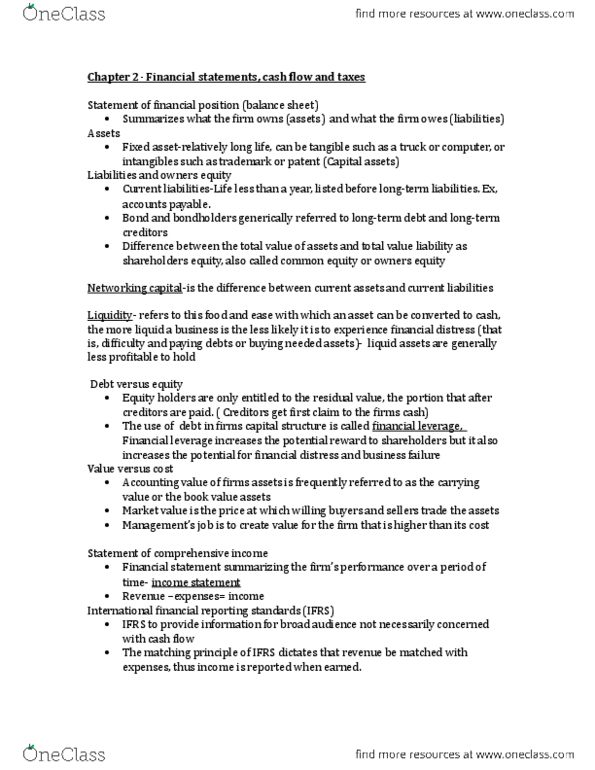

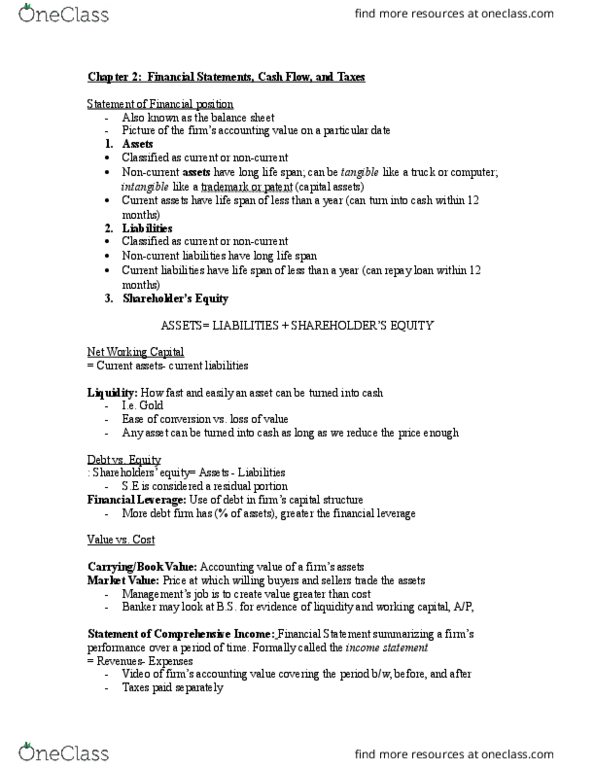

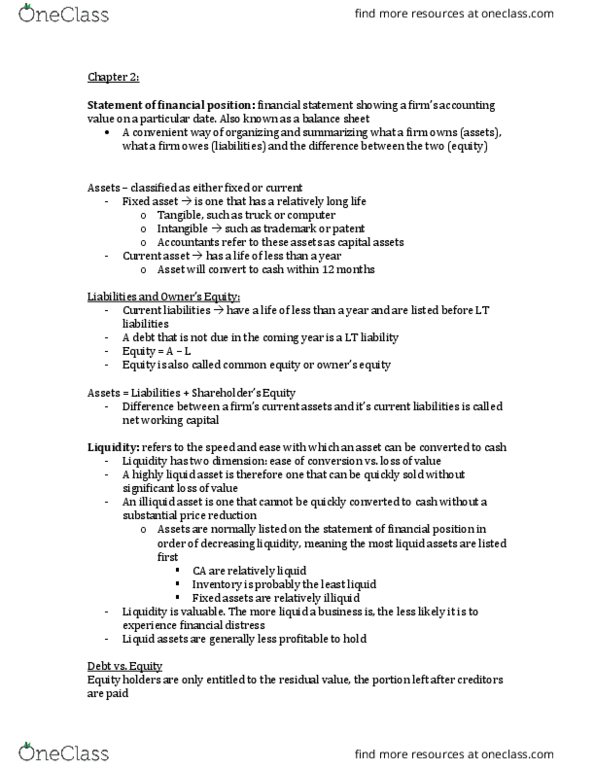

FIN 300 Lecture 8: 8 (Module 10)

Get access

Related Documents

Related Questions

Making Long Term FM Decisions - Integrative Case

Introduction: As a special analytical group set up by ACME Iron by the firmâs Controller, you have been tasked to respond to the following issues raised in a meeting with the CFO.

You must look over several prospective financial strategies to aid in the successful growth of ACME Iron: Capital investment analysis; CAPM â Capital Asset Pricing Model determination for the company; WACC â Weighted Average Cost of Capital computations; EVA â Economic Value Analysis; MVA â Market Value Added; Capital structure of the company; Dividend policy; Stock repurchase and option pricing strategy; Bankruptcy risk analysis; Decision Tree Creation; Real option analysis of projects

The CFO wants to test you out on a simple project in the first task before you get into preparing items for his board presentation in subsequent tasks and projects. He wants to see how well you perform tasks as well as how accurate and thoughtful you are in your work. Details are important to him as well as good organization/presentation and communication.

Financial Statements for use on Tasks

| ACME Iron | Balance Sheet | ||

| Assets | |||

| Current assets: | 2014 | 2015 | change |

| Cash | 500,000 | 600,000 | 100,000 |

| Investments | 1,000,000 | 1,025,000 | 25,000 |

| Inventories | 110,000,000 | 117,000,000 | 7,000,000 |

| Accounts receivable | 11,750,000 | 12,500,000 | 750,000 |

| Pre-paid expenses | 2,500,000 | 2,600,000 | 100,000 |

