ECON 1P92 Lecture 3: The Measurement of National Income

9 Feb 2018

School

Department

Course

Professor

4

ECON 1P92 Full Course Notes

Verified Note

4 documents

Document Summary

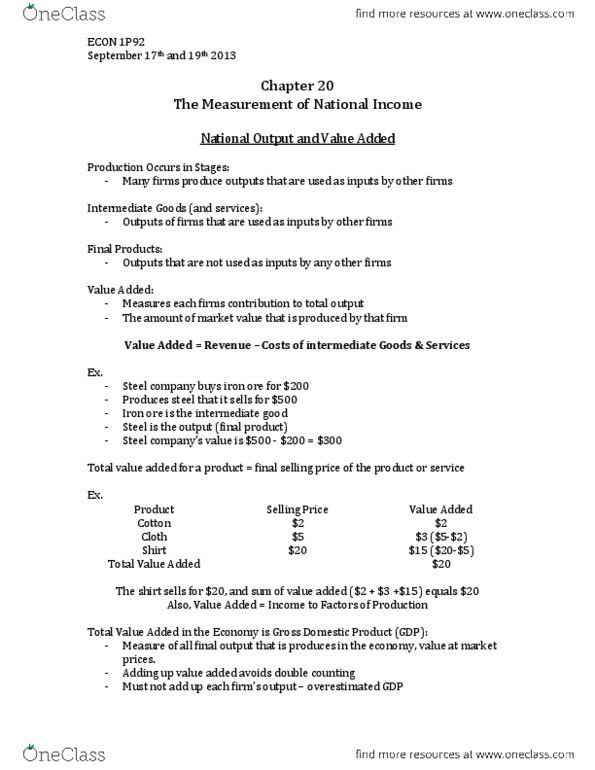

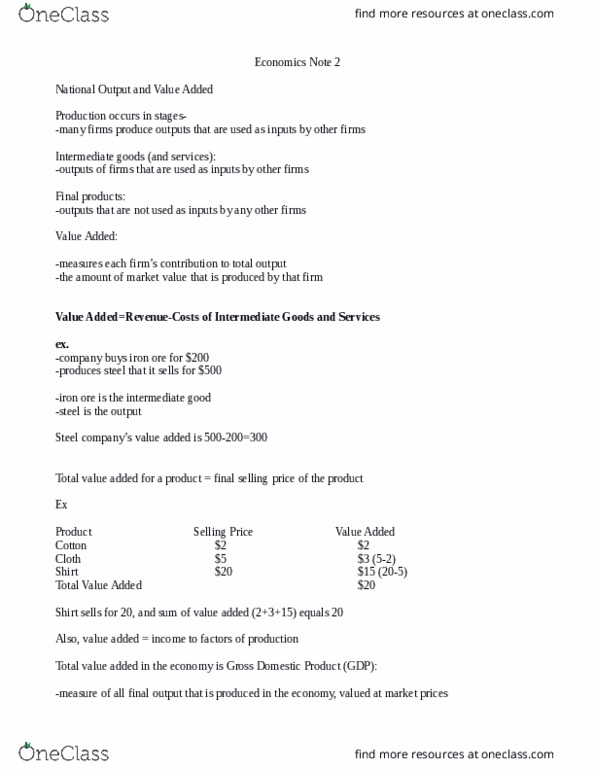

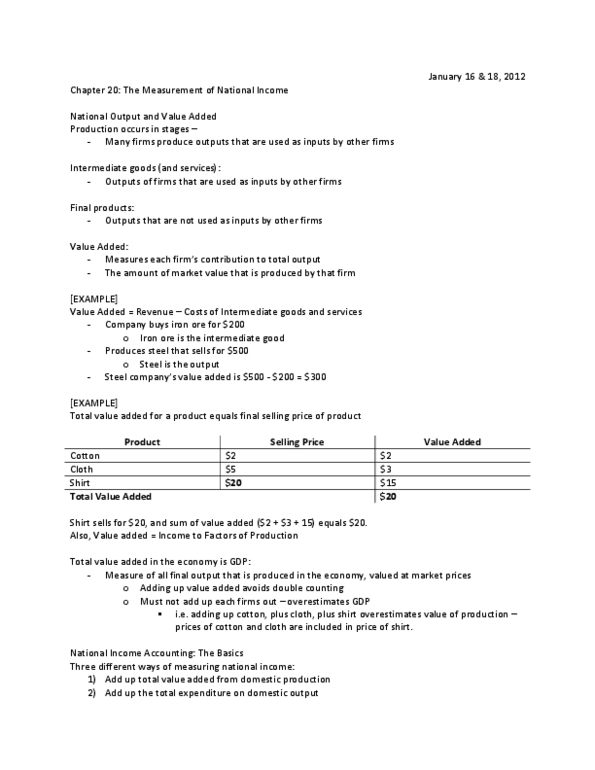

Econ 1p92 - lecture 3 notes: ch 20: the measurement of national income. Many firms produce outputs that are used as inputs by other firms. All outputs that are used as inputs by other producers in a further stage of production. Goods that are not used as inputs by other firms but are produced to be sold for consumption, investment, government, or export during the period under consideration. Measures each firm"s contribution to total outputs. The amount of market value that is produced by that firm. Company buys iron ore for (input/intermediate good) Produces steel that it sells for (product/final good) Total value added for a product = final selling price of the product. Total value of final goods and services produced in the economy during a given period valued at market prices. (market prices of the product/what are we selling it for?) 3 different ways to measuring national income: Add up the total value added from domestic product.