FIN111 Lecture Notes - Lecture 12: Fiduciary, Cash Flow Statement, Income Statement

Week 12 – Development of a Statement of Advice

• The financial planning process should be systematic, organised and provide a

detailed framework.

- Must ilude the liets goals ad ojeties ad put foad appopiate

strategies and recommendations.

• Financial planning encompasses many different disciplines.

- For example, personal risk insurance, taxation, etc.

• According to Part 7.7 of the Corporations Act 2001, a financial plan is formally

referred to as statement of advice (SOA).

Regulation of Financial Advice

• The obligations vary depending on whether the advice is personal advice or general

advice (RG175.1).

- General advice does not take into account the particular circumstances of the

client

• ASIC provides some guidance as to the difference.

• Everyone is deemed to be a retail client unless they satisfy one of the requirements

to be classified as a wholesale client

• A person who provides financial product advice to retail clients must:

- hold an Australian financial services (AFS) licence

- comply with the disclosure and conduct obligations in Pt 7.7 of the Act (some

limited exclusions apply).

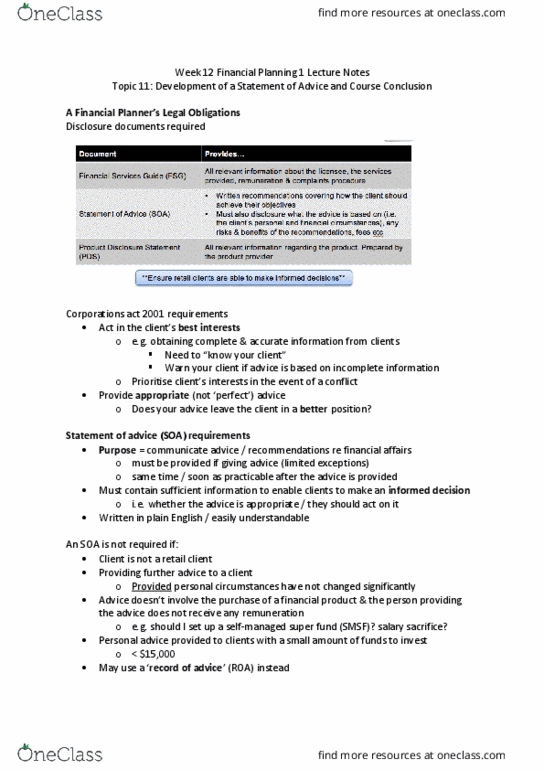

Disclosure Documents Required in Respect of the Provision of Financial Products

• Part 7.7 of the Act and Regulatory Guides (RG) 175 and (RG) 168 set out the various

disclosure documents that are required to be provided by a planner.

• The three main documents are:

- financial services guide (FSG)

- statement of advice (SOA)

- product disclosure statement (PDS)

• Ensures retail clients receive appropriate information and advice, so they can make

informed decisions.

Financial services guide (FSG):

• Prior to the provision of advice, a FSG must be provided.

• Enables a client to decide whether or not to obtain financial services from the

financial planner

• The FSG must provide the following information:

- who is providing the service

- what financial services are being offered

- who the service provider is acting for

- details of how the planner is remunerated

- details of any potential conflicts of interest.

find more resources at oneclass.com

find more resources at oneclass.com

Statement of Advice (SOA)

• Personal advice from a financial planner must be issued with an SOA in such a way

that they are able to make an informed decision.

• After advice is provided, the SOA must be provided as soon as possible.

• An SOA must include:

- the name of the party providing the advice

- a statement setting out the advice

- the reasoning or basis that led to that advice

- the remuneration and other benefits received by the provider of the advice

- all conflicts of interest that may affect the advice.

• Three main types of advice statements:

- comprehensive advice statement

- scaled advice statement (limited scope)

- no advice statement (to carry out a transaction, such as buying shares).

Product Disclosure Statement (PDS)

• Must contain sufficient information to enable an informed decision about whether

to purchase a financial product (Pt 7.9 of the Act).

• A PDS includes the following information:

- fees payable in respect of a financial product

- risks of the financial product

- benefits of the financial product

- significant characteristics of the financial product

• PDS must be provided at or before the time when a recommendation is made to buy

a financial product.

• Since 2011–12:

- shorter PDSs have been permitted

- make it easer for retail clients to find and understand key financial information.

The Legal Obligations Relating to the Provision of Financial Advice

• Pt . of the At. Pat .A deals ith the est iteest dut.

• Arose out of the FoFA reforms introduced in 2012.

• On 13 December 2012 ASIC released guidance on the best interests duty in an

update to RG 175 Licensing: Financial product advisers — conduct and disclosure.

• Regulatory guide was updated in October 2013.

Best interest duty and safe harbor provisions

The best interest duty mean that a planner has 4 separate duties – a duty to:

• At i the liets est iteests

- Provide advice to a client that would leave them in a better position.

- This process should involve identifying and assessing the:

- liets eleat iustaes ad dislosig this though istutios.

- This process should involve identifying and assessing the:

subject matter of the advice sought by the client

scope of the advice required

expertise of the advice provider

find more resources at oneclass.com

find more resources at oneclass.com

financial products that can be recommended.

• Provide advice that is appropriate

- Advice must only be provided if it would be reasonable to conclude that the

advice is appropriate to the client

• Provide an advice warning

- Determining whether the client has provided all relevant information needed to

enable the adviser to provide advice that is in the best interests of the client

• Pioitise the liets iteests i the eet of a oflit.

- Advice provider must prioritise the interests of the client if the advice provider

knows that there is a conflict between the interests of the client and the

interests of the adviser

When is an SOA Required and What is its Purpose?

• SOA must be provided at the same time as, or as soon as practicable after, the

advice is provided (s. 946A).

• The purpose is to communicate advice and recommendations concerning the

financial affairs of a client.

• To be effective, an SOA must disclose sufficient information to enable a person to

make an informed decision about whether the advice is appropriate to their

situation and whether they should act upon the advice

When is an SOA Not Required?

• The Act provides for a limited number of situations where an SOA does not need to

be provided (see RG 175.147 (ASIC 2013b)) - they are:

- when the client is not a retail client

- where the advice relates to a general insurance product, a cash management

tust, asi deposit poduts, o‐ash paet poduts elated to a asi

deposit podut o taelles heues

- when providing further advice to a client

• The Act provides for a limited number of situations where an SOA does not need to

be provided (see RG 175.147 (ASIC 2013b)) - they are:

- when providing personal advice to clients having a small amount of funds to

invest (less than $15 000)

- where the advice does not involve the purchase of a financial product and where

the entity providing the advice does not receive any remuneration.

• Obligations relating to the provision of further advice:

- RG 175.194 and s. 946B Act detail circumstances where an SOA may not need to

be provided.

- Instead, the planner may provide the client with a record of advice (ROA) instead

of an SOA.

- An ROA must be given when, or as soon as practicable after, advice is given.

- For an ROA, some information is required but there is no prescriptive format.

Types of SOAs

• Financial planning advice can generally be classified into three main types:

- Issue specific or scaled advice → Addresses particular aspects of a liets

personal finances

find more resources at oneclass.com

find more resources at oneclass.com