22107 Lecture Notes - Lecture 4: Deferral, Trial Balance, Accounting Information System

Document Summary

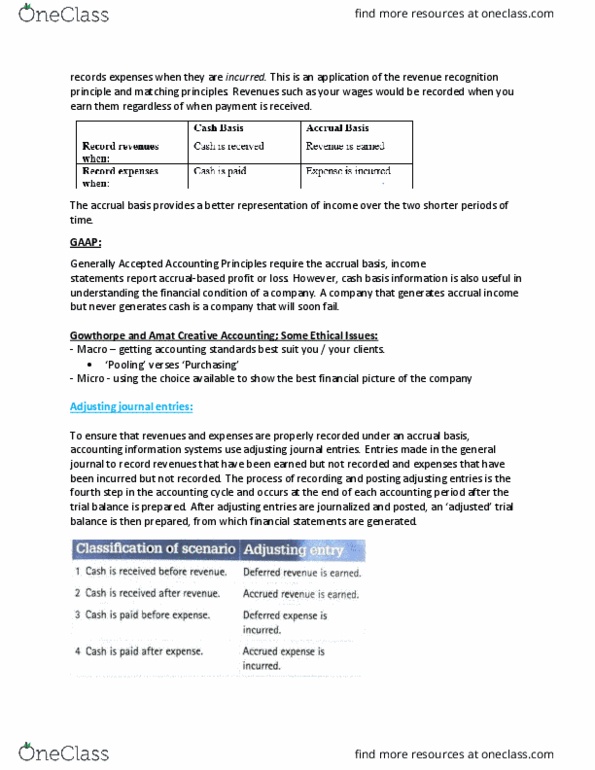

Accrual accounting & adjusting entries: how profit is measured/reported under accrual. Cash basis: records revenues when cash received/expenses paid. Accrual basis: revenues when earned/expenses when incurred is: 4 major circumstances for adjusting journal entries. To ensure revenues/expenses are recorded under accrual basis. Occurs at the end of the period after the trial balance is prepared. Deferred revenue: cash received before revenue earned (liability) Accrued revenue: cash received after revenue earned (receivable) Deferred expense: cash paid before expense is incurred (asset) Accrued expense: cash is paid after expense is incurred (liability: record and post adjusting journal entries. Adjusting journal entries bring the accounts up to date. Involve one asset/liability and one expense/revenue account: prepare an adjusted trial balance and financial statements. Less: accumulated depreciation: closing process and preparing closing entries. Transfer revenue, expenses & dividends back to retained earnings. Each revenue account is reduced to 0 by debiting it/expense credit. Retained earnings = offset account: steps of the accounting cycle.