ACC10007 Lecture Notes - Lecture 8: Opportunity Cost, Sunk Costs

Document Summary

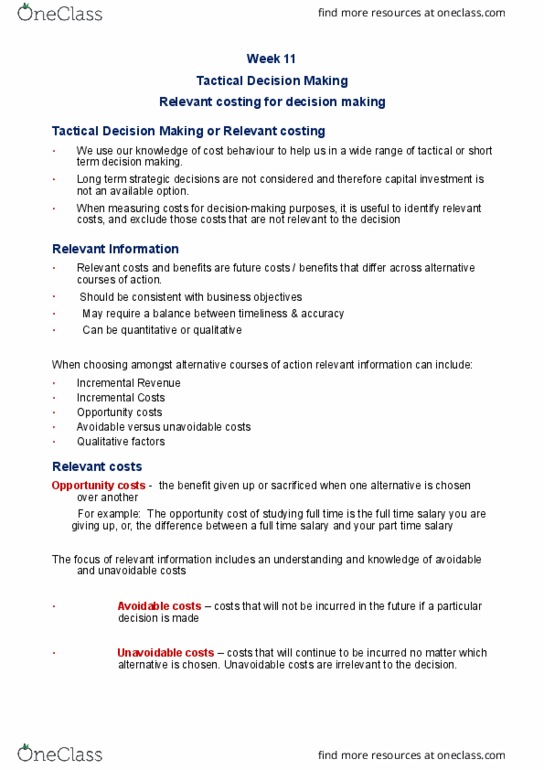

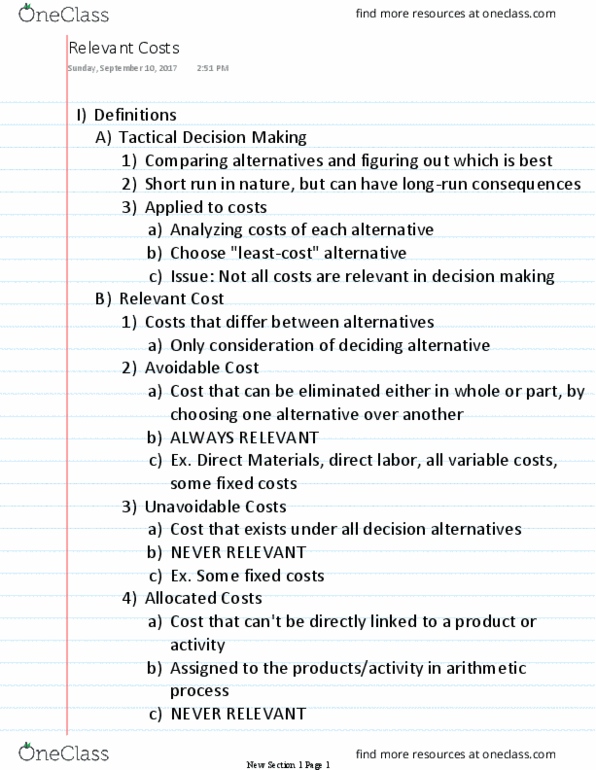

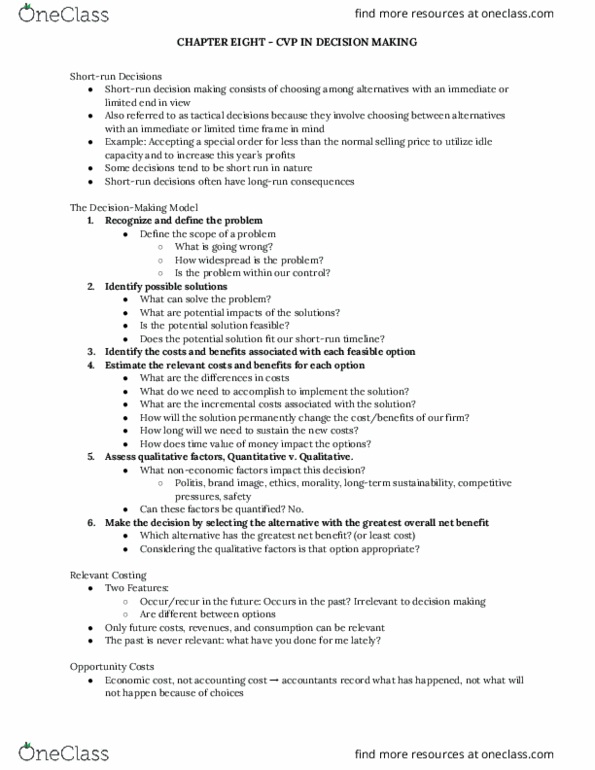

Relevant costing for decision making: we use our knowledge of cost behaviour to help us in a wide range of tactical or short term decision making. For decision making purposes, it makes sense to consider the relevant revenues and costs only, and exclude those that are not relevant to the decision. Tactical decision making involves choosing amongst alternatives with an immediate or limited end in view. The (cid:373)a(cid:374)age(cid:373)e(cid:374)t a(cid:272)(cid:272)ou(cid:374)ta(cid:374)t"s role i(cid:374) the de(cid:272)isio(cid:374)-making process is to provide relevant information to the decision makers. Tactical decision making: does not usually require significant increases or decreases in capacity-related resources. Tends to be short run in nature; though sr decisions can have lt implications. Tends to be able to be changed or reversed easily. Should (cid:271)e (cid:272)o(cid:374)siste(cid:374)t (cid:449)ith fir(cid:373)"s o(cid:448)erall lt o(cid:271)je(cid:272)ti(cid:448)es. Relevant costs and benefits are future costs / benefits that differ across alternative courses of action. May require a balance between timeliness & accuracy.