FINS1613 Lecture Notes - Lecture 8: Dividend Imputation, Efficient-Market Hypothesis, Dividend Tax

Part IV: Payout Policy and Free Cash Flow Models

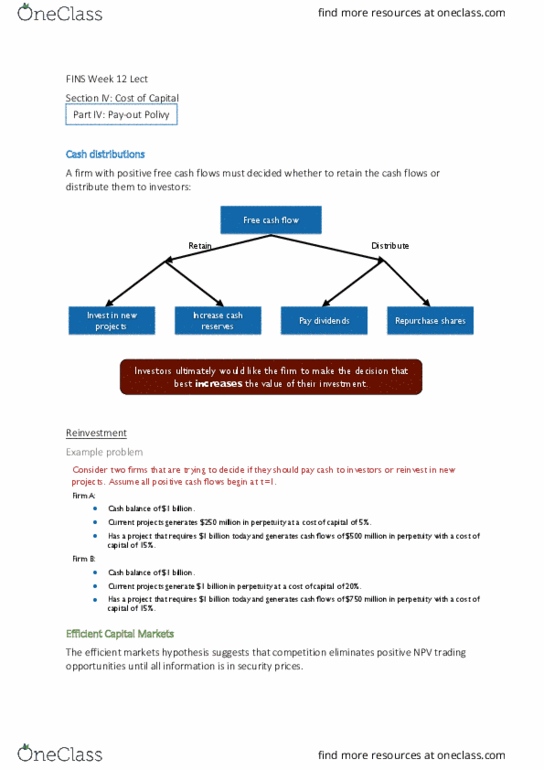

- FCF → retain (invest in new projects or increase cash reserves) OR distribute (pay

dividends or repurchase shares) → best increases value of ownership in the firm

- Retain or payout? (how security prices are set?)

o Information (private/difficult to interpret arbitrage- eventually reflected in

security prices)- efficient markets hypothesis: competition eliminates positive

NPV trading opportunities until all information is in security prices (best

estimate of the discounted value of expected future CF)

- PCM: tax, administration, security prices, costs, financing decision indep of CF

- MM payout irrelevance: in PCM, if a firm invests excess CF in financial securities, the

hoie of payout ersus retetio is irreleat ad doest affet iitial alue of the

firm

o In PCM- all investments have 0 NPV and payouts are untaxed- doest atter

whether firm or owners purchase securities

- Imperfect CM:

Payouts: Dividends and repurchases in PCM

- Before ex-dividend date: (date at which you are entitled to receive dividend) (cum

div)

o P = (cash + project)/shares outstanding

o P = current div + PV(fut div)

- After ex dividend date:

o P = project/shares outstanding

o Div = cash/shares outstanding

o Total value on ex-dividend date to shareholder = 6.8 (in PCM: share price falls

by amount of dividend)

- Issue equity to finance a larger dividend (all options, NPV =)

find more resources at oneclass.com

find more resources at oneclass.com

- Repurchase shares: P before repo: P(B) = (cash + PV(project))/ shares outstanding

o Share repo = cash/P(B)

o New shares outstanding = original shares outstanding – share repo

o Price after repo: P(A) = PV(project)/new shares outstanding

▪ Share repo through a stock exchange available to all shareholders

(open market repo) has no effect on share P

▪ When firm repo, supply of shares reduces + value of firm assets

declines when it spends its cash to buy the shares (at market price-

effects offset)

- Open market repurchase: when firm repurchases its own shares by buying them on

the open market over time

- Off-market buyback: firm invites its shareholders to offer to sell their shares back to

the firm by way of a tender process

- Dutch auction: share repo method in which shareholders indicate how many shares

they are willing to sell at each price. The firm then pays the lowest price at which it

can buy back its desired # of shares

- Selective buyback: firm offers to repo shares directly from only 1/some of

shareholders

find more resources at oneclass.com

find more resources at oneclass.com

Taxes

- Franking credit: a tax credit transfer to shareholders for the amount of tax the

company has paid in an imputation tax system. The franking credit is used by

shareholders to reduce his or her own tax liability, with any excess paid back as a

refund. Only available to resident tax payers in AUS

- Dividend tax depends on tax system: classical (personal tax based on after-tax

dividends to a shareholder) + imputation (personal tax based on pre-tax net profit w

a credit for corporate tax)

Tax on dividends:

o NP before tax → corporate tax → net profit after tax (same for both classical

and imputation)

▪ → dividend before tax → taxable income → personal tax → franking

credit for imputation (corporate tax) → tax payable (personal tax less

franking credit) → income after tax

▪ under imp: corporate pre tax profit – marginal personal rate of tax

- capital gain taxation and share holding period: depends on length of time share held

(less than 1 year tax based on marginal tax rate vs. more than 1 year tax based on

half marginal rate ie taxable component is halved) → gain on sale of share – capital

gain tax

find more resources at oneclass.com

find more resources at oneclass.com