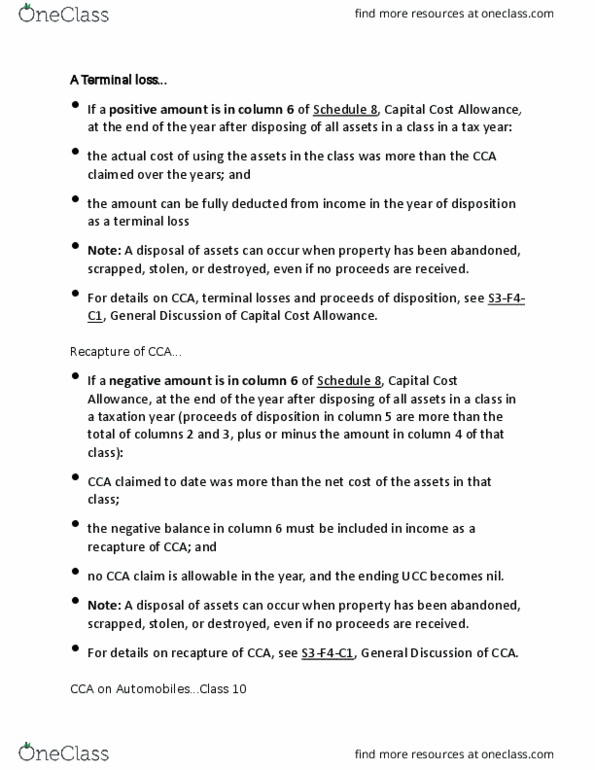

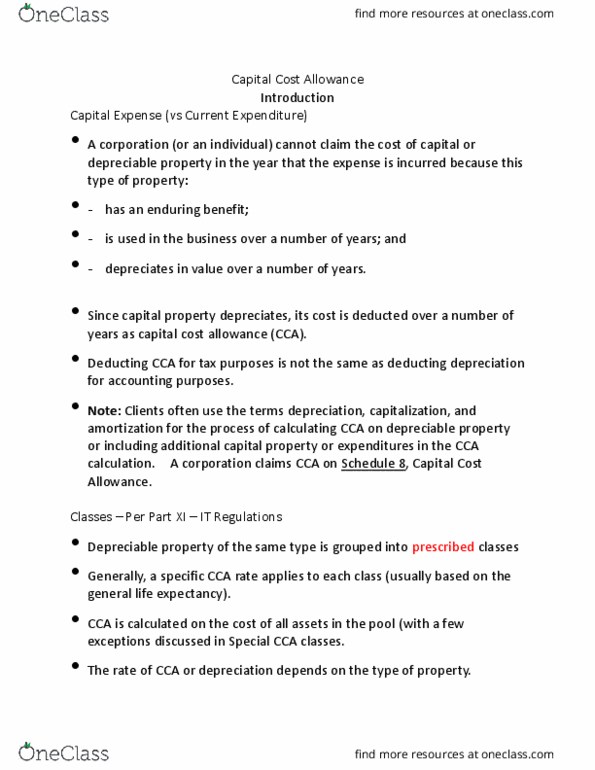

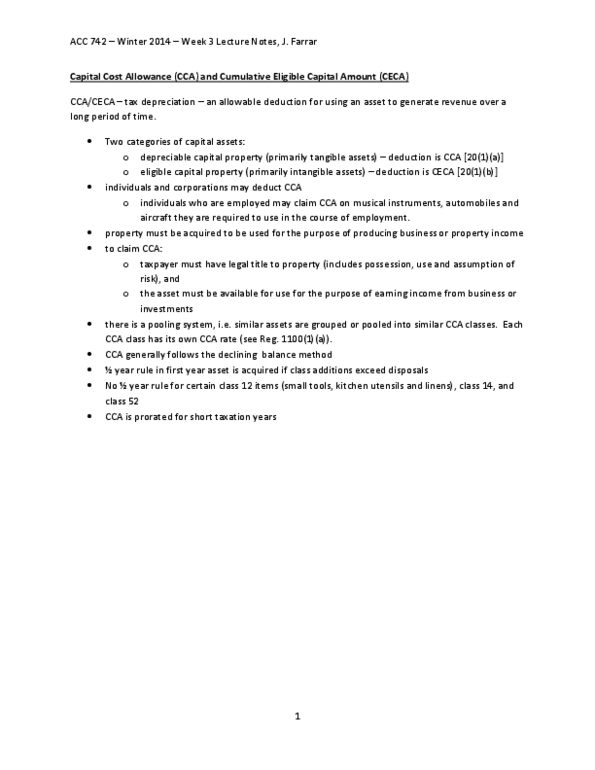

ACC402 Lecture Notes - Lecture 13: Capital Cost Allowance, Capital Cost, Office Supplies

Get access

Related Documents

Related Questions

Multiple Choice:

_____For purposes of calculating depreciation on the taxpayersbusiness usage of his home, the depreciable basis of the officeis:

The allocable share (example - square footage) of the adjustedbasis of the home when he converted the room from personal space toan office for business use.

The allocable share of the fair market value of the home at thetime he converted the room to an office space for business.

The lesser of a. or b.

The greater of a. or b.

____ Which of the following is not included inthe taxpayerâs basis of business property?

Sales taxes paid with the purchase

Title insurance paid with the purchase

Amounts paid to have the property installed

Amounts paid to have the property delivered

All of the above are included in the taxpayerâs basis.

____ A taxpayer has a net short term capital lossof $2,000 and a net long term capital loss of $3,000 for the taxyear. If there are no other gains or losses, what, if anything,carries over to the next year?

$2,000 short term capital loss

$2,000 long term capital loss

$2,000 short term capital loss; $3,000 long term capitalloss

$500 short term capital loss; $1,500 long term capital loss

The taxpayer has no capital loss carryover.

_____ A taxpayer purchased a capital asset on March 22, 2015.What is the earliest date that he can dispose of the asset wherethe sale qualifies for long term capital gains/loss treatment?

September 22, 2015

