ACCT1501 Lecture Notes - Lecture 9: Management Accounting, Finished Good, External Auditor

ACCT1501 – Mgmt Accounting Kristy

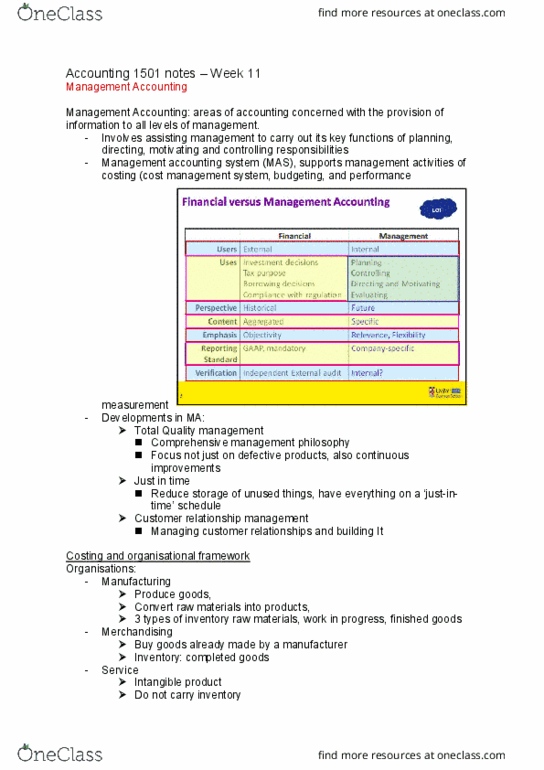

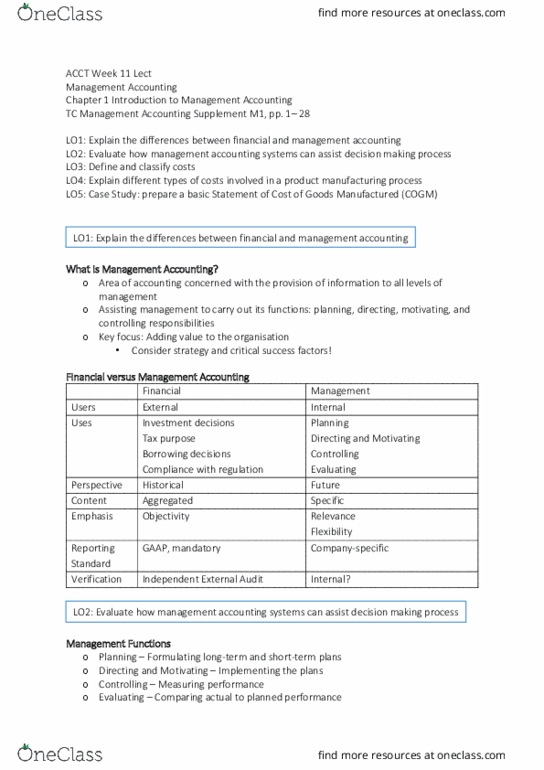

Management Accounting

- provision of information to all levels of management- internal (more forward looking), add value to

stakeholders

- assist management to carry out functions: planning, directing, motivating, controlling responsibilities

- manufacturing organisations produce goods by converting raw materials into physical product- hold 3 types of

inventory: raw materials, work in progress, finished goods inventories

→

COGS

- merchandising organisations buy goods already made (my manufacturers) and then sell them on to

consumers or to other merchandising orgs (retailers+wholesalers) (ready for sale)

- service organisations: manufac/merch- intangible rather than tangible (no inventory)- admin and

selling/marketing costs

Management Accounting System (MAS)

- supporting management activities

- costing- cost management system

- budgeting system

- performance measurement system (PMS)

- strategic and tactical decisions

- TQM: comprehensive management philosophy, focus is not just on defective products (cts improvement)

- flexible workforce, reduced set-up times, aim for zero-defects, improved plant layout, reliable suppliers

- benefits: reduced inventory costs, less warehouse space, greater customer satisfaction, higher quality products,

reduced rework costs

find more resources at oneclass.com

find more resources at oneclass.com

ACCT1501 – Mgmt Accounting Kristy

- Performance assessed across all four dimensions

- Measures are both quantitative and qualitative

- Measures are both backward and forward looking

- Mgmt. accounting doesn’t necessarily need to be audited by external auditor

common MC:

Basic cost concepts:

- Cost: cash or cash equivalent value sacrificed for g&s that are expected to bring a current or fut benefit to the

organisation

- COST

o Value sacrificed for g&s that are expected to bring a current/fut benefit (revenue) to the org

o Incurred to produce fut benefits

o As costs are used up in the production → expire

o Expired costs → expenses

o Unexpired costs → assets

- SUNK COST (main difference is timing)

o Has been paid and irretrievable and cannot be changed

- Differential cost- cost associated w different ways an organisation may achieve the same account

