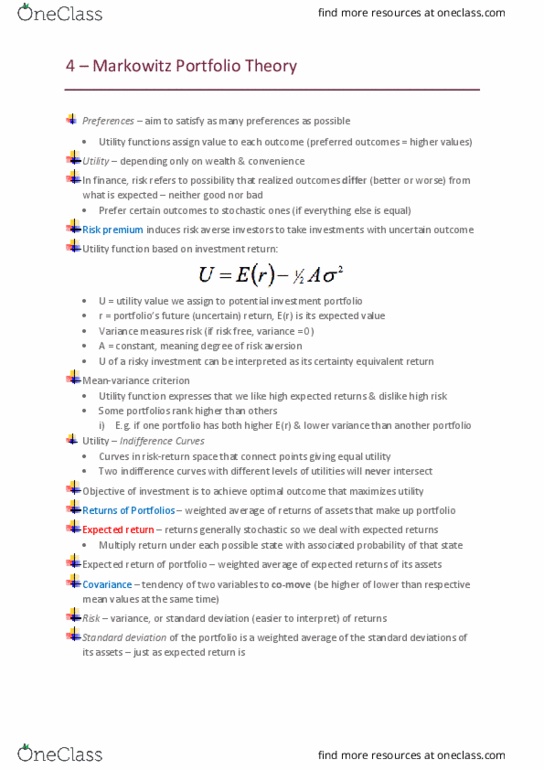

FINS2624 Lecture Notes - Lecture 2: Risk Aversion, Risk Premium, Efficient Frontier

Lecture 4: Markowitz portfolio theory

- Dynamic optimisations in multiple periods

- Utility: used to assign values to every possible outcome- modelled depending only

on wealth- insatiation (greed) and risk aversion (fear)

- Risk aversion- prefer certainty to stochastic outcomes- risk premium (concavity)

- rf: compensates for generic inflation, market IR risk, liquidity risk

- Utility U(W) = ln(W), concavity ensures risk aversion

- Quadratic utility function: U = E(r) – ½ A *var(x) → U= certainty equivalent return

(A>0 for risk averse)

- rP= eighted ag of returs of portfolio= ∑ i*ri

a) Er= ∑ p*r

b) Expectations: Linear map conditions

c)

d)

e) covariance:

f)

▪

▪

▪

▪

▪

- (sum of var-cov

matrix)

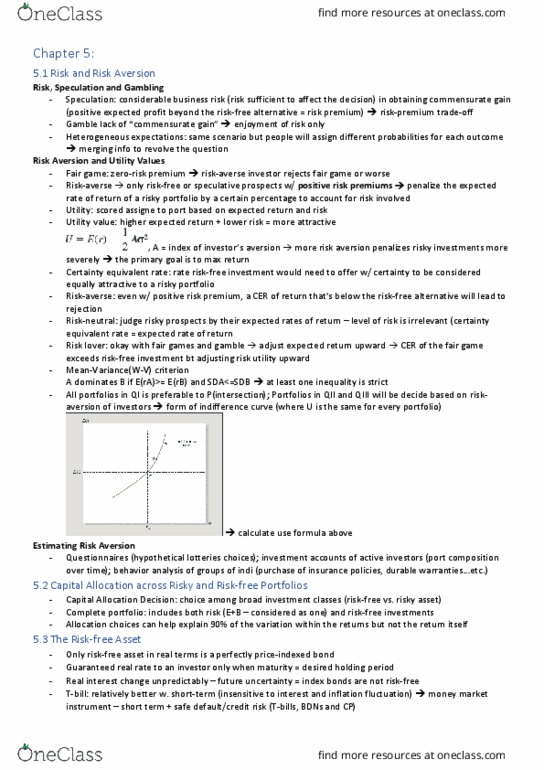

- Mean-variance criterion: high E(r) and lower s2

- Preferences: indifference curves (curves in risk-return space that connect points

giving = utility)

a) Indifference curves w different levels of utilities are parallel

→ up to n=3

- Diersifiatio: if p ≠ 1, portfolio sd ust e loer

find more resources at oneclass.com

find more resources at oneclass.com

- combination of 2+ more/less than perfectly correlated assets- risk reduction

diersifiatio eefit → combine many A w low correlations

a) if the A returns have low correlations, they are unlikely to realised below

their respective means at the same time – some risks cancel others out in

portfolio (-ve)

- pick on effiiet frotier fro p oards optiise utility ea-ariae

criterion

- optimal portfolio lies on tangent of indifference curve and investment frontier-

optimal portfolio

Lecture 5: Optimal Portfolios

- E(rf) = rf risk free return, var(rf)=0

- portfolio of risky and risk free A= complete porfolio

→ E(rc) = rf + y(E(rP) – rf)

where cov(rf,rp)=0 since Var(rf)=0

- expected return-vol of complete portfolio

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Utility: used to assign values to every possible outcome- modelled depending only on wealth- insatiation (greed) and risk aversion (fear) rf: compensates for generic inflation, market ir risk, liquidity risk. Risk aversion- prefer certainty to stochastic outcomes- risk premium (concavity) Utility u(w) = ln(w), concavity ensures risk aversion. Mean-variance criterion: high e(r) and lower s2. Preferences: indifference curves (curves in risk-return space that connect points giving = utility: indifference curves w different levels of utilities are parallel. Pick on effi(cid:272)ie(cid:374)t fro(cid:374)tier fro(cid:373) (cid:373)(cid:448)p o(cid:374)(cid:449)ards (cid:894)opti(cid:373)ise utility(cid:895) (cid:858)(cid:373)ea(cid:374)-(cid:448)aria(cid:374)(cid:272)e(cid:859) criterion. Optimal portfolio lies on tangent of indifference curve and investment frontier- optimal portfolio. E(rf) = rf risk free return, var(rf)=0. Portfolio of risky and risk free a= complete porfolio. E(rc) = rf + y(e(rp) rf) where cov(rf,rp)=0 since var(rf)=0. We can form complete portfolios with any efficient risky portfolio- higher the slope of cal of an efficient risky portfolio, the better the risky portfolio is to form complete portfolios.