16655 Lecture Notes - Lecture 1: Relate, Risk Premium, Basis Point

17 Aug 2018

School

Department

Course

Professor

Document Summary

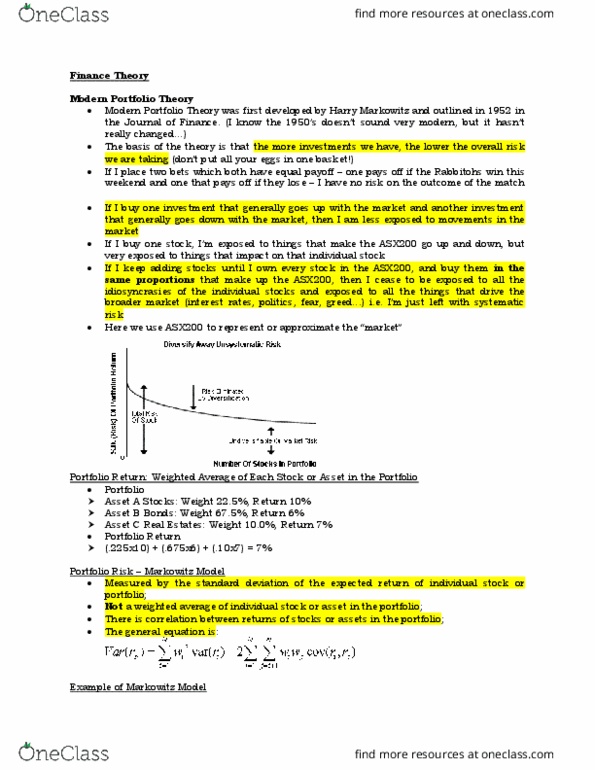

Finance theory: modern portfolio theory, based off the (cid:272)o(cid:374)(cid:272)ept (cid:862)do(cid:374)(cid:859)t put all (cid:455)ou(cid:396) eggs i(cid:374) o(cid:374)e (cid:271)asket(cid:863, the more investments we have, the lower the overall risk we are taking. If i (cid:271)u(cid:455) o(cid:374)e sto(cid:272)k, i(cid:859)(cid:373) e(cid:454)posed to thi(cid:374)gs that (cid:373)ake the a x(cid:1006)(cid:1004)(cid:1004) go up a(cid:374)d do(cid:449)(cid:374), (cid:271)ut (cid:448)e(cid:396)(cid:455) e(cid:454)posed to thi(cid:374)gs that impact on that individual stock unsystematic risk. Portfolio risk markowitz model: measured by the standard deviation of the expected return of individual stock or portfolio, not a weighted average of individual stock or asset in the portfolio, *(see slides for example) Portfolio efficient frontier: efficient portfolios: the ratio whereby the lowest risk is achieved for a given return. Portfolio two-fund theorem: sharpe ratio: the portfolio return less the (cid:396)etu(cid:396)(cid:374) f(cid:396)o(cid:373) the (cid:396)iskless asset (cid:894)o(cid:396) the (cid:862)(cid:396)isk(cid:863) p(cid:396)e(cid:373)iu(cid:373) of the portfolio), divided by the risk of portfolio.