BU127 Lecture Notes - Lecture 5: Accrual, Deferral, Asset

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

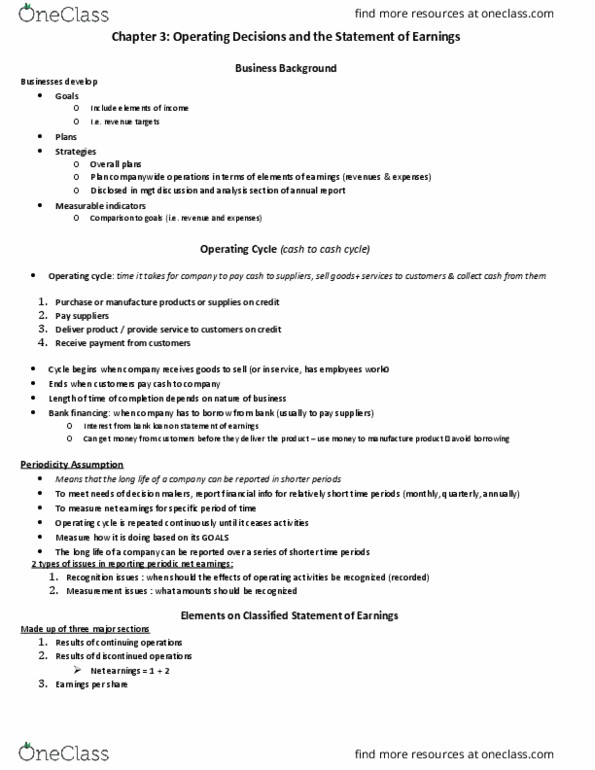

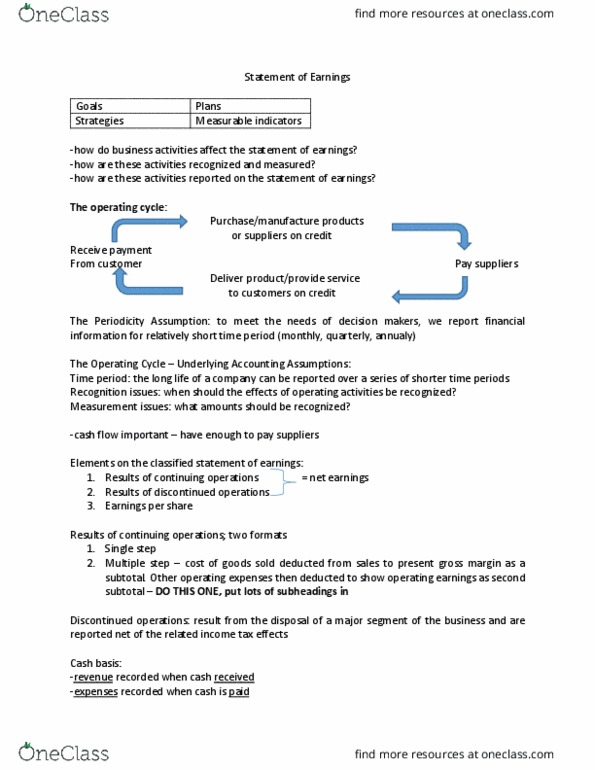

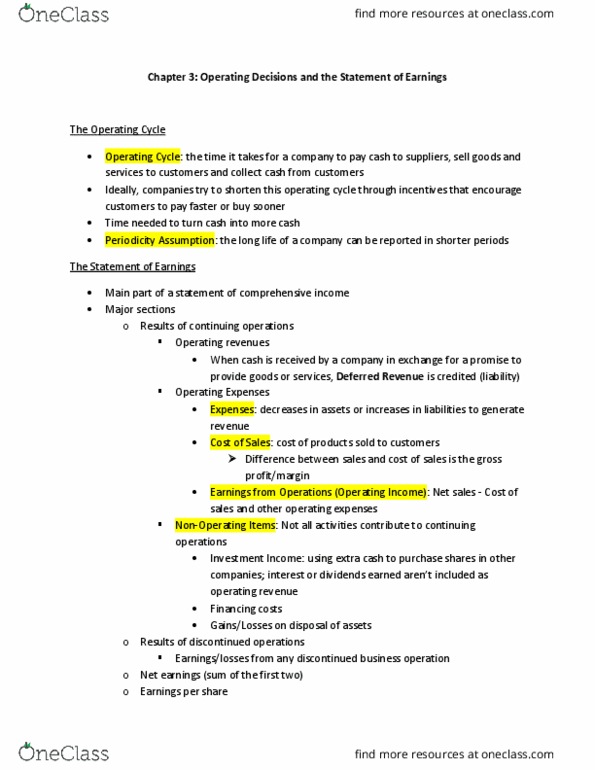

The operating (cash-to-cash) cycle is the time it takes for a company to pay cash to suppliers, sell goods and services to customers and collect cash from customers. The long-term objective is to turn it into more cash. Purchase/manufacture products on credit pay suppliers deliver product or service to customers on credit receive payment from customers. The periodicity assumption the long life of a company can be reported in shorter time periods (months, quarters, years) Discontinued operations: not relevant in anyway because they are gone forever. From the main to the discontinued operations, the information relevancy decreases (less and less detail within each) Earnings per share = net earnings/ average number of shares outstanding. How are operating activities recognized and measured? cash basis: Revenues are recorded when cash is received. Expenses are recorded when cash is paid. Revenues are recorded when earned and expenses are recorded when incurred, regardless of the timing of cash receipts or payments.