ACC10007 Lecture Notes - Lecture 4: Deferral, Jb Hi-Fi, Trend Analysis

The Cash Flow Statement!

!

Chapter 7!

!

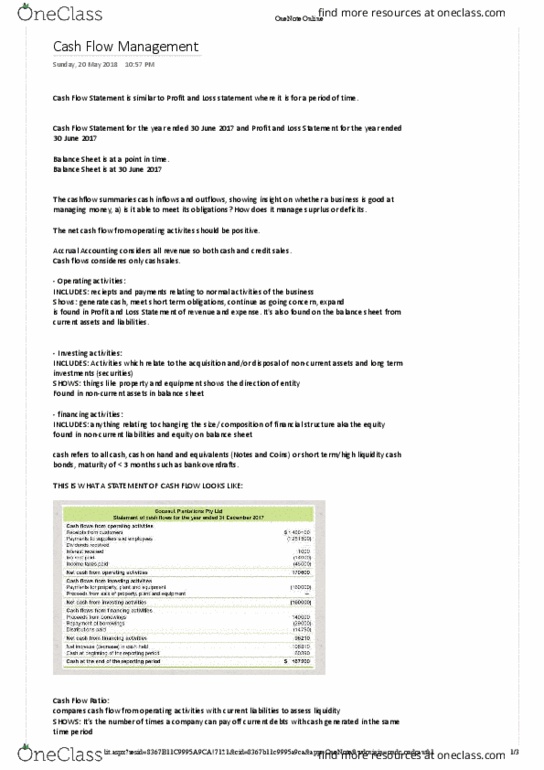

Statement of cash flows

Financial Statements

•Balance Sheet is as at a point in time (snapshot of a company during a particular date

in time)

e.g. Balance Sheet as at 30 June 2017

•

•Profit or Loss Statement is for a period of time (a listing of what has transpired or

happened during a time period)

e.g. Profit or Loss Statement for year ended 30 June 2017

• Cash Flow Statement is for a period of time

e.g. Cash Flow Statement for year ended 30 June 2017

The Purpose and Usefulness of a Cash Flow Statement

Cash flows are the lifeblood of a business.

The Cash Flow Statement summarises cash inflows and cash outflows for a particular

period of time. It is prepared on a cash basis.

Working capital is the difference between current assets (e.g. cash) and current

liabilities (e.g. Accounts payable). It is necessary to fund day to day operations

It can provide insight into whether the business is good at managing its money,

including

➢Is it able to meet its financial obligations when they fall due?

➢How does it manage surpluses and / or deficits?

The flow of cash within the business cycle.

For an entity to survive, the net cash flows from

operating activities should be positive.

Difference between cash and accrual accounting

–The accrual system focuses on when (Revenue and expense recognition

principles) a transaction takes place.

–In contrast, the Cash Flow Statement is concerned with cash receipts and

payments, rather than the timing of the underlying transaction.

–There can be a significant difference between an entity’s cash position and its

profit.

Example of Revenue recognition

An accountant provides tax advice to a client for a fee of $1000. S/ He can recognise the

revenue immediately upon completion of the service, even if s/he does not expect

payment from the customer for weeks.

Example of Expense recognition

A variation on the example is, this Accountant receives $1,000 in advance to help a client

throughout the year. In this case, the Accountant should recognise an increment of the

advance payment in each of the twelve months covered by the agreement, to reflect the

pace at which it is earning the payment.

The Cash Flow Statement

Difference between cash and accrual accounting

The Purpose and Usefulness of a Cash Flow Statement

The Cash Flow Statement gives additional information to the Balance Sheet and

Profit or Loss Statement. It assists decision makers in assessing an entity’s ability to:

• generate cash flows

• meet financial commitments as they fall due

• fund changes in scope and/or nature of activities

• obtain external finance.

Format of the Cash Flow Statement

Cash refers to all cash, cash on hand and cash equivalents:

–Notes and coins held.

–Deposit call accounts at financial institutions.

–Cash equivalents:

• Short term, highly liquid investments (treasury bonds), easily converted to

known amounts of cash with little risk of a change in value. This includes

investments with maturity ≤ 3 months and bank overdrafts.

Classified into 3 main sections reflecting major cash flow activities:

1. Operating activities:

Include receipts and payments relating to the normal activities of the business

2. Investing activities:

Activities which relate to the acquisition and/or disposal of non-current assets,

and longer term investments (e.g. securities)

3. Financing activities:

Activities which relate to changing the size and/or composition of the financial

structure of the entity (e.g. equity), and longer term borrowings

Operating activities:

Cash flow from operating activities shows ability to:

• generate cash

• meet short term obligations

• continue as a going concern

• expand

Relationship of the statement of cash flows to

other financial statements:

–Classified into three main sections reflecting

the major cash flow activities:

•

• operating activities

•

• investing activities

•

• financing activities.

Profit or Loss

statement

revenue and

expenses;

Non-

current assets in the

Non-current liabilities and equity in the balance sheet

Document Summary

Cash flows are the lifeblood of a business. The cash flow statement summarises cash inflows and cash outflows for a particular period of time. Working capital is the difference between current assets (e. g. cash) and current liabilities (e. g. accounts payable). It is necessary to fund day to day operations. It can provide insight into whether the business is good at managing its money, including. The flow of cash within the business cycle. For an entity to survive, the net cash flows from operating activities should be positive. The accrual system focuses on when (revenue and expense recognition principles) a transaction takes place. In contrast, the cash flow statement is concerned with cash receipts and payments, rather than the timing of the underlying transaction. There can be a significant difference between an entity"s cash position and its profit. An accountant provides tax advice to a client for a fee of .