ACCY112 Lecture Notes - Lecture 11: Budget, Accrual, Financial Statement

CHAPTER 12: BUDGETING FOR PLANNING AND CONTROL

I. BUDGET:

a. Definition: a detailed written plan that shows how resources are

expected to be acquired and used during a specified time period to

achieve organisational objectives.

b. A process of preparing a budget is called BUDEGTING. It is an

essential phase of managing a business in an efficient and effective

manner.

c. Ingredients for successful implementation of budgeting:

- Well-defined organisational structure

- Goal congruence

- Management participation & acceptance

- Efficient accounting & reporting system

d. Benefits of Budgeting

1. It forces management to plan ahead and anticipate the future on

a systematic basis.

2. It provides management with realistic performance targets

3. It coordinates the various segments of the organisation and

makes each manager aware how the different activities fit

together

4. It serves as a communication device

5. It furnishes management with motivation

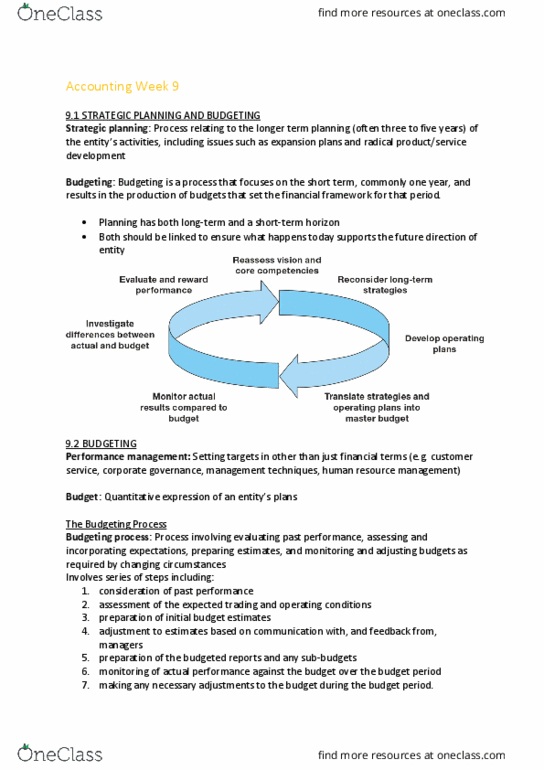

e. Role of budgeting in Financial Planning:

- Main objective of financial phase of budgeting is to identify

how management intends to acquire and use the entity’s

resources to achieve organisational goal.

- A Master budget consisting of several interrelated budgets

provides the basis for financial planning.

f. Major steps in developing a master budget

1. Identify organisational goals for the period

2. Managers develop parts based on accountability

3. Sales for the budget are forecast

4. COGS & operating expenses estimated

5. Capital expenditures identified

6. Accrual accounting converted to cash basis to determine

cash flows

7. Set of budgeted financial statements prepared based on

initial projections

8. Estimated financial performance results compared with

organisational goals

II. OPERATING BUDGETS FOR RETAILING ENTITIES

1. Sales budget

2. Purchases budget

3. Cost of sales budget

4. Selling and distribution expenses budget

5. Administrative expenses budget

6. Finance and other expenses budget

7. Budgeted income statement

III. OPERATING BUDGETS FOR MANUFACTURING

ENTITIES

1. Sales budget

2. Production budget

3. Direct materials budget

4. Direct labour budget

5. Factory overhead budget

6. Cost of sales budget

7. Selling and distribution expenses budget

8. Administrative expenses budget

9. Finance and other expenses budget

10. Budgeted income statement

IV. EXAMPLE:

a. Marco manufacturing is preparing a master budget for the period

from 1 July to 30 September 2018 and has complied the following

data.

The firm sells a single product at a price of $80 per unit. The sales

forecast (in units) prepared by the marketing department for April

2018 to December 2018 is as follows:

Prepare sales budget for the quarter ending 30 September 2018

BUDGETED PRODUCTION (Units)

find more resources at oneclass.com

find more resources at oneclass.com

= Budgeted sales (units) + Target ending finished goods

inventory (units) – beginning finished goods inventory (units)

2) Production Budget: The ending finished goods inventory should equal

to 50% of the sales requirements of the next two months.

The beginning inventories on 1 July 2018 is 3,000 units

Required:

Prepare production budget for the quarter ending 30

September 2018

3) Direct Material Budget: Each finished unit requires 2 kgs of direct

materials at a cost of $2.50 per Kg.

• Desired ending inventory equals 20% of the materials required to

produce next month’s sales.

• The beginning materials inventory on 1 July 2018 is 1,280

kilograms.

Required: Prepare direct materials budget for the quarter ending 30

September 2018.

4) Direct Labour Budget: Each unit requires 3 direct labor-hours at $8.00

per hour.

Required:

Prepare direct labour budget for the quarter ending 30 September

2018.

5) Factory Overhead Budget: Variable overhead is budgeted at $4.00 per

direct labor-hours required.

Fixed overhead is budgeted at $25,000 per month (including

monthly depreciation $5,000)

Required: Prepare factory overhead budget for the quarter ending 30

September 2018.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

It is an essential phase of managing a business in an efficient and effective manner. Efficient accounting & reporting system: benefits of budgeting. It forces management to plan ahead and anticipate the future on a systematic basis. It coordinates the various segments of the organisation and makes each manager aware how the different activities fit together. It furnishes management with motivation: role of budgeting in financial planning: Main objective of financial phase of budgeting is to identify how management intends to acquire and use the entity"s resources to achieve organisational goal. A master budget consisting of several interrelated budgets provides the basis for financial planning: major steps in developing a master budget. Entities: sales budget, production budget, direct materials budget, direct labour budget, factory overhead budget, cost of sales budget, selling and distribution expenses budget, administrative expenses budget, finance and other expenses budget, budgeted income statement.