Management and Organizational Studies 2285 Lecture Notes - Lecture 9: Financial Statement, Income Statement

7 Jun 2017

School

Department

Professor

Document Summary

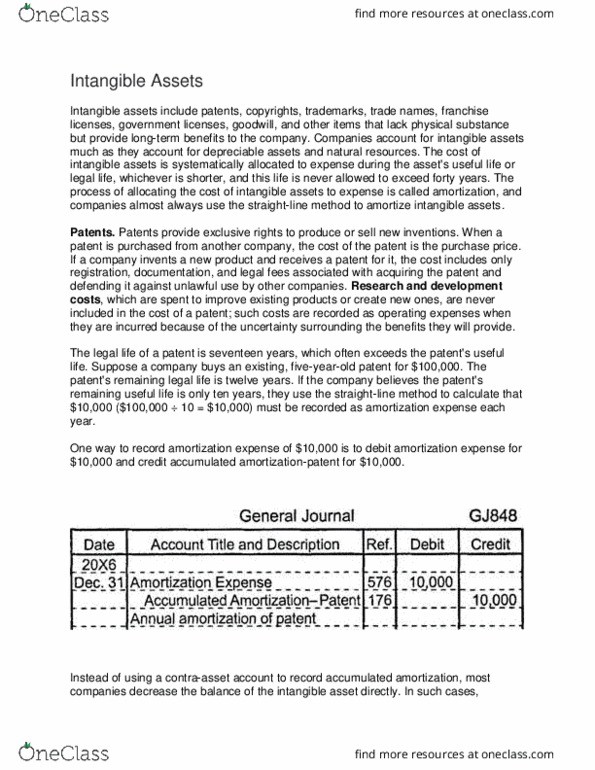

Exercise 12-9 (25-30 minutes) (a) fiscal 2014: the ,000 is a research and development cost that should be charged to r & d expense and, if not separately disclosed on the income statement, total r & d. Expense should be separately disclosed in the notes to the financial statements. These costs are not eligible for capitalization since the six development phase criteria for capitalization are not met. (b) fiscal 2015: Payable, etc. (to record research and development expense) Assuming the criteria are not fulfilled for the development phase. Payable, etc. (to record legal and admin. costs incurred to obtain patent) Accumulated amortization expense (,000 5 = ,000)] Payable, etc. (to record legal cost of successfully defending patent) The cost of defending the patent is capitalized because the defence was successful and because it extended the useful life of the patent. (d)pre sept 2016: