BUS 251 Lecture Notes - Lecture 1: Canada Revenue Agency, Financial Statement, Cash Flow Statement

24 Feb 2016

School

Department

Course

Professor

Document Summary

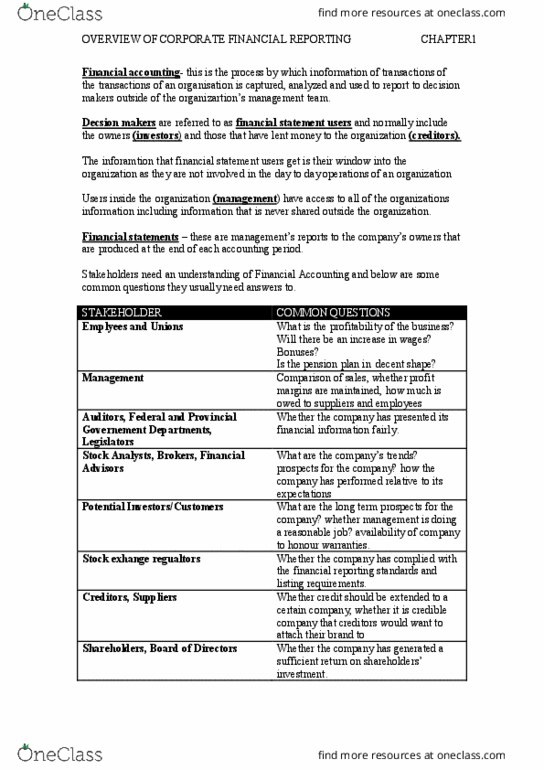

Shareholders and others use a company"s financial statement to see how the company has performed and what its future prospects might be. Shareholders use them to make informed decisions about things such as whether to sell their shares, hold onto them, or buy more. Creditors use financial statements to assess a company"s ability to service its debts (pay interest and repay principal) Suppliers may use them to determine whether to allow the company to purchase on credit. Companies communicate all this information through financial reporting and the tool used to prepare financial information is accounting. Financial accounting: the process by which information on the transactions of an organization is captured, analyzed, and used to report to decision makers outside of the organization"s management team. Decision maker= financial statement user (usually outside of the organization) Those who lent money to the organization= creditors. Primary purpose of financial accounting information: to aid these users in their economic decision-making relative to the organization.