ACTG 1P91 Lecture Notes - Lecture 9: Asset, Intangible Asset, Fixed Asset

31

ACTG 1P91 Full Course Notes

Verified Note

31 documents

Document Summary

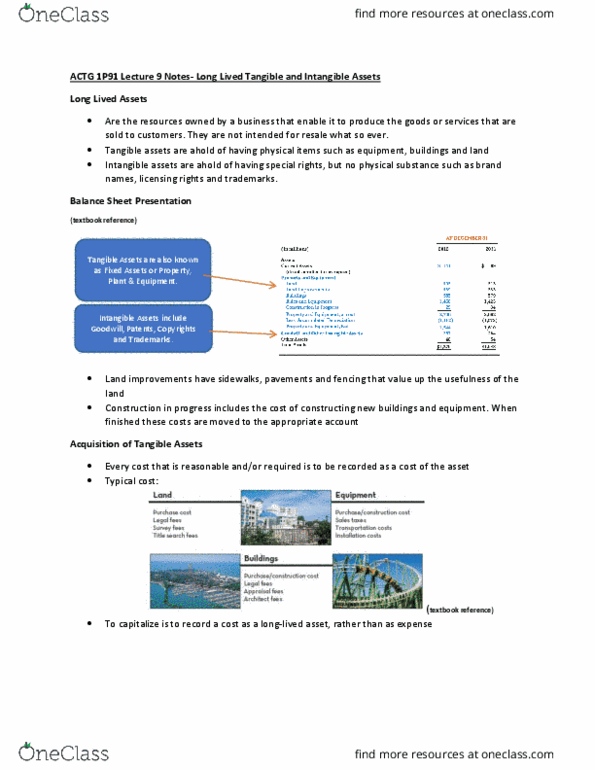

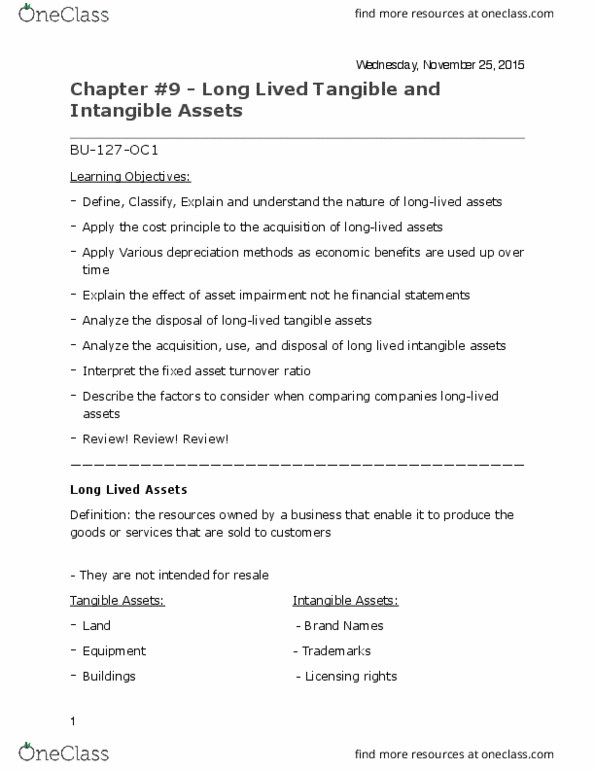

Reporting and interpreting long-lived tangible and intangible assets: chapter 9. The resources owned by a business that enable it to produce the goods or provide the services that are sold to customers. Have special rights, but no physical substance. All reasonable and necessary costs to acquire and prepare an asset for use should be recorded as a cost of the asset. To capitalize is to record a cost as an asset rather than an expense. Purchase cost, legal fees, survey fees, title search fees. Purchase/construction cost, legal fees, appraisal fees, architect fees. Purchase/construction cost, sales taxes, transportation costs, installation costs. Fmv of what was give up if available. Allocate to tangible and limited-life intangibles first. Match expenses to producing revenue to periods when revenue generated. Allocation of cost of tangible fixed asset. Allocation of cost of intangible fixed asset. Two types of maintenance costs can be incurred. Ordinary repairs and maintenance for routine upkeep of long-lived assets.