ACC10007 Lecture Notes - Lecture 10: Variable Cost, Fixed Cost

Accounting for Decision Making Lecture 10

Cost Volume Profit Analysis

Cost Behavior pattern

Cost behaviour is the relationship between a cost and the level of activity

Consider

Variable costs

Fixed costs

Step-fixed costs

Semi-variable costs

Understanding cost behaviour can assist with cost estimation

Estimating costs

Y = mX + c

Where Y = estimated total cost

m = variable cost per unit of activity (the slope of the line)

X = the level of activity (volume)

c = fixed cost component (the intercept on the vertical axis)

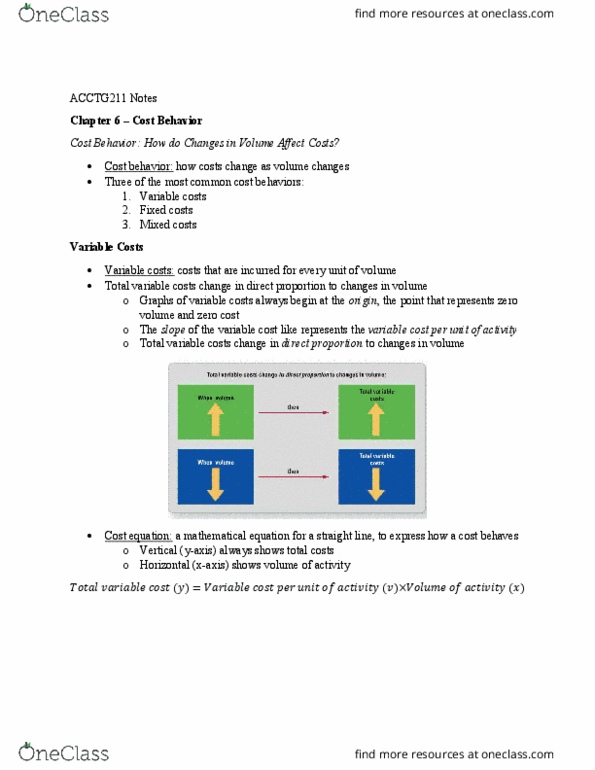

Variable Costs

Total Variable costs change in direct proportion to changes in the level of activity.

Variable cost per unit remains constant regardless of the level of activity

The variable cost per unit is the slope (m) of the cost line in the following cost function:

Y = mX + c

Variable costs can be depicted as a linear straight line

!!!!!!!

Variable cost per unit remains constant at $100

Total variable cost varies with volume

Fixed costs

As activity increases or decreases total fixed costs stay constant

As activity level changes the allocated fixed cost per unit changes

The fixed cost is the vertical axis intercept (c) of the cost line in the following cost

function:

Y = mX + c

Note: Fixed cost per unit is often calculated to use in product costing but is of limited use

in other management decision making. Fixed costs do not vary with the level of

activity within the relevant range

Semi-variable costs have both fixed and variable elements

Stepped fixed costs remain fixed over a range of activity levels but jump to a different amount

for levels outside that range

Cost Behavior Examples

Variable cost - Raw Materials - driven by production volume. Total variable cost varies

directly in proportion to changes in the level of production volume

Fixed cost - Lease of Premises – total fixed cost is constant regardless of changes in

activity levels

Semi-variable cost - Operating Delivery Trucks – fixed lease cost plus running costs

(eg petrol used per km travelled)

Cost behavior or relevant Range

Relevant Range

The range of activity over which a particular cost behaviour pattern can be assumed to be valid

Outside the relevant range of activity, the expected behaviour of costs may change

Cost Volume Profit

Understanding the relationship between Cost, Volume & Profit can improve decision making

CVP Analysis

For short-term operating decisions, managers may need to answers questions like:

How many units do we need to sell to breakeven?

If we want to make a profit of $X, how many units would we need to sell?

What is the impact of a given increase or decrease in variable and/or fixed costs on breakeven

point?

What is the impact of a given increase or decrease in price on profit?

For CVP analysis, which can be used to answer these questions, we make assumptions about

how costs behave in a business

Terminology and Abbreviations

CM = Contribution Margin

SP = Selling Price

VC = Variable Cost

FC = Fixed Cost

$pu = $ Per Unit

B/e = Breakeven

PBT = Profit before tax

T = Total SR = Sales Revenue

FORMULAS

Contribution Margin $per unit

= Selling Price – Variable Cost $pu

CM = SP - VC

Contribution Margin Ratio

= Contribution Margin / Selling Price

CM ratio = CM / SP

Breakeven in units

= Fixed Costs / Contribution Margin $per unit

B/e (units) = FC / CM $pu

Breakeven in sales dollars

= Fixed Costs / Contribution Ratio

B/e (sales $) = FC / CM ratio

Units to earn a Target Profit

= (Fixed Costs + Target Profit before tax)/CM per unit

(FC + Target PBT) / CM

Document Summary

Cost behaviour is the relationship between a cost and the level of activity. Understanding cost behaviour can assist with cost estimation. Where y = estimated total cost m = variable cost per unit of activity (the slope of the line) X = the level of activity (volume) c = fixed cost component (the intercept on the vertical axis) Total variable costs change in direct proportion to changes in the level of activity. Variable cost per unit remains constant regardless of the level of activity. The variable cost per unit is the slope (m) of the cost line in the following cost function: Variable costs can be depicted as a linear straight line. Variable cost per unit remains constant at . As activity increases or decreases total fixed costs stay constant. As activity level changes the allocated fixed cost per unit changes. The fixed cost is the vertical axis intercept (c) of the cost line in the following cost function: