ACCT1501 Lecture Notes - Lecture 12: Cost Driver, Variable Cost, Root Mean Square

18 May 2018

School

Department

Course

Professor

Thursday, 25 May 2017

Accounting & Financial Management 1A

Cost-Volume Profit Analysis

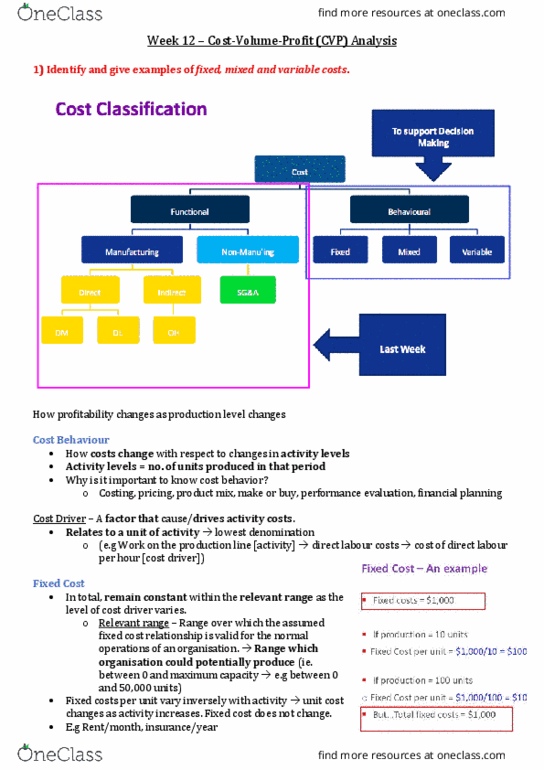

-Cost Behaviour: Deals with how costs change with respect to changes in activity

levels

•Essential for planning, control & decision making

-Cost Driver - factor that causes (drives) activity costs

-Fixed Cost: In total, remains constant within relevant range as level of cost driver

varies (e.g. rent per month, insurance per year)

•Relevant range - range over which assumed fixed cost relationship is valid for

normal operations of an organisation

•Fixed costs per unit vary inversely with activity → unit cost changes as level of cost

driver changes

-Variable Cost: In total, vary proportionally with changes in activity level

•Remain same on per unit basis

•Assumptions:

(i) Cost behaviour is defined with respect to a single, specific cost object/driver

(ii) Linearity

(iii) Specified time span (e.g. per month)

(iv) Changes in output volume are moderate (ie capacity)

-Semi-Fixed Cost: Some fixed costs do not fit the fixed cost classification completely

•Fixed over moderate range of activity, then rise or fall to new levels beyond that

range

-Semi-Variable Cost: Some variable costs do not fit variable cost classification

completely

•Although directly proportional to activity, have a fixed component

-CVP Analysis: Examines effect of changes in costs & volumes on a firm’s profits

•Factors considered: Volume of activity level, unit selling price, variable cost per unit,

total fixed cost, sales mix

•Assumptions:

!1

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Cost behaviour: deals with how costs change with respect to changes in activity levels: essential for planning, control & decision making. Cost driver - factor that causes (drives) activity costs. Semi-fixed cost: some xed costs do not t the xed cost classi cation completely: fixed over moderate range of activity, then rise or fall to new levels beyond that range. Semi-variable cost: some variable costs do not t variable cost classi cation completely: although directly proportional to activity, have a xed component. Cvp analysis: examines effect of changes in costs & volumes on a rm"s pro ts: factors considered: volume of activity level, unit selling price, variable cost per unit, total xed cost, sales mix, assumptions: Contribution margin: revenue - variable cost: contributes to meeting xed costs, contribution margin per unit = unit selling price - unit variable cost (s-v, contribution margin ratio = cm per unit unit selling price. Where cm ratio = total cm total sales revenue.