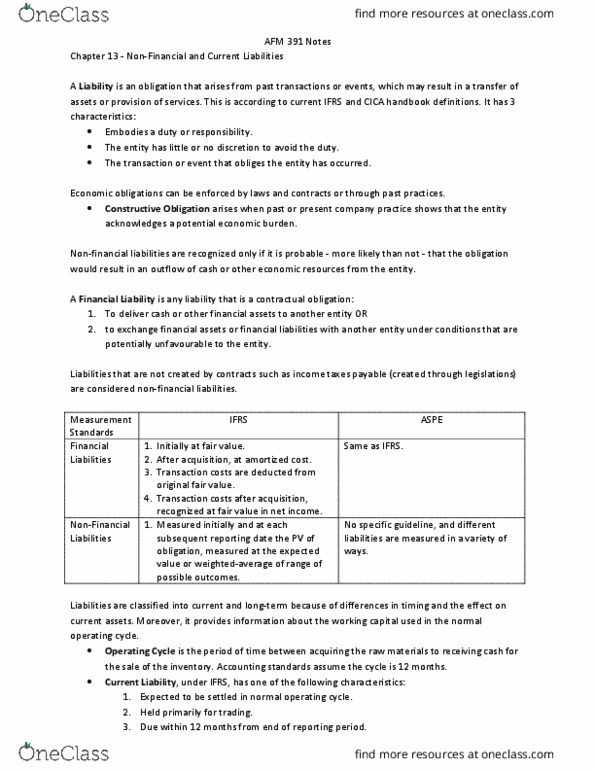

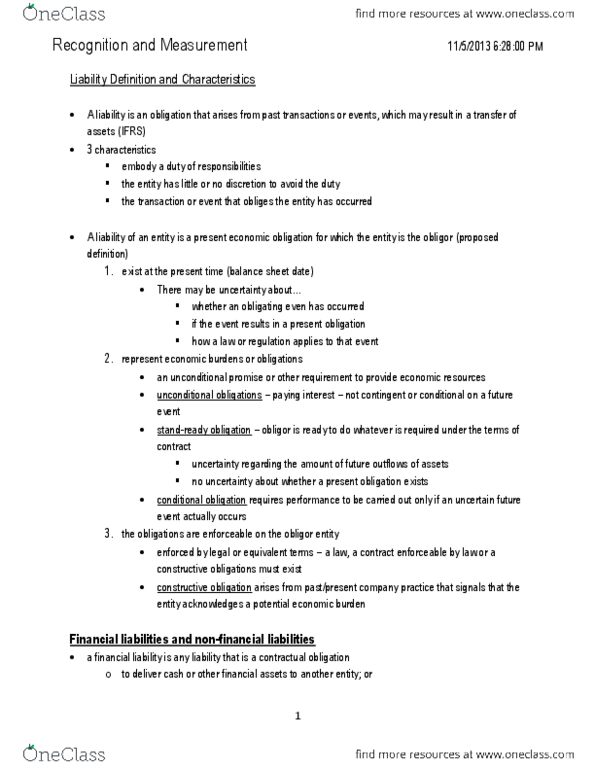

AFM391 Lecture Notes - Lecture 1: Accounts Payable, Current Liability

28 Jun 2018

School

Department

Course

Professor

INTRODUCTION

A.

Liabilities are obligations to provide cash, other assets, or services to external parties•

The obligation is a financial or non

-

financial liability

○

The market rate of interest is different from that recorded in the loan documentation

○

The market rate of interest has changed since the liability was incurred

○

There is uncertainty about the amount owed

○

The amount owed depends upon the outcome of a future event

○

The obligation is payable in a foreign currency

○

Many factors can affect the value of the indebtedness •

DEFINITION, CLASSIFICATION, AND MEASUREMENT OF LIABILITIES

B.

Liabilities defined

1.

A liability is a present obligation of the entity arising from past events, the settlement of which is

expected to result in an outflow from the entity of resource embodying economic benefits

•

e.g. if I repair products within the warranty period but also after the warranty period to

maintain good customer relations

○

Present obligations are normally legally enforceable but can also be constructive •

Recognition

2.

Although you do not know how much to pay for warranty, we still record a liability for the

estimated cost

○

Provision is the IFRS terminology used to refer to liabilities that have some uncertainty with

respect to the timing or amount of payment. All provisions are liabilities

○

IAS 37 suggests that it would be rare that a reliable estimate cannot be obtained

•

Financial and non

-

financial liabilities

3.

e.g. loan from a bank

○

Financial liability

is a contractual obligation to deliver cash or other financial assets to another

party

•

Usually settled through delivery of goods or services

○

e.g. magazines routinely sell subscription to customers by periodically providing goods

rather than paying cash or providing a financial asset

○

e.g. warranties

○

e.g. income taxes payable as it is not contractual in nature

○

Non

-

financial liability are obligations that meet the criteria for a liability but are not financial

liabilities

•

Some Financial liabilities are measured at fair value rather than amortized cost

•

Current vs. non-current liabilities4.

If it does not have an unconditional right to defer settlement of the liability for at least 12

months after the reporting period

○

Certain financial liabilities classified as FVPL would also be reported as current liabilities

○

Current liabilities expect to settle within one year of the balance sheet or the business's normal

operating cycle

•

Measurement5.

There are three categories of indebtedness for measurement

•

Financial liabilities at FVPL should be initially and subsequently measured at fair value

a.

Accounting standards permit many current obligations to be recognized at their maturing

face value because it is hard to determine fair value of short

-

term obligations and time value

of money is immaterial

○

Other financial liabilities not FVPL should be initially measured at fair value minus the transaction

costs associated with incurring the obligation. Subsequent to the date of acquisition, financial

liabilities not FVPL are measured at amortized cost using the effective interest method

b.

Warranties are recorded at management's best estimate or settlement value

○

Prepaid magazine subs are valued at the initially received less the amount earned to date

○

Non

-

financial liabilities depends on their nature

c.

An entity shall measure trade receivables that do not have a significant financial component at

their transaction price

•

CURRENT LIABILITIES

C.

Current liabilities arise from past events: the amounts to be paid is known or can be reasonably

estimated

•

Contingencies arise from past events: the amount to be paid is determined by future events•

Financial guarantees arise from contracts previously entered into: the amount to be paid is

determined by future events

•

An entity generally uses its

current assets

such as cash to pay its current liabilities when due

•

Trade payables

1.

Also known as accounts payable or trade accounts payable

•

Chapter 11

-

Current Liabilities and Contingencies

January 4, 2018 9:25 PM

AFM 391 Page 1

Document Summary

Liabilities are obligations to provide cash, other assets, or services to external parties. Many factors can affect the value of the indebtedness. The obligation is a financial or non-financial liability. The market rate of interest is different from that recorded in the loan documentation. The market rate of interest has changed since the liability was incurred. The amount owed depends upon the outcome of a future event. The obligation is payable in a foreign currency. A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resource embodying economic benefits. Present obligations are normally legally enforceable but can also be constructive e. g. if i repair products within the warranty period but also after the warranty period to maintain good customer relations. Ias 37 suggests that it would be rare that a reliable estimate cannot be obtained.