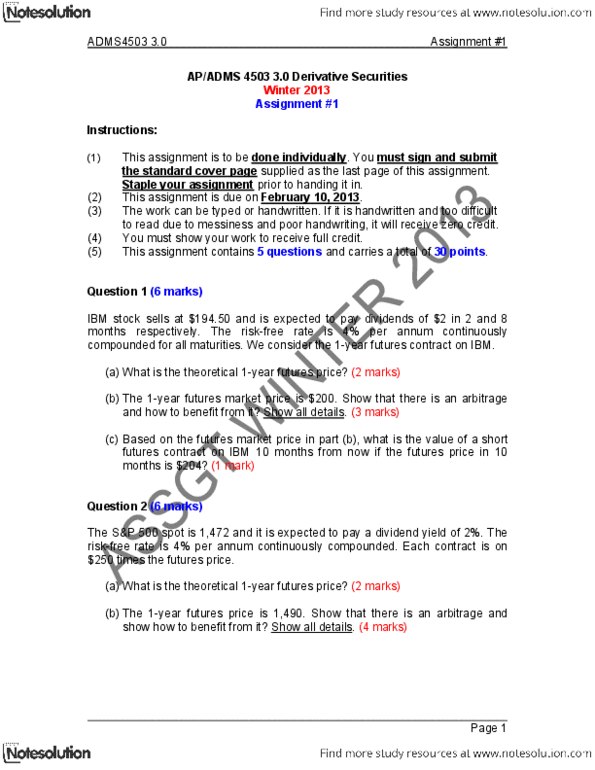

Instructions:

Read the scientific inquiry below. Use the data and your scientific knowledge, to complete the questions in each of the sections on the rest of this document. Place your answers, in the space provided and bold or change the color of the text of your answer. Once the assignment is complete, save it as a PDF document file. To submit this assignment, email the completed PDF document to your instructors email address by the due date/time. This assignment is to be done individually. Per the Angelina College student handbook, plagiarism will be will not be tolerated.

Scientific Inquiry:

A farmer wishes to determine which of the two fertilizers, Brand X or Brand Y, helps his corn crops grow at a faster rate in a five-week period of time. He asks his daughter, whom is a college freshman taking introductory biology, to design an experiment to help him test each fertilizer. They decide to grow three different crops of corn, each grown in a controlled environment, receiving the same amount of sunlight, same climate, soil type, and water. Crop 1 will receive no fertilizer during watering. Crop 2 will receive Brand X fertilizer while watering. Crop 3 will receive Brand Y fertilizer while watering. The farmer and his daughter performed the experiment and collect data on each fertilizer over a five-week period. Use the data, represented in Table 1, to complete the following assignment.

Table 1. Average height of corn plants when treated with Brand X or Brand Y fertilizer compared to corn plants not treated with fertilizer (control).

| Time (T) in weeks | Control (cm) | Brand X (cm) | Brand Y (cm) |

| 0 | 0 | 0 | 0 |

| 1 | 1.3 | 1.4 | 1.2 |

| 2 | 2.4 | 2.7 | 2.3 |

| 3 | 4.2 | 8.3 | 7.3 |

| 4 | 6.8 | 12.4 | 8.2 |

| 5 | 8.7 | 16.8 | 11.6 |

Section 1: Representation

Define each term or variable, with respect to the scientific inquiry.

Independent variable-

Dependent variable-

Control group-

Experimental group(s)-

Hypothesis-

Write the equation to determine the average growth rate, with the appropriate values included, for each corn crop type (control, Brand X, and Brand Y). Use the equation shown below.

Growth rate = (T5 â T0)/5

Control =

Brand X =

Brand Y =

Section 2: Calculation

Solve the equations generated, in question 2, for each corn crop type. You must show your work, in the space below, for full credit.

Control =

Brand X =

Brand Y =

Section 3: Interpretation

Analyzing the data table and the calculated growth rates, complete the following questions.

Which crop type grew the fastest? Explain your answer using factual information.

Which plant was tallest? Explain your answer using factual information.

What can you conclude about the treatment of fertilizer on crop growth? Explain your answer using factual information.

Section 4: Application and Analysis

What could happen if the temperature were not controlled during the experiment? Would this impact treatment effectiveness on plant growth? Explain your answer.

Do you think the same outcome would occur if pine trees were used? Explain your answer.

If a particular fertilizer works on corn crops, should we be using that fertilizer on all plants? Why or why not?