ACC 406 Lecture Notes - Lecture 5: Corn Chip, International Labor Standards, European Cooperation In Science And Technology

16 Oct 2017

School

Department

Course

Professor

Document Summary

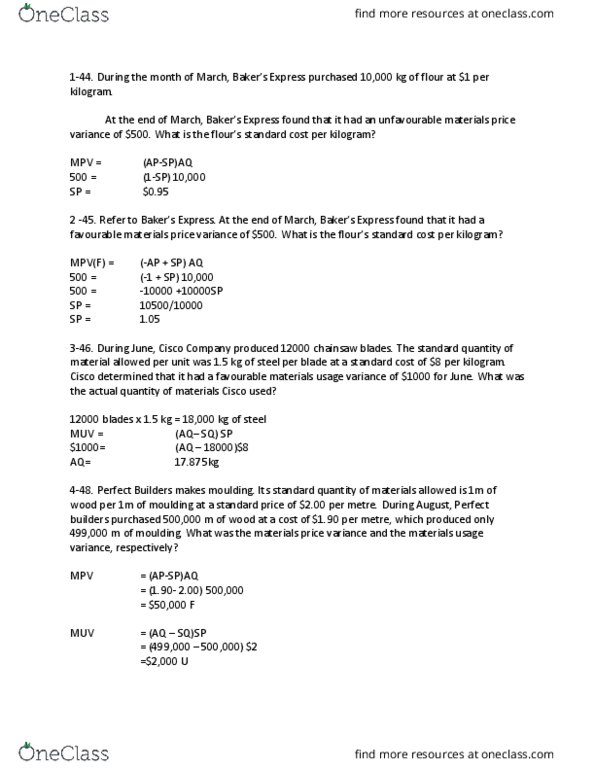

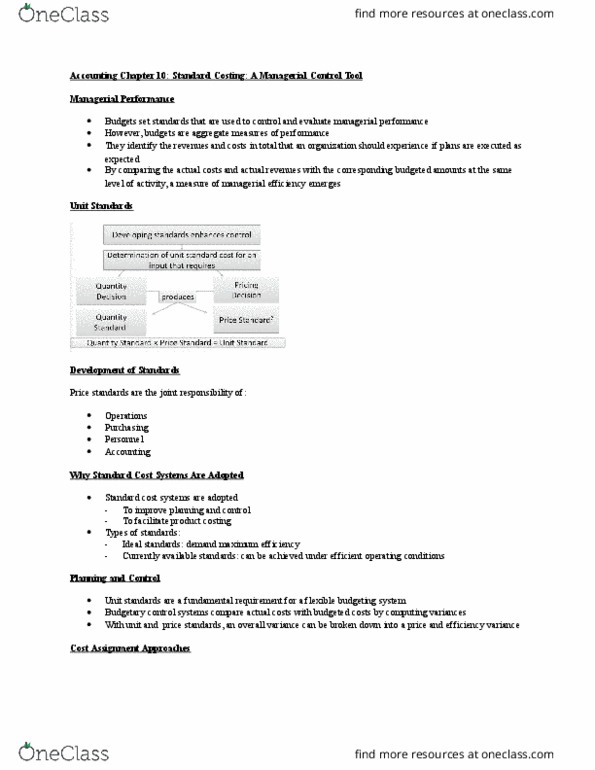

Acc406 chapter 10: standard costing: a managerial control tool. Development of standards: price standards are made by operations, purchasing, personnel and accounting, standard cost systems are used, to improve planning and control, to enable product costing, provides readily available unit cost info, types of standards: Ideal standards demand maximum efficiency: currently available standards can be achieved with efficient operating conditions, from both the standards, currently available standards offer the most behavioural benefits. If standards are too tight, workers become frustrated and performance levels go down: standard cost sheet: (provides the production data needed to calculate standard unit cost) Material variances: price variance belongs to purchasing agent and factors influencing price, quality, quantity discounts, distance of the source from the plant, usage variance belongs to the production manager and factors influencing usage are, scrap, waste, rework. Sp = sh. 018 per 100 grams standard usage = 550 grams per bag actual production = 48500 bags of chips.