September 23, 2015

March 22, 2016

March 23, 2016

_____ A married couple sells the following capital assets duringthe year:

Date Acquired | Date Sold | Sales Price | Adjusted Basis | |

The coupleâs net capital gain is:

$4,000

$12,000

$5,000

$11,000

None of the above

_____ Land purchased for $80,000 in 2000 and used in thetaxpayers business is sold in 2015 for $87,000. The sale of theland results in:

$7,000 short term capital gain

$7,000 long term capital gain

$7,000 ordinary income

$7,000 section 1231 gain

None of the above

_____ Taxpayer purchased office equipment for $9,000. Theequipment had been depreciated $5,000. It was sold for $7,500. Whatis the amount and nature of the gain/loss from the sale?

$1,500 ordinary loss

$1,500 capital loss

$3,500 ordinary income

$3,500 long term capital gain.

_____ Taxpayer has a plant where she acquired a machine for$14,000. Over time depreciation of $6,000 was claimed. In thecurrent year taxpayer sells the asset for $19,000. What is theamount and nature of the gain/loss from the sale?

$6,000 of ordinary income, $5,000 long term capital gain

$5,000 of long term capital gain, $5,000 of ordinary income

$11,000 ordinary income.

$11,000 long term capital gain

______ Equipment used in the business is purchased in 2012 for$50,000. It was sold in 2015 for $22,000.

Depreciation information is as follows:

Accelerated depreciation claimed $23,758

Straight line Depreciation would have been$21,500

What is the gain or loss on the sale of the equipment, and howwill it be treated for tax purposes?

