ACTG 2011 Lecture Notes - Lecture 9: Revenue Recognition, Financial Statement

Document Summary

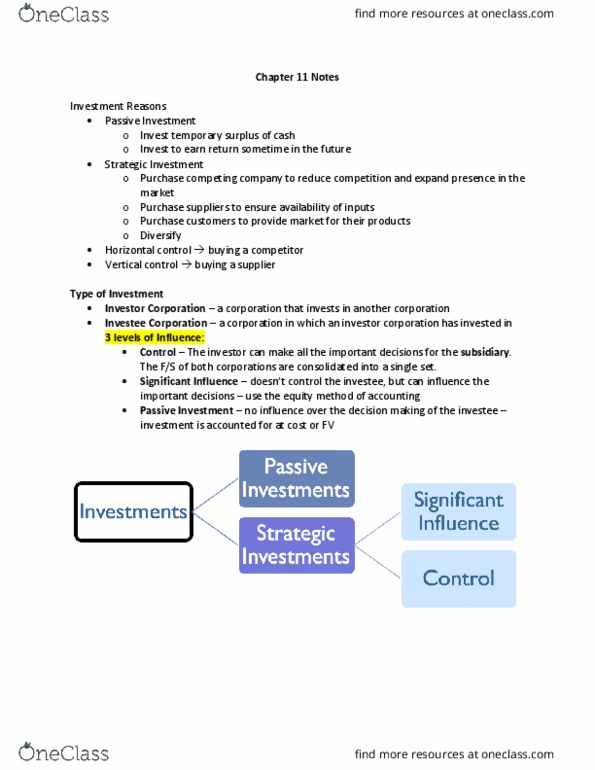

Chapter 5, 10 and 11 question + pre-midterm topics (bonds/amortization schedules (not likely since already tested), leases, chapter 9 is fair game. Table 11. 2 consolidated balance sheet (add current assets, capital assets, and liabilities and just record good will as is. If you own it you have to consolidate your statements and merge them. Own inc 1 inc 2 can"t call your own because you won"t know how much is coming from each. Own 20-50% of stock - significant influence, when you merge your statements will be overstated. Passive - no control, no significance, some influence, treat as regular influence. Portion you do not own is recorded as non-controlling interest. Investment if it"s passive, significant etc. question answer using different methods. Gain/loss can be left in oci or transferred to net income when sold. Page 674 - know difference if company decides to consolidate. Don"t have to compute nci, just know what it is.