16657 Lecture Notes - Lecture 4: Capital Asset Pricing Model, Securities Offering, Market Risk

Document Summary

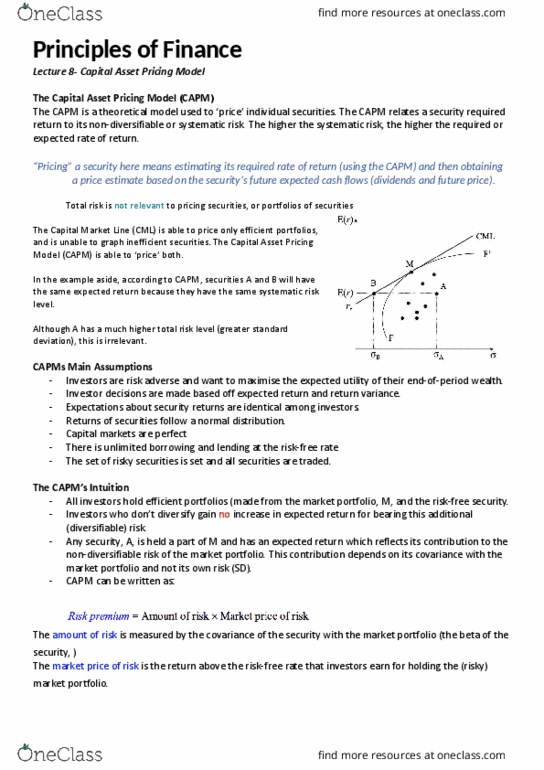

The capital asset pricing model (capm) is a general equilibrium model for the pricing of investments in relation to their risk. It defines the price of a single asset and its risk. The capital market line is established after the establishment of the minimum variance set and the efficient frontier. The assumption here is that the risk-free bond exists and it matures at the end of the time period and is guaranteed by the government. In the context of capm explain the security market line. The graph: x axis is risk in terms of beta, y axis is expected return. Required return = risk free rate of return + beta (market return - risk free rate of return) The sml is frequently used in comparing two similar securities offering approximately the same return, in order to determine which of the two securities involves the least amount of inherent market risk in relation to the expected return.