FINS1613 Lecture Notes - Lecture 6: International Accounting Standards Board, Financial Accounting Standards Board, Capital Budgeting

Wednesday, 5 April 2017

Business Finance

Capital Budgeting

-Financial Statements:

•Accounting boards provide rules by which corporations prepare financial statements

-Australian Accounting Standards Board

-International Accounting Standards Board (IASB)

-Financial Accounting Standards Board (U.S.)

•Auditors are neutral third parties that verify annual statements

-Attest that statement is prepared according to rules

-Provide evidence that information is available

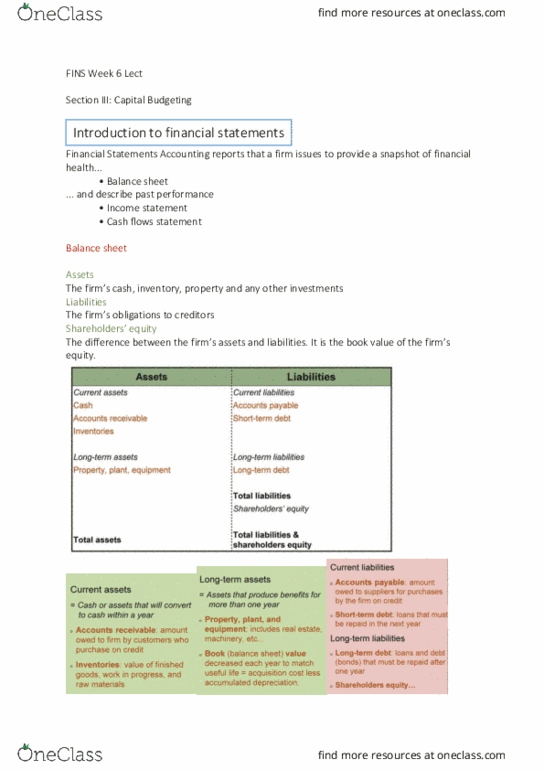

-Balance Sheet:

•Snapshot of a firm’s financial assets & liabilities at a single point in time

•Assets: Firm’s cash, inventory, property & any other investments

-Current assets can be converted to cash within a year

•Accounts receivable - amount owed by customers who purchase on credit

•Inventories - value of finished goods, work in progress & raw materials

-Long-term assets produce benefits for more than one year

•Property, plant & equipment - includes real estate, machinery etc

•Book value (balance sheet value) decreased each year to match assets useful

life - equal to acquisition cost less accumulated depreciation

•Liabilities: Firm’s obligations to creditors

-Current liabilities

•Accounts payable - amount owed to suppliers for purchases by firm on credit

•Short-term debt - loans that must be repaid in next year

-Long-term liabilities

•Long-term debt - loans & debt (bonds) that must be repaid after one year

-Liquidation: Process of closing a firm by selling its assets & paying its liabilities

!1

find more resources at oneclass.com

find more resources at oneclass.com

Wednesday, 5 April 2017

•Shareholders’ equity: Difference between firm’s assets & liabilities (book value of

firm’s equity)

-Represents net worth of firm from accounting perspective

-Estimate of the liquidation value of the firm

-Not the market value of the firm (the value to investors) because it is a snapshot

in time & ignores potential future earnings

•Balance Sheet Identity: Assets = Liabilities + Shareholders’ Equity

-Income Statement:

•Lists firm’s revenues & expenses over a period of time

•Net profit is a measure of firm profitability over the period

-Aka ‘bottom line’, net income, earnings

•Determined using rules of accrual basis accounting

-Revenues & expenses matched & recognised when incurred, not when paid

-Cash Flow Statement:

•Lists all cash generated by a firm & how cash has been allocated over a period of

time

-Operating activities - main activities of firm

-Investing activities - capital expenditures, acquisitions

-Financing activities - dividend payments, net borrowing

•Determined using rules of cash basis accounting

-Revenues & expenses recognised when paid

-Preparing Basic Financial Statements for Project Evaluation:

•Income Statement determined using rules of accrual basis accounting

-Property, plant & equipment depreciated over time - matches long-term life to

period of use

-Taxes are based on Earnings before Interest & Taxes (EBIT)

•Debt payments ignored when evaluating projects

•Tax benefits of debt addressed through appropriate discount rate

!2

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Financial statements: accounting boards provide rules by which corporations prepare nancial statements. Financial accounting standards board (u. s. : auditors are neutral third parties that verify annual statements. Attest that statement is prepared according to rules. Balance sheet: snapshot of a rm"s nancial assets & liabilities at a single point in time, assets: firm"s cash, inventory, property & any other investments. Current assets can be converted to cash within a year: accounts receivable - amount owed by customers who purchase on credit, inventories - value of nished goods, work in progress & raw materials. Current liabilities: accounts payable - amount owed to suppliers for purchases by rm on credit, short-term debt - loans that must be repaid in next year. Long-term liabilities: long-term debt - loans & debt (bonds) that must be repaid after one year. Liquidation: process of closing a rm by selling its assets & paying its liabilities. !1: shareholders" equity: difference between rm"s assets & liabilities (book value of.