FINS3630 Lecture Notes - Lecture 6: Liquidity Risk, Money Market Account, Monetary Policy Of The United States

Liquidity Risk

- Liability side liquidity risk: demand deposits (core deposits), money market deposits,

transaction accounts

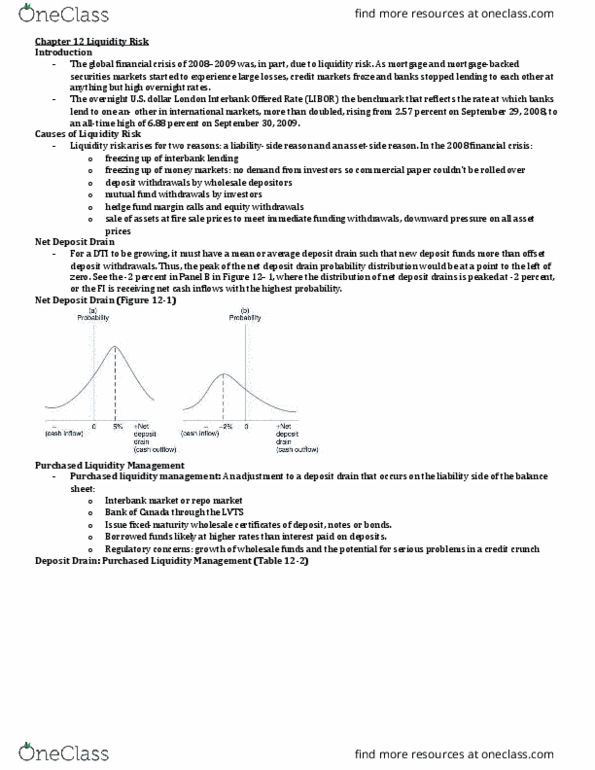

o Net deposit drain = deposit withdrawals – deposit additions

o Purchased liquidity management: interbank market for ST loans (market for

purchased funds) – allows DI to maintain overall BS size w/out disturbing

size/composition of A

▪ Can insulate A side of BS from normal drains on L side of BS

o Stored liquidity mgmt.: liquidate A utilising stored liquidity (use cash as liquidity

adjustment mechanism

- Asset side liquidity risk: loan commitments drawn

- Liquidity index: , P= fire-sale price, P*= fair market price

- Financing gap = avg loans – avg deposits

= borrowed funds (or financing requirements) – liquid assets

- Liquidity regulation: liquidity coverage ratio, net stable funds ratio

→

remain liquid stress + unencumbered

Total net outflow over next 30 calendar days = outflows – min(inflows, 0.75 of outflows)

- Net stable funding ratio: ensure LT assets are funded w min amount of stable liabilities (limit

reliance on ST wholesale funding)

o Available stable funding: bank cap, preferred stock/liab (maturity>1yr), portion of

retail/wholesale depo expected to stay w bank during period of idiosyncratic stress

- ASF factor: equity and liabilities into 5 categories- amount assigned to each category * ASF

factor= weighted sum total ASF

- RSF factor: assets into 5 categories amount assigned to each category * RSF factor= weighted

sum total RSF

- Monitoring issues:

find more resources at oneclass.com

find more resources at oneclass.com

find more resources at oneclass.com

find more resources at oneclass.com

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

: liquidate a utilising stored liquidity (use cash as liquidity adjustment mechanism. Asset side liquidity risk: loan commitments drawn. Financing gap = avg loans avg deposits. , p= fire-sale price, p*= fair market price. = borrowed funds (or financing requirements) liquid assets. Liquidity regulation: liquidity coverage ratio, net stable funds ratio remain liquid stress + unencumbered. Total net outflow over next 30 calendar days = outflows min(inflows, 0. 75 of outflows) Asf factor: equity and liabilities into 5 categories- amount assigned to each category * asf factor= weighted sum total asf. Rsf factor: assets into 5 categories amount assigned to each category * rsf factor= weighted sum total rsf. High liquidity, low default risk assets lower returns. Limit liquidity/default risk of di, regulators have imposed a minimum liquid asset reserve requirement. Monetary implementation reasons multiplier, rr= reserve requirement ratio m= money market.