ACC 406 Lecture Notes - Lecture 2: Finished Good, Income Statement, Cost Driver

Document Summary

Get access

Related Documents

Related Questions

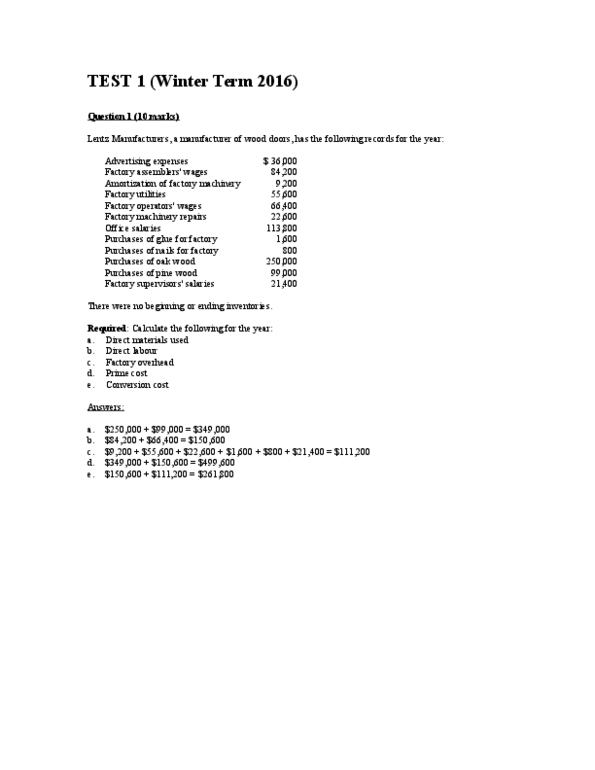

Problem 15-1A Production costs computed and recorded; reports prepared LO C2, P1, P2, P3, P4

[The following information applies to the questions displayed below.]

Marcelino Co.'s March 31 inventory of raw materials is $82,000. Raw materials purchases in April are $580,000, and factory payroll cost in April is $381,000. Overhead costs incurred in April are: indirect materials, $59,000; indirect labor, $25,000; factory rent, $31,000; factory utilities, $24,000; and factory equipment depreciation, $58,000. The predetermined overhead rate is 50% of direct labor cost. Job 306 is sold for $650,000 cash in April. Costs of the three jobs worked on in April follow.

| Job 306 | Job 307 | Job 308 | ||||||||||

| Balances on March 31 | ||||||||||||

| Direct materials | $ | 28,000 | $ | 36,000 | ||||||||

| Direct labor | 24,000 | 15,000 | ||||||||||

| Applied overhead | 12,000 | 7,500 | ||||||||||

| Costs during April | ||||||||||||

| Direct materials | 139,000 | 205,000 | $ | 100,000 | ||||||||

| Direct labor | 103,000 | 152,000 | 101,000 | |||||||||

| Applied overhead | ? | ? | ? | |||||||||

| Status on April 30 | Finished (sold) | Finished (unsold) | In process | |||||||||

rev: 03_15_2018_QC_CS-121813

Problem 15-1A Part 1

Required:

1. Determine the total of each production cost incurred for April (direct labor, direct materials, and applied overhead), and the total cost assigned to each job (including the balances from March 31).

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Problem 15-1A Part 2

- Materials purchases (on credit).

- Direct materials used in production.

- Direct labor paid and assigned to Work in Process Inventory.

- Indirect labor paid and assigned to Factory Overhead.

- Overhead costs applied to Work in Process Inventory.

- Actual overhead costs incurred, including indirect materials. (Factory rent and utilities are paid in cash.)

- Transfer of Jobs 306 and 307 to Finished Goods Inventory.

- Cost of goods sold for Job 306.

- Revenue from the sale of Job 306.

- Assignment of any underapplied or overapplied overhead to the Cost of Goods Sold account. (The amount is not material.)

