EC120 Lecture Notes - Lecture 8: Marginal Revenue, Profit Maximization, Marginal Cost

18 views3 pages

30

EC120 Full Course Notes

Verified Note

30 documents

Document Summary

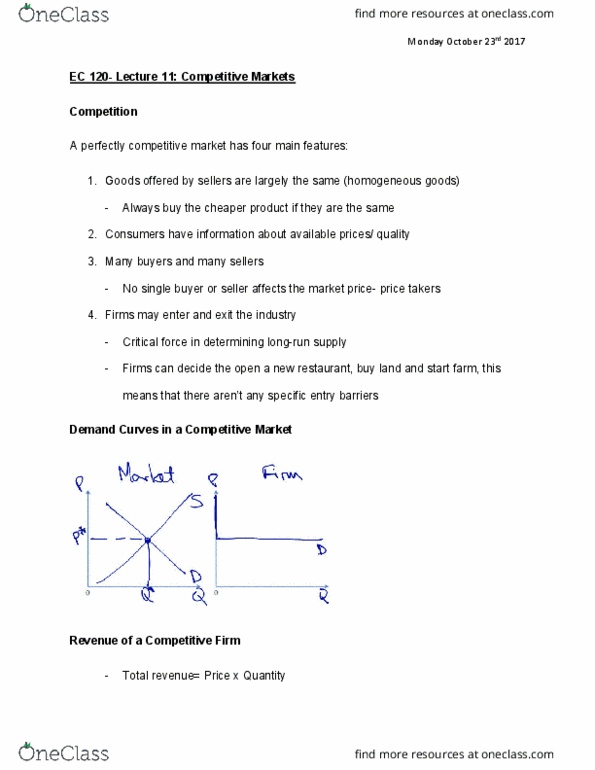

A perfectly competitive market has three main features: goods offered by sellers are largely the same (homogeneous goods, many buyers and many sellers. No single buyer or seller affects the market price - price takers: firms may enter and exit the industry. Average revenue = total revenue/quantity = price. Marginal revenue = price = average revenue. Basic assumption - firms maximize economic profit. With competitive firms: price minus marginal cost. If increasing quantity creates more profit increase quantity. If marginal profit is positive - increase quantity. If reducing quantity generates more profit decrease quantity. If marginal profit is negative - decrease quantity. If marginal profit = zero - profit maximizing quantity. Firm produces nothing - pay fixed costs, no revenue. 1 = p q tc = p q fc vc. 1 = p q fc vc fc = 0. Cancel fixed costs, divide by quantity produce if:

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers