ECON 202 Lecture 3: Chap3-Spring2016

7 Jul 2016

School

Department

Course

Professor

Document Summary

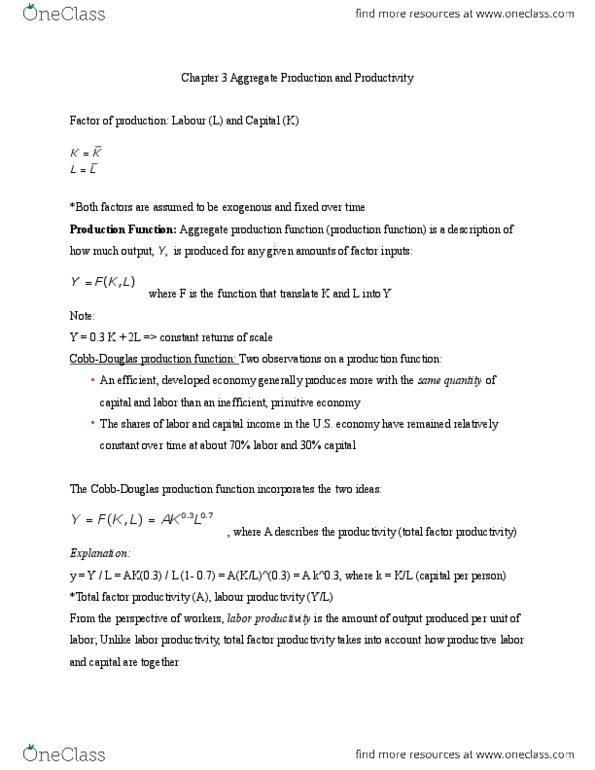

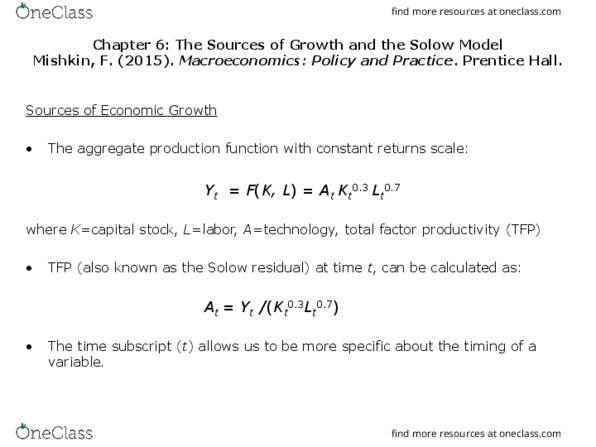

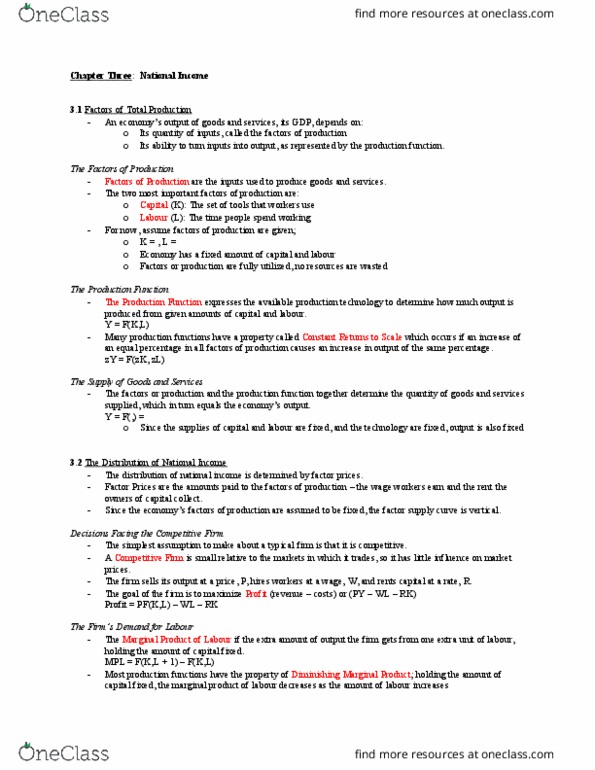

Factors of production (inputs) include: labor (l) and capital (k: both factors are assumed to be exogenous and fixed over time: Is a description of how much output, y, is produced for any given amounts of factor inputs: F k l where f is the function that translates k and l into y: two observations on a production function: An efficient, developed economy generally produces more with the same quantity of capital and labor than an inefficient, primitive economy. The shares of labor and capital income in the u. s. economy have remained relatively constant over time at about 70% labor and 30% capital. The cobb-douglas production function incorporates the two ideas: Ak l where a describes productivity (total factor productivity) From the perspective of workers, labor productivity is the amount of output produced per unit of labor: unlike labor productivity, total factor productivity (tfp) takes into account how productive labor and capital are together.