| Other | 0 | 0 | - |

| Total current assets | 125,750,000 | 133,725,000 | 7,975,000 |

| Fixed assets: | 2014 | 2015 | change |

| Property and equipment | 165,000,000 | 175,000,000 | 10,000,000 |

| Leasehold improvements | 0 | 0 | - |

| Equity and other investments | 55,000,000 | 65,000,000 | 10,000,000 |

| Less accumulated depreciation | 15,000,000 | 15,500,000 | 500,000 |

| Total fixed assets | 235,000,000 | 255,500,000 | 20,500,000 |

| Other assets: | 2014 | 2015 | change |

| Goodwill | 75,000,000 | 70,000,000 | (5,000,000) |

| Total other assets | 75,000,000 | 70,000,000 | (5,000,000) |

| Total assets | 435,750,000 | 459,225,000 | 23,475,000 |

| Liabilities and owner's equity | |||

| Current liabilities: | 2014 | 2015 | change |

| Accounts payable | 40,500,000 | 42,400,000 | 1,900,000 |

| Accrued wages | 85,000,000 | 90,500,000 | 5,500,000 |

| Accrued compensation | 10,000,000 | 10,855,000 | 855,000 |

| Income taxes payable | 4,024,000 | 4,697,000 | 673,000 |

| current portion of LT debt | 5,500,000 | 10,350,000 | 4,850,000 |

| Other | 0 | 0 | - |

| Total current liabilities | 145,024,000 | 158,802,000 | 13,778,000 |

| Long-term liabilities: | 2014 | 2015 | change |

| Long term debt | 125,000,000 | 130,000,000 | 5,000,000 |

| Total long-term liabilities | 125,000,000 | 130,000,000 | 5,000,000 |

| Owner's equity: | 2014 | 2015 | change |

| Common stock | 122,000,000 | 122,000,000 | - |

| Preferred stock | 16,725,000 | 16,725,000 | - |

| Accumulated retained earnings | 27,001,000 | 31,698,000 | 4,697,000 |

| Total owner's equity | 165,726,000 | 170,423,000 | 4,697,000 |

| Total liabilities and owner's equity | 435,750,000 | 459,225,000 | 23,475,000 |

