Management and Organizational Studies 3311A/B Lecture Notes - Lecture 3: Weighted Arithmetic Mean, European Cooperation In Science And Technology, Capital Asset Pricing Model

6 Dec 2018

School

Department

Professor

Document Summary

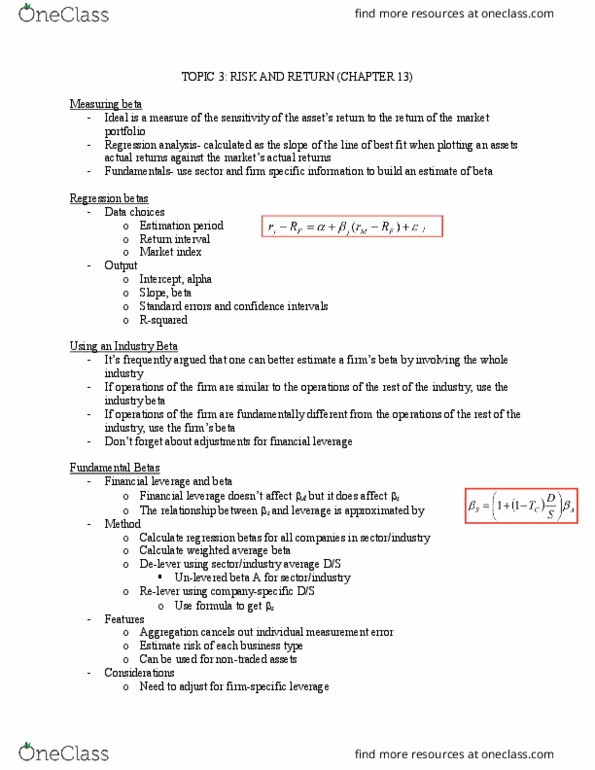

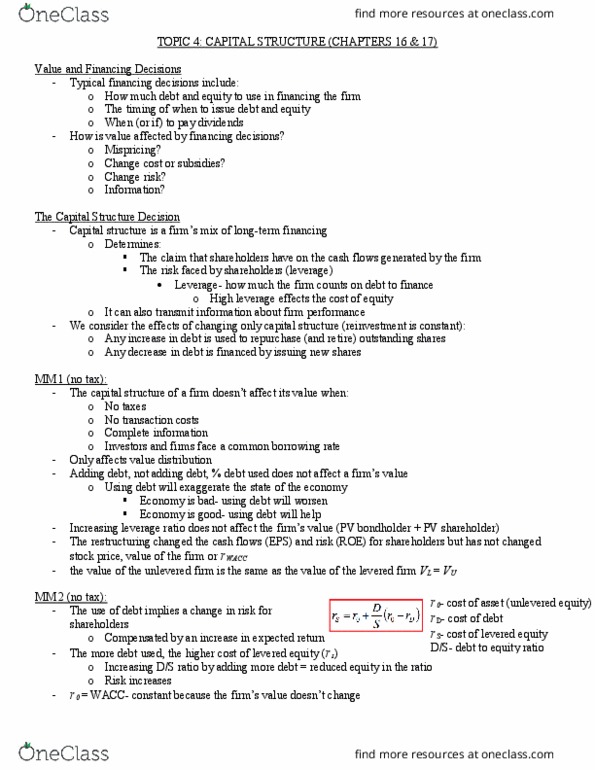

Fundamental beta: financial leverage does not affect asset beta (ba), but it does affect stock beta (bs) In class explanation of formula: you can think of the ba as a portfolio, containing both debt (d) and stock (s) and therefore, bd is risk free, therefore, equals zero. Ba=[bs(s/(s+d)]+[bd(d/(s+d): note this is with no tax, method. Bs=ba*(1+d/s: calculate beta for all companies in industry, calculate weighted average beta, de-lever using industry average (debt/stock)", de-lever bs find ba for each industry, using the following formula. Ba=bs*1+[((1-tax)*d)/s: re-lever using company specific d/s, re-lever ba from bs using the following formula, Investor receives return from firm : cost of capital (firm perspective) Firm owes the investor the return : use cost of financing as r . The firms as a portfolio: consider a company financed through debt and shares, value of firm = debt + shares, the weights of the portfolio are proportional to the market value of each security.