2. Prepare journal entries for the month of April to record the above transactions.

Problem 15-1A Part 3

3. Prepare a schedule of cost of goods manufactured.

| |||||||||||||

| Hermon Company, amanufacturing company, produces a single product. Thefollowing | ||||||

| information has been takenfrom the company's production, sales, and cost records for the | ||||||

| just completed year. | ||||||

| Hermon Company | ||||||

| Production in units | 29,000 | |||||

| Sales in units | ? | |||||

| Ending finished goods inventory inunits | ? | |||||

| Sales in dollars | $1,300,000 | |||||

| Costs: | ||||||

| Advertising | $105,000 | |||||

| Entertainment and travel | $40,000 | |||||

| Direct labor | $90,000 | |||||

| Indirect labor | $85,000 | |||||

| Raw materials purchased | $480,000 | |||||

| Building rent (production uses 80% of thespace; | ||||||

| administrative andsales offices use the rest) | $40,000 | |||||

| Utilities, factory | $108,000 | |||||

| Royalty paid for use of production patent,$1.50 | ||||||

| per unit produced | ? | |||||

| Maintenance, factory | $9,000 | |||||

| Rent for special production equipment,$7,000 per | ||||||

| year plus $0.30 perunit produced | ? | |||||

| Selling and administrative salaries | $210,000 | |||||

| Other factory overhead costs | $6,800 | |||||

| Other selling and administrativeexpenses | $17,000 | |||||

| Inventories: | Beginning | End of | ||||

| of the Year | theYear | |||||

| Raw materials | $20,000 | $30,000 | ||||

| Work in process | $50,000 | $40,000 | ||||

| Finished goods | $0 | ? | ||||

| The finished goods inventoryis being carried at the average unit production cost for theyear. | ||||||

| The selling price is $50 per unit. | ||||||

| Required: Use the P3 Solution Sheet | ||||||

| 1. Prepare a schedule of costof goods manufactured for the year. | ||||||

| 2. Compute the following: | ||||||

| a.The number of units in the finished goods inventory at the end ofthe year. | ||||||

| b.The cost of the units in the finished goods inventory at the end ofthe year. | ||||||

| 3. Prepare an income statement for theyear. | show all work | |||||

1. Azucar, Inc. has six processing departments for refining sugarâAffination, Carbonation, Decolorization, Boiling, Recovery, and Packaging. Conversion costs are added evenly throughout each process. Data from August for the Decolorization Department are as follows:

| â | Metric Tons |

| Beginning Work-in-Process Inventory | 0 |

| Transferred in | 13,500 |

| Completed and transferred out to Boiling in August | 5500 |

| Ending Work-in-Process Inventory | 8000 |

| â | Costs |

| Beginning Work-in-Process Inventory | $0 |

| Costs added during August | â |

| Direct materials | 3,000,000 |

| Direct labor | 1,100,000 |

| Manufacturing overhead | 625,000 |

| Total costs added during August | $4,725,000 |

The ending Work-in-Process Inventory is 100% and 75% complete with respect to direct materials and conversion costs, respectively. The weighted-average method is used. Compute the cost per equivalent unit for direct materials and conversion costs. (Round any intermediate calculations and your final answer to two decimal places.)

| A | $81.48 per metric ton for direct materials; $200.00 per metric ton for conversion costs | |

| B | $200.00 per metric ton for direct materials; $81.48 per metric ton for conversion costs | |

| C | $222.22 per metric ton for direct materials; $150.00 per metric ton for conversion costs | |

| D | $222.22 per metric ton for direct materials; $222.22 per metric ton for conversion costs |

2. Martinez Manufacturing incurred $4000 for indirect labor in Department III. The journal entry to record indirect labor utilized, but not paid is ________. Process costing is used.

| A | debit Manufacturing Overhead, $4000; credit Wages Payable, $4000 | |

| B | debit Wages Payable, $4000; credit Manufacturing Overhead, $4000 | |

| C | debit Accounts Payable, $4000; credit Manufacturing Overhead, $4000 | |

| D | debit Manufacturing Overhead, $4000; credit Accounts Payable, $4000 |

3. The managerial role that involves the day-to-day running of the business is the ________.

| A strategic planning function | ||

| B directing function | ||

| C planning function | ||

| D controlling function |

4. Manufacturing costs flow from Work-in-Process Inventory to Cost of Goods Sold to Finished Goods Inventory.

A True

B False

5. Payton Corporation provided the following information for the year:

| Beginning BalanceâWork-in-Process Inventory | $26,000 |

| Ending BalanceâWork-in-Process Inventory | 55,000 |

| Beginning Balanceâ Direct Materials | 81,000 |

| Ending Balanceâ Direct Materials | 59,000 |

| Purchases â Direct Materials | 360,000 |

| Direct Labor | 471,000 |

| Indirect Labor | 19,000 |

| Depreciation on Factory Plant and Equipment | 24,000 |

| Plant Utilities and Insurance | 268,000 |

What was the amount of the cost of goods manufactured for the year?

| A | $1,363,000 | |

| B | $1,164,000 | |

| C | $1,193,000 | |

| D | $1,135,000 |