22107 Lecture Notes - Lecture 7: Accounts Payable, Current Asset, Income Statement

Document Summary

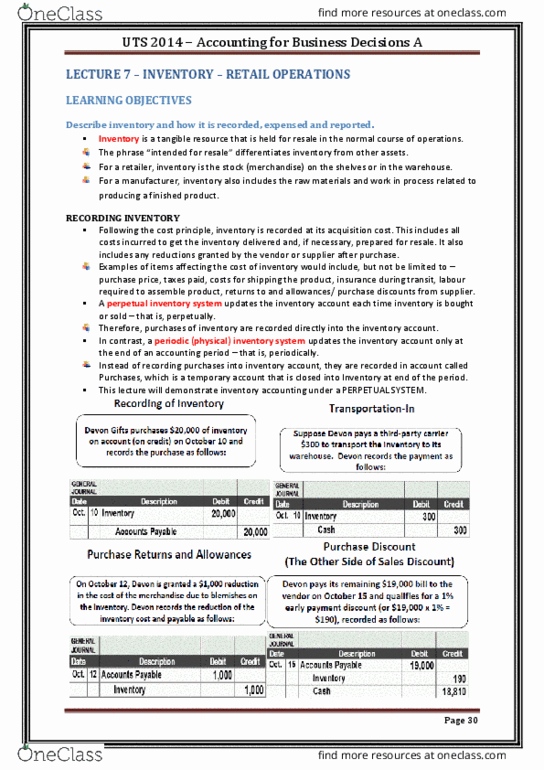

When purchasing inventory on account, inventory (asset) is debited and accounts payable is credited. Costs such as delivery are debited to the inventory account and credited cash. Purchase allowance - reduction in the cost of inventory due to defects. In the case of a purchase allowance, inventory is credited and accounts payable is debited. Inventory becomes an expense when it is sold. Cost of goods sold/ cost of sales is used to capture the amount of inventory expensed during a period. After selling inventory, cash is debited (asset increases), sales increases (revenue). Cogs increases for the cost of the inventory sold, while inventory decreases for the same amount (assets and equity increasing - an expense is a decrease in equity) Reported on balance sheet as a current asset (expected to be sold within a year). Normally reported as a separate line item on the income statement just below sales.