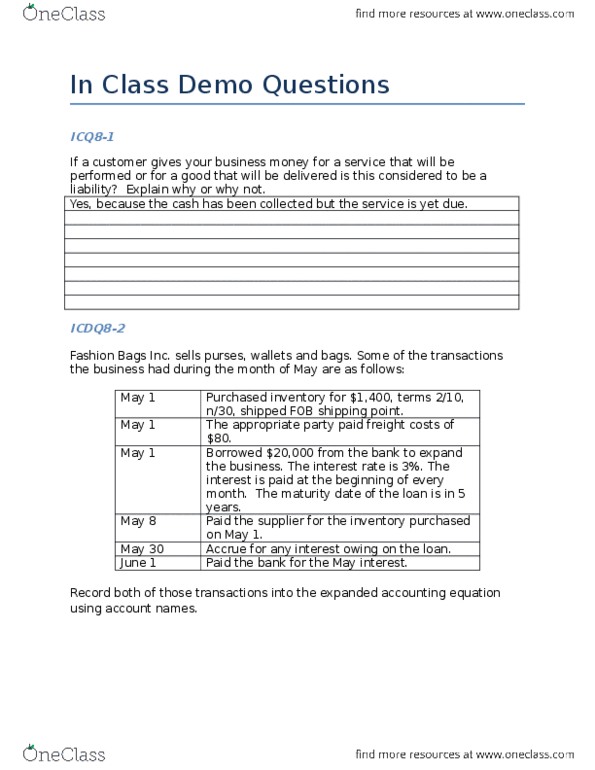

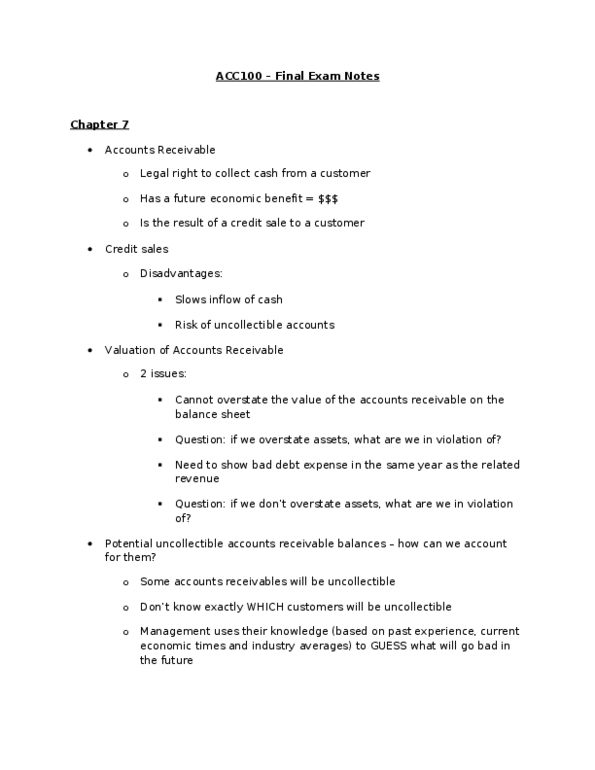

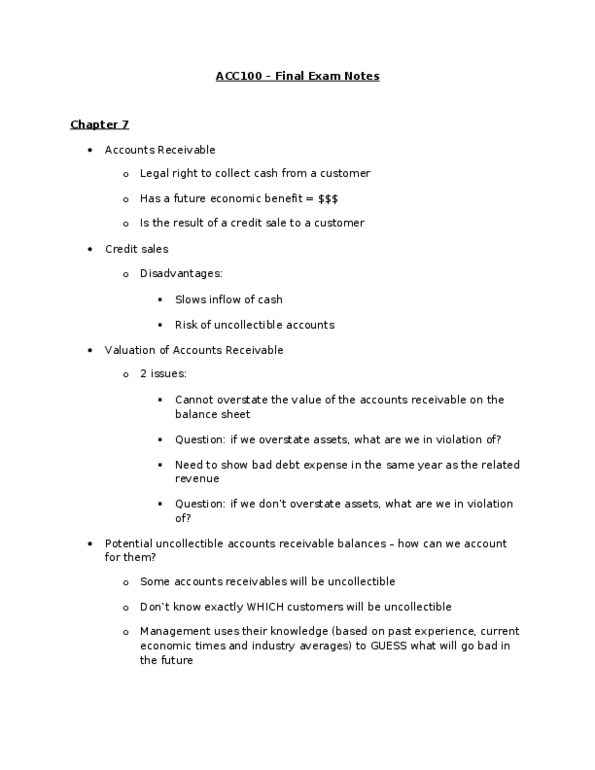

ACC 100 Lecture Notes - Lecture 1: No Entry, Operating Expense, Accounting Software

