FINS3630 Lecture Notes - Lecture 7: Reinvestment Risk, Monetary Policy Of The United States, Investment

FINS3630 Notes

Lecture 5: Interest Rate Risk (I)

- etral aks atio targeted at “T rates, feed through to hole ter struture of I‘

- increased financial M integration- irease speed ad assoiated olatilit of I‘ ∆

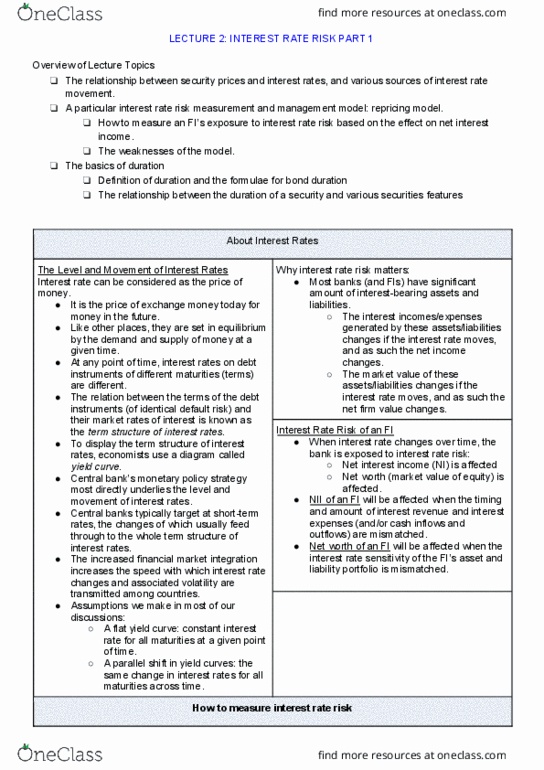

- IR: price of money

- Relation between TERMS of debt instruments of IDENTICAL DEFAULT RISK and their MARKET IR is

known as TERM STRUCTURE OF IR → yield curve

- Asset transformation results in mismatch of asset/liability maturities: interest spread = IR risk

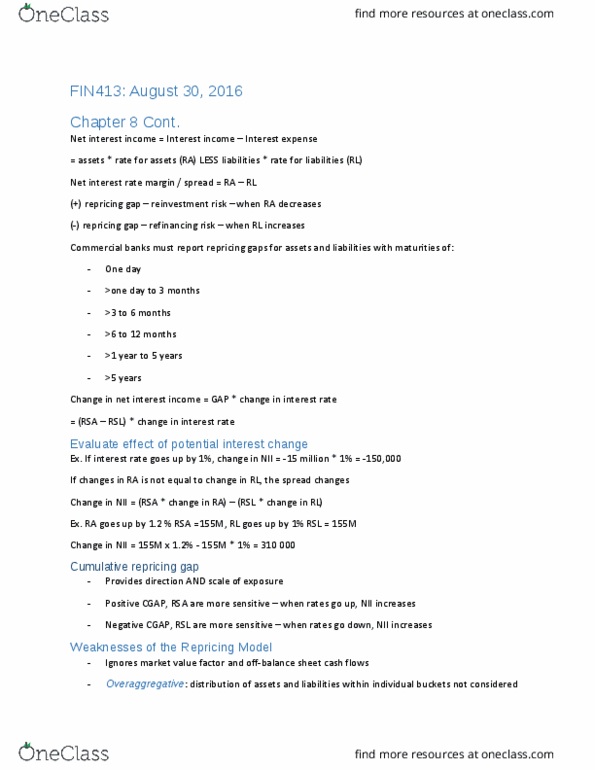

o Net interest income (NII): Repricing Model

o Net worth (market value of equity): Duration Model

- ‘efiaig risk I‘ for orro ∆- liabilities)

- ‘eiestet risk I‘ for iest ∆- assets profit spread

- Repricing model

o Repricing gap: difference between amounts of A and L whose IR will be repriced or

changed over some fut period → proides a easure of a FIs NII eposure to I‘ ∆ i

different maturity buckets

▪ Risk sensitive assets (RSA) vs. risk sensitive liabilities (RSL)

o Result of: rollover of A/L (loan paid off prior/at maturity and funds used to issue new loan

at current market rates) OR variable rate A/L instrument

1 Identifying A/L that will be repriced over maturity bucket

2 Annualised change in NII (IR quoted on pa basis)- assumes RSA/RSL repriced at same time

- Negative repricing gap (RSA<RSL) exposes the bank to refinancing risk in that a rise in IR would

lower NII

o Projecting a decrease in IR, maintain negative repricing gap increase NII

- Positive repricing gap (RSA>RSL) exposes the bank to reinvestment risk in that a drop in IR would

lower NII

o Projecting an increase in IR, maintaining positive repricing gap increase NII

- Cumulative gap: sum repricing gaps over longer period

- RSA: ST consumer loans, 3-month T bills, 6m T notes, 30-year gloating rate mortgages

- RSL: 3m CDs, 3m bank accepted, 6m commercial papers, 1year time deposits

- Demand deposits and passbook savings accounts = rate insensitive (core deposits)

o IR on demand deposits = 0 by regulation, IR on these do not fluctuate w changes in general

level of IR

o Inclusion in rate sensitive: when IR rise, indiv may draw down their demand deposits and

move money to alternative instruments paying higher interests, forcing the bank to

replace them w more expensive fund substitutions

- IR sensitivity as % of assets: CGAP/Assets → direction of IR exposure + scale of exposure

- Gap ratio: RSA/RSL → >1 exposed to refinancing risk, <1 exposed to reinvestment risk

-

- spread effet st ∆ i spread is +el related to ∆ NII

- when CGAP and Spread effects work in opposite directions, ∆NII aot e predited /out

koig size of CGAP ad ∆spread

- repriig odel: igore MV effets of I‘ ∆ assue BV approah – PV of CF o A/L ∆ + iediate

iterest reeied/paid ∆s

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lecture 5: interest rate risk (i) (cid:272)e(cid:374)tral (cid:271)a(cid:374)k(cid:859)s a(cid:272)tio(cid:374) targeted at t rates, feed through to (cid:449)hole ter(cid:373) stru(cid:272)ture of i increased financial m integration- i(cid:374)(cid:272)rease speed a(cid:374)d asso(cid:272)iated (cid:448)olatilit(cid:455) of i . Relation between terms of debt instruments of identical default risk and their market ir is known as term structure of ir yield curve. Asset transformation results in mismatch of asset/liability maturities: interest spread = ir risk: net interest income (nii): repricing model, net worth (market value of equity): duration model. Efi(cid:374)a(cid:374)(cid:272)i(cid:374)g risk (cid:894)i for (cid:271)orro(cid:449) - liabilities) Ei(cid:374)(cid:448)est(cid:373)e(cid:374)t risk (cid:894)i for i(cid:374)(cid:448)est - assets (cid:858)profit spread(cid:859)(cid:895) Identifying a/l that will be repriced over maturity bucket. 2 annualised change in nii (ir quoted on pa basis)- assumes rsa/rsl repriced at same time. Negative repricing gap (rsa