$4,242 Section 1231 loss

$1,758 Section 1231 loss

$2,258 ordinary loss; $1,984 Section 1231 loss

$4,242 ordinary loss

$6,500 ordinary loss

_____ In Malat v Riddell, 383 U.S. 569, 86 S.Ct. 1030,which of the following statements is accurate:

The Supreme Court sustained the governmentâs position, holdingthat the property was held by the taxpayer primarily for sale tocustomers in the ordinary course of his trade or business.

The Supreme Court held that the sale of âproperty held by thetaxpayer primarily for sale to customers in the ordinary course ofa trade or business is synonymous with the wordâsubstantiallyâ.

Words of the statutes should be interpreted where possible intheir ordinary, everyday senses. The Supreme Court concluded thatas used in Section 122191), âprimarilyâ means âof first importanceâor âprincipallyâ.

In so concluding as it did, the Supreme Court found itunnecessary to remand the case back to the lower court.

Question 2

You, a recent auditor with a local auditing firm, are responsible for the audit of a new client, PresentShop, a retailer of electronic home and office equipment in Western Canada.

PresentShop has 14 locations across Western Canada. It specializes in providing customers with the latest technology in home entertainment electronics such as televisions and DVD players as well as top of the line office technology such as computers.

The business was started 15 years ago in Alberta by two brothers who are still the only owners of the company. The brothers paid themselves a management bonus in 2017 of $60,000. The business has grown as a result of excellent advertising, good locations, and reasonable prices based on the ability of the company to buy in volume. Each store has a high degree of security such as electronic bars and video surveillance.

The accounting for the stores is all electronically performed. The sales tills are downloaded every day to the main office in Calgary which performs the accounting for all of the stores. The main office also has the warehouse from which all inventory is shipped to the stores.

Business has been relatively stable but the company does have pressure from American competitors moving into Canada as well as another Western Canadian competitor, B&C Sound. As well, the business tends to fluctuate with the economic cycles so recent government cutbacks in B.C. have resulted in lower sales. As a result of a decrease in profits, the company requires a significant loan from a bank and the bank has requested audited financial statements. It is the first year that the financial statements have been audited. The bank intends to use the inventory as collateral for the loan.

PresentShop has provided you with the following financial information for the years ending December 31, 2017:

| December 31, 2017 (â000s) | |

| Total assets | $48,900 |

| Total revenues | $124,900 |

| Total net income before tax | $23,500 |

| Total net income after tax | $15,400 |

Required:

Assess inherent risk at the overall financial statement level. Conclude on inherent risk. Is it low, medium or high?

Assess control risk at the overall financial statement level. Conclude on control risk. Is it low, medium or high?

Conclude on detection risk and the level of substantive testing required.

Assess overall (planning) materiality

Question 3

Explain the approach adopted by auditors of identifying accounts and related assertions at risk of material misstatement. How does this approach help auditors to reduce audit risk to an acceptably low level?

Question 4

What is the relationship between materiality and audit risk?

# Warren Co. recorded a right-of-use asset of $800,000 in a10-year Type A lease. The interest rate charged by the lessor was8%. Under the new ASU, the balance in the right-of-use asset aftertwo years will be:

#Refer to the following lease amortization schedule. The 10payments are made annually starting with the inception of thelease. Title does not transfer to the lessee and there is nobargain purchase option or guaranteed residual value. The asset hasan expected economic life of 12 years. The lease isnoncancelable.

| Payment | Cash Payment | Effective Interest | Decrease in balance | Balance |

| 63,282 | ||||

| 1 | 10,000 | 10,000 | 53,282 | |

| 2 | 10,000 | 6,394 | 3,606 | 49,676 |

| 3 | 10,000 | 5,961 | 4,039 | 45,638 |

| 4 | 10,000 | 5,477 | 4,523 | 41,114 |

| 5 | 10,000 | 4,934 | 5,066 | 36,048 |

| 6 | 10,000 | 4,326 | 5,674 | 30,373 |

| 7 | 10,000 | 3,645 | 6,355 | 24,018 |

| 8 | 10,000 | 2,882 | 7,118 | 16,901 |

| 9 | 10,000 | ? | ? | ? |

| 10 | 10,000 | ? | ? | ? |

What would the lessee record as annual depreciation on the assetusing the straight-line method?