Document Summary

Get access

Related Documents

Related Questions

Use the following to answer questions 53-56:

The financial statements of Wines, Inc., provide the followinginformation for the current year:

Dec.31 | Jan.1 | |

Accountsreceivable...................................................................... | $210,000 | $180,000 |

Inventory...................................................................... | 200,000 | 190,000 |

Prepaidexpenses....................................................................... | 14,000 | 10,000 |

Accounts payable (formerchandise)................................................................. | 176,000 | 161,000 |

Accrued expensespayable......................................................................... | 13,000 | 19,000 |

Netsales.............................................................................. | 2,900,000 | |

Cost of goodssold............................................................................... | 1,500,000 | |

Operating expenses (including depreciation of$40,000)...................................................................................... | 300,000 |

53. Refer to the above data.Compute the amount of cash received from customers during thecurrent year.

A) $2,900,000.

B) $2,690,000.

C) $2,870,000.

D) Some other amount.

54. Refer to the above data.Compute the amount of Wine's cash payments for purchases ofmerchandise during the current year.

A) $1,500,000.

B) $1,495,000.

C) $1,505,000.

D) Some other amount.

55. Refer to the above data. Compute the amount of Wine's cash paymentsfor operating expenses.

A) $260,000.

B) $270,000.

C) $250,000.

D) Some other amount.

56. Refer to the above data.Wine's net cash flow from operating activities for the current yearis:

A) $1,105,000.

B) $1,375,000.

C) $1,495,000.

D) Some other amount.

57. Alpine Company reported anincrease of $190,000 in its accounts receivable during the year2005. The company's statement of cash flows for 2005 reported $1million of cash received from customers. What amount of net salesmust Alpine have recorded in 2005?

A) $ 810,000.

B) $1,190,000.

C) $1,000,000.

D) $ 190,000

58. When there is an allowancefor doubtful accounts in use, the writing-off of an uncollectibleaccounts receivable will:

A) Reduce income.

B) Reduce an expense.

C) Not change income nor total assets.

D) Increase total assets.

59. The aging of the accountsreceivable approach to estimating uncollectible accounts doesnot:

A) Take into consideration the existing balance in the Allowancefor Doubtful Accounts.

B) Utilize a percentage of probable uncollectibleaccounts for each age group of accounts receivable.

C) Stress the relationship between uncollectibleaccounts expense and net sales.

D) Tend to give a reliable estimate of uncollectible accountsbecause of the consideration given to the collectability ofspecific accounts receivable.

60. Juliet Inc. had accounts receivable of $300,000 and an allowancefor doubtful accounts of $18,500 just before writing off asworthless an account receivable from Arrow Company of $1,200. Thenet realizable values of the accounts receivable before and afterthe write-off were:

A) $281,500 before and $280,300 after.

B) $281,500 before and $281,500 after.

C) $300,000 before and $298,800 after.

D) $318,500 before and $317,300 after.

61. Romeo Inc. had accountsreceivable of $250,000 and an allowance for doubtful accounts of$9,700 just before writing off as worthless an account receivablefrom Juliet Company of $1,500. After writing off this receivablewhat would be the balance in Romeo's Allowance for DoubtfulAccounts?

A) $9,700 credit balance.

B) $10,900 credit balance.

C) $8,200 credit balance.

D) $8,200 debit balance.

62. Sandy Company uses thebalance sheet approach in estimating uncollectible accountsexpense. It has just completed an aging analysis of accountsreceivable at December 31, 2006. This analysis disclosed thefollowing information:

Age | Percentage | |

Group | Considered | |

Total | Uncollectible | |

Not yet due | $51,000 | 1% |

1-30 days past due | $29,000 | 2% |

31-60 past due | $12,000 | 8% |

What is the appropriate balance for Sandy's Allowance for DoubtfulAccounts at December 31, 2006?

A) $92,000.

