adms1000 Lecture Notes - Lecture 5: Income Tax, Accounts Receivable, Retained Earnings

Document Summary

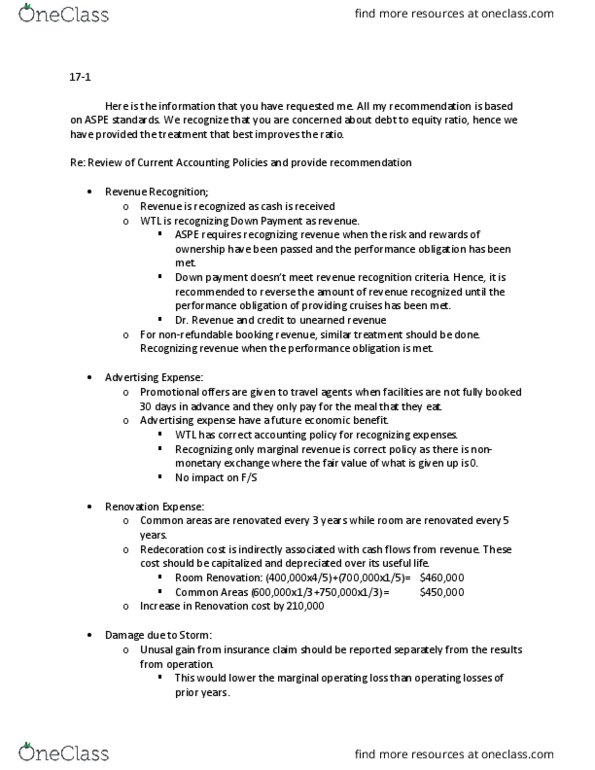

We recognize that you are concerned about debt to equity ratio, and we have provided treatments that best improves the ratios. Here is the information that you have asked me. All my recommendation is based on: revaluation model of land, currently, land is being measured at its historical cost. Increases net income by in 20x13 and in 20x2. Investment properties are currently recorded at its historical cost: fair value model should be used to measure the value of investment. Properties: under fair value model, investment properties are measured at fair value at each reporting period, land should be reported at in 20x13 and in 20x12. Impact: depreciation should be removed from sfp and change in fair value on. 20x12: change in fair value of bonds receivable should be reported in sci. Impact: net income increase by 5 and 10 million in 20x13 and 10x2 respectively. Long term bond receivable note 1 210. 2 205. 2.