EFB210 Lecture Notes - Lecture 7: Central Moment, Random Variable, Elizabeth Daily

Week 7 Finance 1 Lecture Notes

Introduction to Statistics for Finance

Measuring investment Returns

• Introduction

o Future earnings are uncertain for most investments; therefore, most

investments are risky

o Can we use past price data to understand regularities in the behavior of stock

prices?

o We cannot tell what the future price will be exactly because the outcome is

uncertain.

o However, we can gain an idea about the likelihood of particular outcomes

from past outcomes.

o To do this, we need find a repetitive pattern in the probability distributions

based on price information.

Prices and Returns

• Can we expect that the prices which the

shares took in the past will again be

realised?

• No! in fact, we expect share prices, in the

long-run, to grow, i.e. to move into higher

price regions.

o Can be referred to as a random walk

plus drift

• What about returns?

(= % price changes)

• It appears that share price returns behave in the same

manner through time.

o Outcomes still random, but constant distribution

▪ Mean

▪ Variance

find more resources at oneclass.com

find more resources at oneclass.com

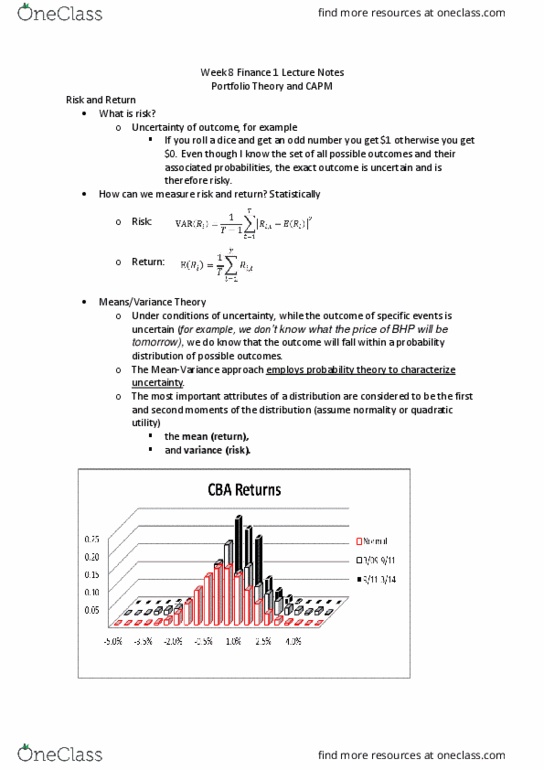

Distributions

• Comparison of price and return distributions across securities

o Price distributions: shape, central moment and variance tend to vary across

securities

o Return distributions: shape, central moment and variance may display some

minor variations, but generally shape appears the same across securities

• Comparison of price and return distributions across time

o Price distributions: shape, central moment and variance tend to vary across

time (random walk)

o Return distributions: shape, central moment and variance may display some

sample variations, but can assume they are same across time

• Describing one investment / random variable

o Share Price Returns behave in a regular fashion across time and across

investments, share prices do not.

o Convenient result, since it is the investment returns we are interested in

rather than price levels. Even if we wanted the price levels, the returns allow

us to go back to the price level anyway.

o Moreover, we can approximate the distribution of returns with the Normal

Distribution

▪ Normal Distribution is characterised by two parameters: mean &

variance

▪ If returns display constant behaviour through time, we can use past

return data to calculate means (average returns) and variances of

returns.

▪ Using this information one can make statements like:

• There is a 5% proailit to eperiee a loss of 7% or ore

i the et oth.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Even if we wanted the price levels, the returns allow us to go back to the price level anyway: moreover, we can approximate the distribution of returns with the normal. Distribution: normal distribution is characterised by two parameters: mean & variance. Prices and returns: summary, prices, specific outcome unknown, distributions vary across security and time, returns, specific outcome unknown, distributions display similar characteristics across security and time that is similar to a normal distribution. If we assume that returns do follow a normal distribution and the shape of distribution is constant through time, we only need to measure the mean and variance of returns to fully describe the distribution. It was established earlier, that we can gauge the parameters of return distributions from historical return data: the same formula applies for returns of different frequencies (e. g. daily, weekly, annual etc.