FIN222 Lecture Notes - Lecture 10: Financial Distress, Retained Earnings, Tax Shield

LECTURE 10.

CAPITAL

STRUCTURE

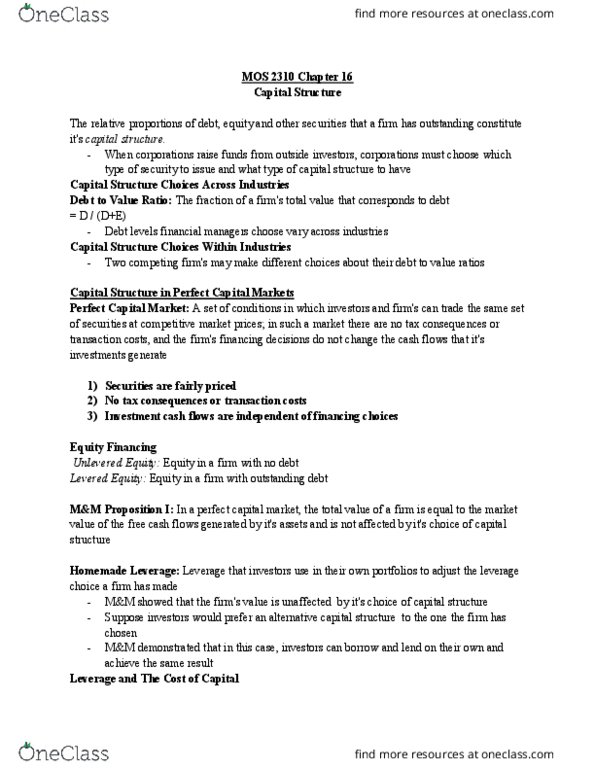

Capital structure

choices

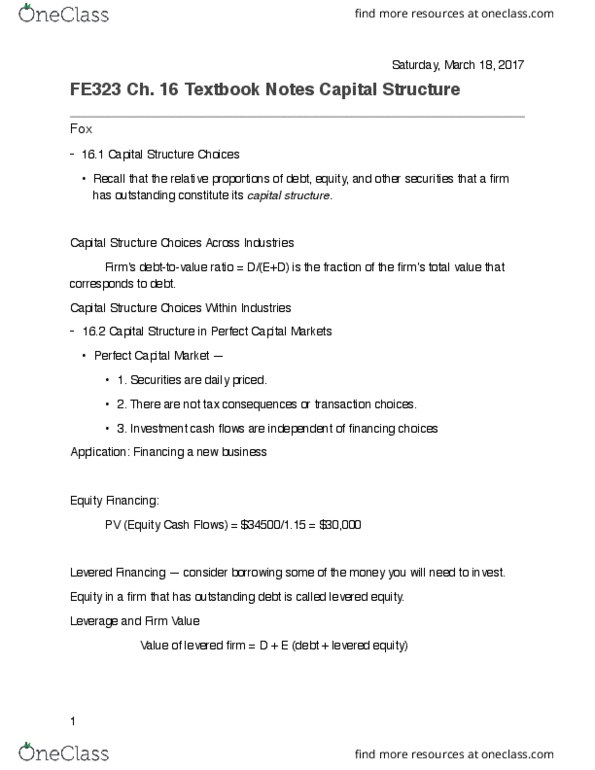

• Capital Structure is the collection of

securities that a firm issues to raise capital

from investors.

• Equity and Debt are securities most

commonly used by firms.

• Various financing choices will promise

different future amounts to each security

holder in exchange for the cash that is raised

today.

• Managers also need to consider whether the

securities that the firm issues will receive a

fair price in the market, have tax

consequences, entail transaction costs, or

even change its future investment

opportunities.

Capital structure

in perfect capital

markets

Perfect Capital Market

• Securities are fairly priced: equivalent

borrowing costs for investors and firms

• No taxes, no transaction costs, no bankruptcy

costs

• Investment CFs are independent of financing

choices

• Symmetry of market information: firms and

investors have the same information

Financing a new business

(in perfect capital

market)

(1) Equity financing: raising money solely by

selling equity. Equity in a firm w/out debt is

called unlevered equity.

(2) Levered financing: consider borrowing some

needed money to invest. Equity in a firm w

outstanding debt is called levered equity.

**Note: ironically, financing a firm

with leverage can make it more

valuable.

Owner of a firm should choose the capital

structure that maximises the total value of

the securities issued.

Leverage and Firm Value

(2)

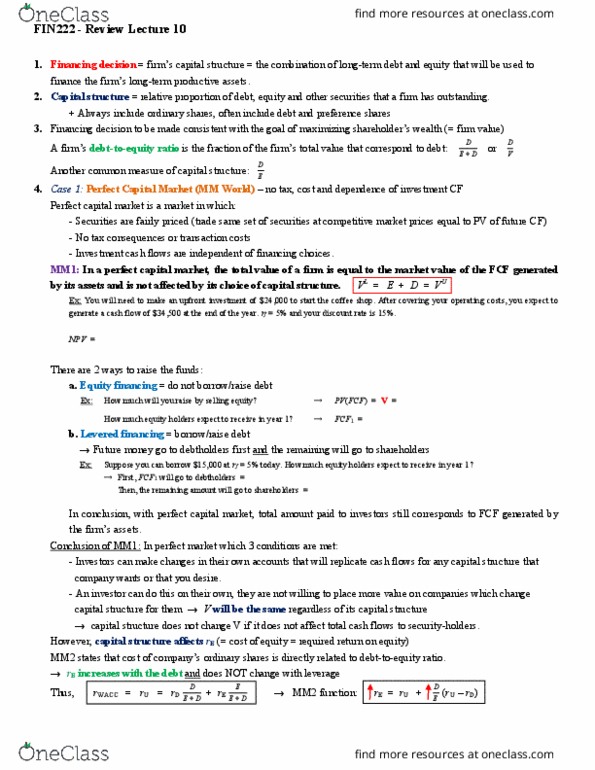

MM Proposition I: In perfect capital market, the

total value of a firm is equal to the market value of

the free cash flows generated by its assets and is not

affected by its choice of capital structure.

𝑉𝐿= 𝐷 + 𝐸 = 𝑉𝑈

When the firm has no debt: CFs paid to

equity holders correspond to the FCFs

generated by the firm’s assets.

When the firm has debt: the CFs are

divided between debt and equity

holders. The total amount, however,

still corresponds to the FCFs generated

by the firm’s assets.

**Notes: WACC is constant for a

given firm, regardless of the capital

structure

Effect of leverage on risk

and return

Leverage increases the risk of equity even when there

is no risk that the firm will default

**Note: the cost of equity rises with

leverage, because the risk to equity

rises with leverage

Homemade Leverage

Home-made Leverage: when investors use leverage

in their own portfolios to adjust the leverage choice

made by a firm.

If investors can borrow/lend at the same interest rates

as the firm (which is true in perfect capital market),

the out-of-pocket cost of securities will be lowered.

Document Summary

Investment cfs are independent of financing choices: symmetry of market information: firms and investors have the same information (1) equity financing: raising money solely by selling equity. Equity in a firm w/out debt is called unlevered equity. (2) levered financing: consider borrowing some needed money to invest. Equity in a firm w outstanding debt is called levered equity. **note: ironically, financing a firm with leverage can make it more valuable. Owner of a firm should choose the capital structure that maximises the total value of the securities issued. Mm proposition i: in perfect capital market, the total value of a firm is equal to the market value of the free cash flows generated by its assets and is not affected by its choice of capital structure. Leverage increases the risk of equity even when there is no risk that the firm will default.