ECO100Y1 Lecture Notes - Lecture 9: Natural Monopoly, Perfect Competition, Longrun

Document Summary

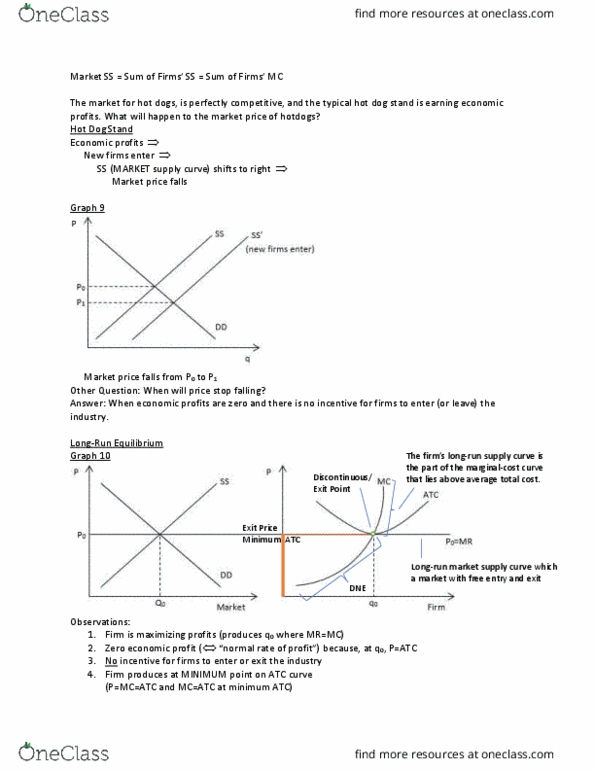

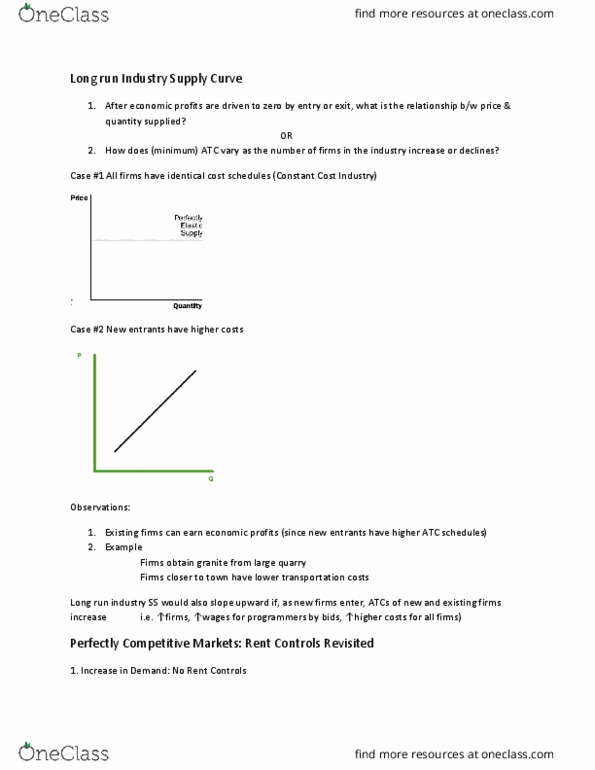

Demand increases, market price increases (from to ) Case 1: new firms have identical cost schedules as existing firms. In long run, p==minimum (unchanged) atc (cid:1005)(cid:1004),(cid:1004)(cid:1004)(cid:1004) (cid:862)old(cid:863) fir(cid:373)s a(cid:374)d (cid:1005),(cid:1004)(cid:1004)(cid:1004) (cid:862)(cid:374)ew(cid:863) fir(cid:373)s ear(cid:374) zero eco(cid:374)o(cid:373)ic profits. Long-run industry supply curve is horizontal (perfectly elastic) Case 2: the entry of 1,000 new firms results in higher wages and mc of all firms increase by [so atc of all firms increase by ] In the long run, p==[minimum] atc of all firms. Price falls from short-term level () as new firms enter industry, but only to . In eco100, we will focus only on case 1: as shown by case 2, we need to track how [minimum] atc changes as new firms enter industry to identify long-run industry supply curve. Single seller (of product with no close substitutes) Barriers to entry: legal barriers (legal monopoly) *o(cid:374)e pipeli(cid:374)e is efficie(cid:374)t, the go(cid:448)er(cid:374)(cid:373)e(cid:374)t (cid:449)o(cid:374) t (cid:373)ake (cid:1005)(cid:1004)(cid:1004) pipeli(cid:374)es.