CCT109H5 Lecture Notes - Lecture 6: Dependent And Independent Variables, Business Cycle

11 Jul 2017

School

Department

Course

Professor

10

CCT109H5 Full Course Notes

Verified Note

10 documents

Document Summary

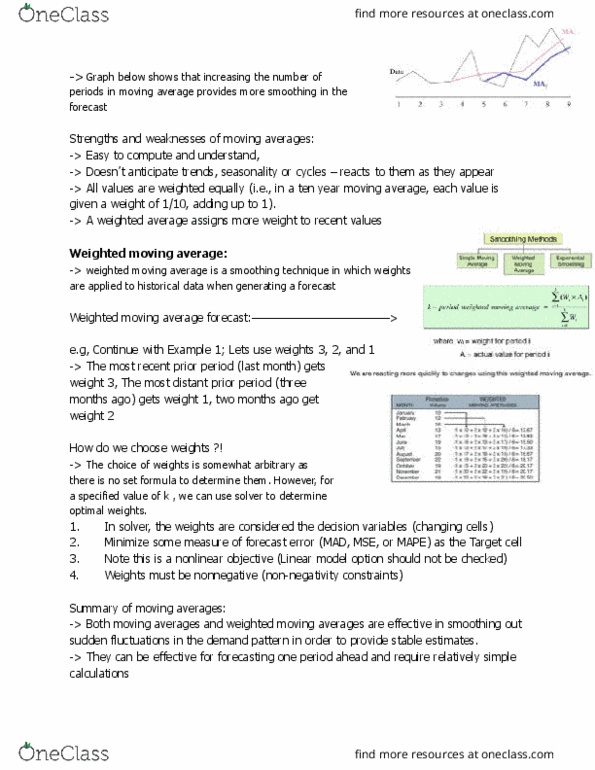

Time-series forecasting: set of evenly spaced numerical data. Obtained by observing response variable at regular time periods: forecast based only on past values, no other values are important. Assume factors influencing present and past will continue to influence in. Cyclical component the future: repeating up and down movements, affected by business cycle, political, and economic factors, multiple years duration, often casual or associative relationships. Random component: erratic, unsystematic, residual fluctuations, due to random variation or unforeseen events, short duration and nonrepeating. Moving average method: ma is a series of arithmetic means, used if little or no trend, used often for smoothing. = sum demand in previous n periods / n. Weighted moving average: used when some trend might be present. Older data usually less important: weights based on experience and intuition, = sum((weight for period n)(demand in period n)) / sum of weights. Exponential smoothing: form of weighted moving average. Weights decline exponentially most recent data weighted.