BUSS1030 Lecture Notes - Lecture 10: Fixed Cost, Variable Cost, Opportunity Cost

24 Jul 2018

School

Department

Course

Professor

Document Summary

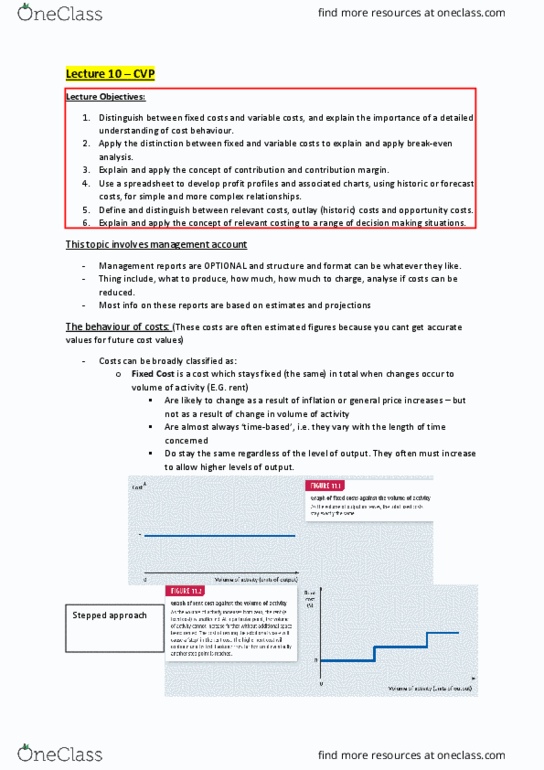

Information is used by managers to make decisions. Distinguish between fixed costs and variable costs, and explain the importance of a detailed understanding of cost behaviour. Apply the distinction between fixed and variable costs to explain and apply break-even analysis. Costs are classified as: fixed cost cost which stays same in total when changes occur to volume of activity eg. rent graph is a horizontal line. Particular points can have sharp rise like steps: likely to change due to inflation or general price increases not result of change in volume activity, almost always time based, stay same regardless of level of output. Cost of heating remains largely fixed but for powering machinery, would increase with production level. Break even analysis: break even point when revenue = cost. Everything above break even point contributes to profit. Break-even point can be calculated as follows: memorise formula.