Income Statement

ACME Iron

December 2015

Financial Statements in '000s of U.S. Dollars

| REVENUE | ||

| Gross Sales | 250,000 | |

| Less: Sales Returns & Allowances | 2,500 | |

| Net Sales | 247,500 | |

| COST OF GOODS SOLD | ||

| Beginning Inventory | 7,500 | |

| Add: Purchases | 4,500 | |

| Freight-in | 0 | |

| Direct Labor | 75,000 | |

| Indirect Expenses | 15,000 | |

| Inventory Available | 102,000 | |

| Less: Ending Inventory | ||

| Cost of Goods Sold | 102,000 | |

| Gross Profit (Loss) | 145,500 | |

| EXPENSES | ||

| Advertising | 7,500 | |

| Amortization | 0 | |

| Bad Debts | 5,000 | |

| Depreciation | 500 | |

| Dues and Subscriptions | 0 | |

| Employee Benefit Programs | 18,750 | |

| Insurance | 2,500 | |

| Interest | 10,350 | |

| Legal & Professional Fees | 100 | |

| Licenses & Fees | 0 | |

| Miscellaneous | 10 | |

| Office Expenses | 100 | |

| Payroll Taxes | 5,625 | |

| Postage | 3 | |

| Rent | 0 | |

| Repairs & Maintenance | 5,000 | |

| Supplies | 2,000 | |

| Telephone | 120 | |

| Travel | 1,750 | |

| Utilities | 50,000 | |

| Vehicle Expenses | 450 | |

| Wages | 25,000 | |

| Total Expenses | 134,758 | |

| Net Operating Income | 10,742 | |

| OTHER INCOME | ||

| Gain (Loss) on Sale of Assets | 0 | |

| Interest Income | 1,000 | |

| Total Other Income | 1,000 | |

| TAXES | 4,697 | |

| Net Income (Loss) | 7,045 |

TASK 2

In this task we are examining the current capital structure of ACME Iron and determining the WACC of the company. Assume that ACMEâs tax rate is 40%.

To compute the WACC you must first find the after-tax cost of debt, the cost of equity and the proportions of debt and equity in the firm. You can assume that the cost of debt before tax is 8% for the firm. Please clearly show how you derive each of these values:

After-tax cost of debt =

Cost of equity =

Proportions of debt and equity in the firm =

How do we compute the WACC in this circumstance? Why do we need to be concerned with the WACC?

Any insights into the capital structure of ACME Iron?

The weighted average cost of capital is the weighted average of the cost of equity and the after-tax cost of debt. Another way of looking at this is computing the effect of the capital structure on expected returns by investors.

WACC= S/B+S x Rs + B/B+S x RB x (1 â tc )

Where

S = value of equity

B = value of debt

Rs = cost of equity

After tax cost of debt: RB x (1 â tc )

Helpful Hint: One thing to bring up here is WACC is needed to determine risk on several levels. To determine risk we need to remember the following items:

1. Risk is deviation from expectations.

2. We need to set expectations for our investments in relation to risk and return. Higher risk = higher return.

3. Capital is obtained from the marketplace in two forms; equity and debt. This is the capital structure of a corporation and impacts the profits of a company depending on how this is managed.

4. We use our cost of capital to discount any cash flows from new investments (NPV and IRR analysis).

5. If cost of capital rises then our risk rises and the projects we undertake to increase sales and return to our investors is reduced.

6. If debt rises then our obligation to make payments on interest increases and profits can decrease if sales do not increase rapidly enough.

7. If risk increases our beta will increase to show the increase in risk. This will increase our required rate of return to stockholders (CAPM) and thus increase our required rate of return we must use in discounting future cash flows.

TASK 3

Acme is planning construction of a new loading ramp for its single iron mill. The initial cost of the investment is $1 million. Efficiencies from the new ramp are expected to reduce costs by $100,000 for the life of the plant which is currently estimated at another 30 years.