#XYZ Company leased equipment to West Corporation under a leaseagreement that qualifies as a capital lease to West but not as aresult of a bargain purchase option or a title transfer. Thepresent value of the asset is $600,000. The expected economic lifeof the asset is 10 years. The lease term is five years. Using thestraight-line method, what would West record as annualdepreciation?

# If the lessee and lessor use different interest rates toaccount for a capital lease, then:

Total expenses for the lessee will be different from thelessor's total revenues.

Total expenses for the lessee will equal the lessor's totalrevenues.

GAAP has been violated by at least one party.

The lessee will report more net income for the year.

##

Technoid Inc. sells computer systems. Technoid leases computersto Lone Star Company on January 1, 2016. The manufacturing cost ofthe computers was $12 million.

This noncancelable lease had the following terms:

⢠Lease payments: $2,466,754 semiannually; first payment at January1, 2016; remaining payments at June 30 and December 31 each yearthrough June 30, 2020.

⢠Lease term: five years (10 semiannual payments).

⢠No residual value; no bargain purchase option.

⢠Economic life of equipment: five years.

⢠Implicit interest rate and lessee's incremental borrowing rate:5% semiannually.

⢠Fair value of the computers at January 1, 2016: $20million.

Collectibility of the rental payments is reasonably assured, andthere are no lessor costs yet to be incurred.

Lone Star Company would account for this as:

A capital lease.

A direct financing lease.

A sales type lease.

An operating lease.

##

Refer to the following lease amortization schedule. The 10payments are made annually starting with the inception of thelease. Title does not transfer to the lessee and there is nobargain purchase option or guaranteed residual value. The asset hasan expected economic life of 12 years. The lease isnoncancelable.

| Payment | Cash Payment | Effective Interest | Decrease in balance | Balance |

| 63,282 | ||||

| 1 | 10,000 | 10,000 | 53,282 | |

| 2 | 10,000 | 6,394 | 3,606 | 49,676 |

| 3 | 10,000 | 5,961 | 4,039 | 45,638 |

| 4 | 10,000 | 5,477 | 4,523 | 41,114 |

| 5 | 10,000 | 4,934 | 5,066 | 36,048 |

| 6 | 10,000 | 4,326 | 5,674 | 30,373 |

| 7 | 10,000 | 3,645 | 6,355 | 24,018 |

| 8 | 10,000 | 2,882 | 7,118 | 16,901 |

| 9 | 10,000 | ? | ? | ? |

| 10 | 10,000 | ? | ? | ? |

What would be the outstanding balance after payment 10?

## Cady Salons leased equipment from Smith Co. on January 1,2016, in a Type B lease. The present value of the lease paymentsdiscounted at 10% was $80,000. Ten annual lease payments of $12,000are due at each January 1 beginning January 1, 2016. Following theguidance of the new ASU, the amortization of the right-of-use assetfor the reporting year ending December 31, 2016, would be:

## Karla Salons leased equipment from Smith Co. on July 1, 2016,in a Type A lease. The present value of the lease paymentsdiscounted at 10% was $80,000. Ten annual lease payments of $12,000are due each year beginning July 1, 2016. Smith Co. had constructedthe equipment recently for $66,000, and its retail fair value was$80,000.

Under the new ASU, what amount of interest revenue from the leaseshould Smith Co. report in its December 31, 2016, incomestatement?

### If the leaseback portion of a sale-leaseback transaction isclassified as an operating lease:

Any gain is deferred and recognized as a reduction of rentexpense.

Any gain is deferred and recognized as a reduction ofdepreciation.

Any gain is recognized at the lease's inception.

There can be no gain.