ACCTG322 Lecture Notes - Lecture 8: Cash Flow, Budget, Finished Good

17 Apr 2015

School

Department

Course

Professor

Document Summary

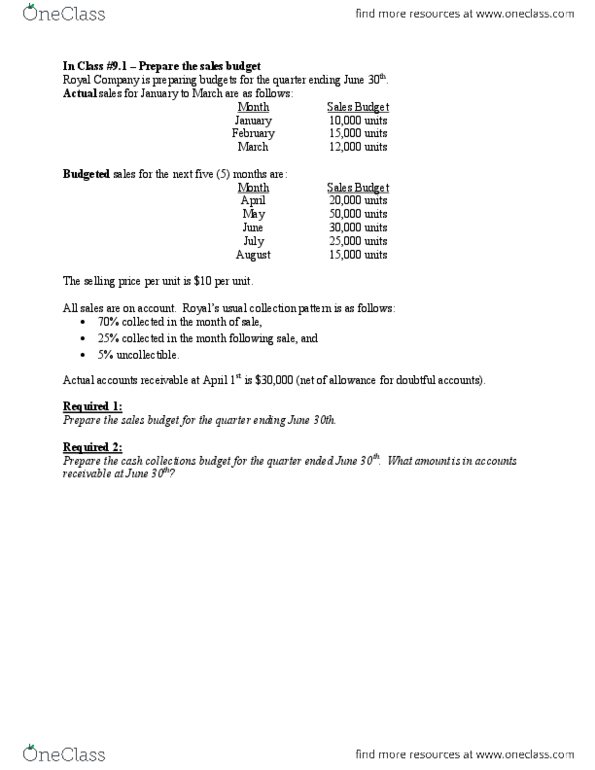

It provides resource information that can be used to improve decision making. Responsibility accounting: managers should be held responsible for those items and only those items that the manager can actually control to a significant extent. Operating budgets direct labour budget: shows both the quantity of hours and cost of direct labour necessary to meet production requirements, critical in maintaining a labour force that can meet expected production, total direct labour cost formula: Operating budgets manufacturing overhead budget: shows the expected manufacturing overhead costs for the budget period, distinguishes between fixed and variable overhead costs, may want to separate cash and non-cash items for cash flow purposes. Operating budgets selling and administrative expense budget: projection of anticipated operating expenses, distinguishes between fixed and variable costs. Indicates expected profitability of operations: provides a basis for evaluating company performance, prepared from the operating budgets, sales budget, production budget, direct materials budget, direct labour budget, manufacturing overhead budget, selling and administrative expense budget.