When will this project break-even on a simple cash basis and a discounted cash basis.

What is the NPV of the project if Acme has an after tax cost of debt of 8% and a cost equity of 12% (they are currently funded equally by debt and equity)?

Helpful Hint: The first step in conducting an NPV analysis is to include all the relevant cash flows. This includes savings from taxes and any expenses directly related to the venture. We reject any project with a negative NPV.

| Sorenson Manufacturing Corporation was incorporated on January 3, 2013. The corporationâs financial statements for its first yearâs operations were not examined by a CPA. You have been engaged to audit the financial statements for the year ended December 31, 2014, and your work is substantially completed. A partial trial balance of the companyâs accounts follows: |

| SORENSON MANUFACTURING CORPORATION | |||||

| Trial Balance | |||||

| at December 31, 2014 | |||||

| Debit | Credit | ||||

| Cash | $ | 11,000 | |||

| Accounts receivable | 42,500 | ||||

| Allowance for doubtful accounts | $ | 500 | |||

| Inventories | 38,500 | ||||

| Machinery | 75,000 | ||||

| Equipment | 29,000 | ||||

| Accumulated depreciation | 10,000 | ||||

| Patents | 85,000 | ||||

| Leasehold improvements | 26,000 | ||||

| Prepaid expenses | 10,500 | ||||

| Organization expenses | 29,000 | ||||

| Goodwill | 24,000 | ||||

| Licensing Agreement No. 1* | 50,000 | ||||

| Licensing Agreement No. 2* | 49,000 | ||||

| * An intangible asset representing the right to use a patent. |

| The following information relates to accounts that may yet require adjustment: |

| 1. | Patents for Sorensonâs manufacturing process were purchased January 2, 2014, at a cost of $68,000. An additional $17,000 was spent in December 2012 to improve machinery covered by the patents and charged to the Patents account. The patents had a remaining legal term of 17 years. |

| 2. | On January 3, 2011, Sorenson purchased two licensing agreements; at that time they were believed to have unlimited useful lives. The balance in the Licensing Agreement No. 1 account included its purchase price of $48,000 and $2,000 in acquisition expenses. Licensing Agreement No. 2 also was purchased on January 3, 2013, for $50,000, but it has been reduced by a credit of $1,000 for the advance collection of revenue from the agreement. |

| 3. | In December 2013, an explosion caused a permanent 60 percent reduction in the expected revenue-producing value of Licensing Agreement No. 1 and, in January 2014, a flood caused additional damage, which rendered the agreement worthless. |

| 4. | A study of Licensing Agreement No. 2 made by Sorenson in January 2014 revealed that its estimated remaining life expectancy was only 10 years as of January 1, 2014. |

| 5. | The balance in the Goodwill account includes $24,000 paid December 30, 2013, for an advertising program, which it is estimated will assist in increasing Sorensonâs sales over a period of four years following the disbursement. |

| 6. | The Leasehold Improvement account includes (a) the $15,000 cost of improvements with a total estimated useful life of 12 years, which Sorenson, as tenant, made to leased premises in January 2013; (b) movable assembly-line equipment costing $8,500, which was installed in the leased premises in December 2014; and (c) real estate taxes of $2,500 paid by Sorenson, which, under the terms of the lease, should have been paid by the landlord. Sorenson paid its rent in full during 2014. A 10-year nonrenewable lease was signed January 3, 2013, for the leased building that Sorenson used in manufacturing operations. |

| 7. | The balance in the Organization Expenses account includes preoperating costs incurred during the organizational period. |

| Required: |

| a. | For each of the items 1â7, prepare adjusting entries as necessary. (Omit the '$" sign in your response.) |

| Sl No. | General Journal | Debit | Credit |

| 1. | (Click to select)MachineryRetained earningsCost of goods soldGoodwillLeasehold improvementsOrganizational expensesRevenue received in advanceLicensing agreement no. 2 | ||

| (Click to select)EquipmentRetained earningsRevenue received in advancePatentsDrawingsOrganizational expensesBuildingsCost of goods sold | |||