B) 2% of credit sales in 2006.

C) $1,540.

D) $2,050.

63. At the start of the currentyear, Utopia Corporation had a credit balance in the Allowance forDoubtful Accounts of $1,400. During the year, a monthly provisionof 2% of sales was made for uncollectible accounts. Sales for theyear were $300,000, and $5,200 of accounts receivable were writtenoff as worthless. No recoveries of accounts previously written offwere made during the year. The year-end financial statements shouldshow:

A) Uncollectible accounts expense of $11,200.

B) Allowance for Doubtful Accounts with a creditbalance of $2,200.

C) Allowance for Doubtful Accounts with a creditbalance of $6,600.

D) Uncollectible accounts expense of $5,200.

Peace Corporation acquired 100 percent of Harmony Inc in anontaxable transaction on December 31, 20X1. The following balancesheet information is available immediately following thetransaction: |

Peace Corporation | Harmony Inc | |||||||||||

| BookValue | FairValues | BookValue | FairValues | |||||||||

| Cash | $ | 30,000 | $ | 30,000 | $ | 8,000 | $ | 8,000 | ||||

| Accounts Receivable,net | 50,000 | 50,000 | 12,000 | 12,000 | ||||||||

| Inventory | 75,000 | 82,000 | 7,000 | 10,000 | ||||||||

| Deferred Tax Asset | 8,000 | 1,000 | ? | |||||||||

| Investment inHarmony | 60,000 | 60,000 | ||||||||||

| Equipment, net | 160,000 | 195,000 | 25,000 | 40,000 | ||||||||

| Patent | 0 | 20,000 | ||||||||||

| TotalAssets | $ | 383,000 | $ | 53,000 | ||||||||

| Accounts Payable | $ | 62,000 | $ | 62,000 | $ | 13,000 | $ | 13,000 | ||||

| Accrued VacationPayable | 15,000 | 15,000 | ||||||||||

| Deferred TaxLiability | 6,000 | 2,000 | ? | |||||||||

| Long-Term Debt | 100,000 | 110,000 | 8,000 | 8,000 | ||||||||

| Common Stock | 150,000 | 20,000 | ||||||||||

| Retained Earnings | 50,000 | 10,000 | ||||||||||

| TotalLiabilities and Equity | $ | 383,000 | $ | 53,000 | ||||||||

| AdditionalInformation |

| 1. | The current and future effective tax rate for both Peace andHarmony is 40 percent. |

| 2. | The recorded deferred tax asset for Peace relates to the booktaxdifferences arising from the allowance for doubtful Accounts andthe Accrued vacation payable. The expenses associated with each ofthese amounts will not be deductible for tax purposes until therelated accounts receivable are written off or until the employeevacation is actually paid out. |

| 3. | The recorded deferred tax asset for Harmony is related solely tothe booktax difference arising from the allowance for doubtfulaccounts. |

| 4. | The recorded deferred tax liability in both Peace and Harmonyrelates solely to the booktax differences arising from thedepreciation of their respective equipment. |

| 5. | Accumulated depreciation on the financial accounting records ofPeace and Harmony is $40,000 and $10,000, respectively. |

| 6. | The Harmony patent was identified by Peace in the due diligenceprocess and has not previously been recorded in the accountingrecords of Harmony. |

| 7. | The book and tax bases of all other assets and liabilities ofPeace and Harmony are the same. |

| Required: |

| a. | Compute the tax bases of the assets and liabilities for Peaceand Harmony, where different from the amounts recorded in therespective accounting records. |

| b. | Compute the fair value of the deferred tax assets and deferredtax liabilities for Harmony. |

| c. | Prepare all of the consolidation entries needed to prepare theworksheet for Peace and Harmony at the date of acquisition.(If no entry is required for a transaction/event, select"No journal entry required" in the first accountfield.) |

| d. | Prepare the consolidation worksheet for Peace and Harmony at thedate of acquisition. (Values in the first two columns (the"parent" and "subsidiary" balances) that are to be deducted shouldbe indicated with a minus sign, while all values in the"Consolidation Entries" columns should be entered as positivevalues. For accounts where multiple adjusting entries are required,combine all debit entries into one amount and enter this amount inthe debit column of the worksheet. Similarly, combine all creditentries into one amount and enter this amount in the credit columnof the worksheet.) |