- Controllable costs- heavily influenced by a manager vs. non-controllable costs

- Direct: costs that can be traced to a cost object, in a convenient and cost-effective way

- Indirect: costs that are common to several cost objects (not directly traceable to any one particular cost obj)

- Allocate on percentage of production to factory- traceability depends on point of reference

o Decision making + performance evaluation

find more resources at oneclass.com

find more resources at oneclass.com

ACCT1501 – Mgmt Accounting Kristy

Functional classification of cost

- Relates to the way an organisation sets out its income statement

- Cost related to inventory/manufac → componenets of the COGS vs. admin (not COGS)- non-manufac cost

SG&A

- Manufacturing costs- costs incurred in process of converting raw materials into finished goods (D/ID)

Direct Manufacturing:

- Direct manufacturing costs: manufacturing costs directly traceable to product being converted from raw

materials into finished good

o Cost of raw materials (direct materials)

o Cost of labour (convert raw materials to finished product- direct labour)

Indirect:

- Indirect manufacturing costs: common to all products and cannot be economically and conveniently

associated w a particular cost object (ie manufacturing overhead)

- Depreciation on PPE, maintenance, supervision, material handling, utilities,

o indirect materials (necessary for production but not part of finished product + raw materials that form

insignificant part of finished)

o indirect labour

Non-manufacturing

- selling (marketing) and administrative costs

- Allocated to a cost object

Total manufacturing cost = DM + DL + OH

Cost concepts

- Period costs: expensed in period they occur (eg advertising, salaries)

- Product costs: manufacturing cost that are first inventories and later expensed as the goods are sold

o Expenses are capitalised- direct materials, direct labour, overhead

- Prime costs = direct materials + direct labour

- Conversion costs = direct labour + overhead (incurred in transformation of direct material into finished

product)

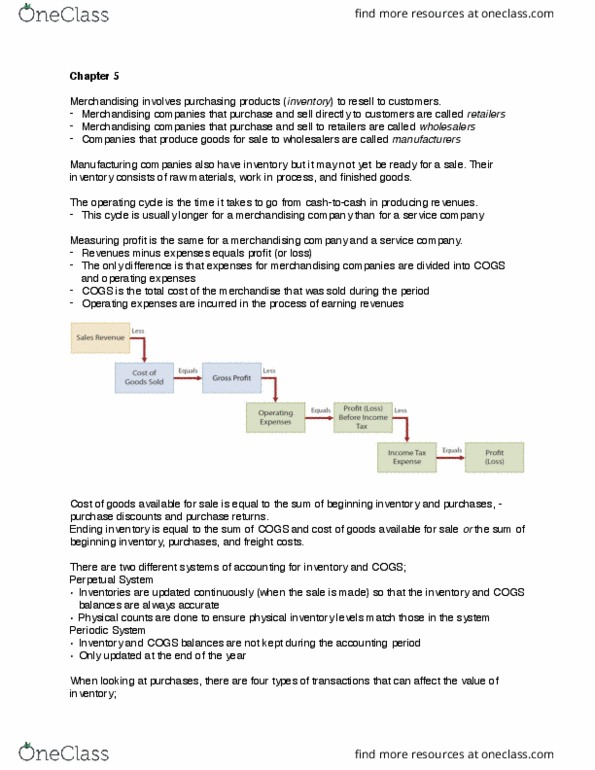

Financial Statements and the Functional Classification M1.10

Cost flows in a manufacturing organisation

- Absorption-costing profit: expenses (COGS+ operating) segregated according to function and then deducted

from revenues → profit before taxes

o COGS: beginning finished g inventory + COGS manufactured – ending finished g inventory = gross

profit – operating expenses (SGA) = profit before tax

o Costs of g manufactured- total cost of goods completed during period

- COGS = DM + DL + OH

- Work in progress: consists of all partially completed units found in production at a given PiT: beginning WiP

(manufacturing costs carried over from prior period)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Kristy provision of information to all levels of management- internal (more forward looking), add value to stakeholders assist management to carry out functions: planning, directing, motivating, controlling responsibilities. Manufacturing organisations produce goods by converting raw materials into physical product- hold 3 types of inventory: raw materials, work in progress, finished goods inventories cogs. Merchandising organisations buy goods already made (my manufacturers) and then sell them on to consumers or to other merchandising orgs (retailers+wholesalers) (ready for sale) service organisations: manufac/merch- intangible rather than tangible (no inventory)- admin and selling/marketing costs. Management accounting system (mas) supporting management activities costing- cost management system budgeting system performance measurement system (pms) strategic and tactical decisions. Tqm: comprehensive management philosophy, focus is not just on defective products (cts improvement) Flexible workforce, reduced set-up times, aim for zero-defects, improved plant layout, reliable suppliers. Benefits: reduced inventory costs, less warehouse space, greater customer satisfaction, higher quality products, reduced rework costs. Measures are both backward and forward looking.