| To transfer cost of improving machinery to the fixed asset account | |||

| (Click to select)EquipmentPatentsBuildingsOrganizational expensesRetained earningsCost of goods soldRevenue received in advanceLicensing agreement no. 2 | |||

| (Click to select)Retained earningsEquipmentCost of goods soldOrganizational expensesGeneral expensesBuildingsPatentsGoodwill | |||

| To record straight-line amortization of patents for the year | |||

| 2. | (Click to select)GoodwillMachineryPatentsOrganizational expensesLicensing agreement no. 2Retained earningsLeasehold improvementsCost of goods sold | ||

| (Click to select)MachineryPatentsRetained earningsRevenue received in advanceLicensing agreement no. 2EquipmentCost of goods soldInventory | |||

| To record unearned revenue in a deferred credit account | |||

| 3. | (Click to select)Organizational expensesRevenue received in advanceGoodwillLeasehold improvementsMachineryLicensing agreement no. 2Retained earningsCost of goods sold | ||

| (Click to select)Organizational expensesLeasehold improvementsRevenue received in advanceGoodwillEquipmentCost of goods soldLicensing agreement no.1Machinery | |||

| To record the 60% loss caused by the explosion in the prior year. Correction of an accounting error of the prior year. Write-off of damage due to flood | |||

| 4. | (Click to select)Leasehold improvementsGoodwillRetained earningsMachineryCost of goods soldOrganizational expensesRevenue received in advanceEquipment | ||

| (Click to select)MachineryCost of goods soldGoodwillOrganizational expensesPatentsLeasehold improvementsLicensing agreement no. 2Accounts receivable nontrade | |||

| To record amortization for the year on straight-line basis, 10-year life | |||

| 5. | (Click to select)Retained earningsEquipmentGoodwillRevenue received in advancePatentsCost of goods soldLeasehold improvementsOrganizational expenses | ||

| (Click to select)GoodwillMachineryPatentsCost of goods soldOrganizational expensesEquipmentRetained earningsLeasehold improvements | |||

| To correct the accounting error of last year of improperly capitalizing an expense item | |||

| 6. | (Click to select)Organizational expensesPatents EquipmentCost of goods soldGoodwillLicensing agreement no. 2Accounts receivable nontradeLeasehold improvements | ||

| (Click to select)GoodwillAccounts receivable nontradePatents Organizational expensesEquipmentLeasehold improvementsCost of goods soldLicensing agreement no. 2 | |||

| (Click to select)EquipmentLeasehold improvementsPatentsOrganizational expensesRevenue received in advanceBuildingsAccounts receivable nontradeCost of goods sold | |||

| To record equipment in the proper account and to record a receivable for the real estate taxes | |||

| (Click to select)Amortization expense-error correctionPatents Licensing agreement no. 2Cost of goods soldOrganizational expensesRetained earningsGoodwillAmortization expense-current year | |||

| (Click to select)Cost of goods soldGoodwillLicensing agreement no. 2Organizational expensesPatents Amortization expense-error correctionAmortization expense-current yearRetained earnings | |||

| (Click to select)DrawingsLicensing agreement no. 2BuildingsRetained earningsGeneral expensesLeasehold improvementsCost of goods soldOrganizational expenses | |||

| To record current amortization and correct the error of failure to record amortization of leasehold improvements on a straight-line, 10-year basis. No adjustment to depreciation of equipment because it was acquired in December | |||

| 7. | (Click to select)MachineryEquipmentPatentsOrganizational expensesCost of goods soldInventoryRetained earningsRevenue received in advance | ||

| (Click to select)BuildingsLicensing agreement no.2Organizational expensesPatentsEquipmentRevenue received in advanceRetained earningsCost of goods sold | |||

| To write off organizational expenses improperly capitalized in prior period | |||

References

eBook & Resources

WorksheetLearning Objective: 10-03 Describe substantive testing procedures for finance and investment accounts.

Difficulty: 3 HardLearning Objective: 10-04 Describe common errors and frauds in the accounting for investment and financing transactions and investments, and design audit procedures for detecting them.

Ask your instructor a question

©2016 McGraw-Hill Education. All rights reserved.