AYB340 Lecture Notes - Lecture 10: New Zealand Dollar, Local Currency, Financial Statement

Document Summary

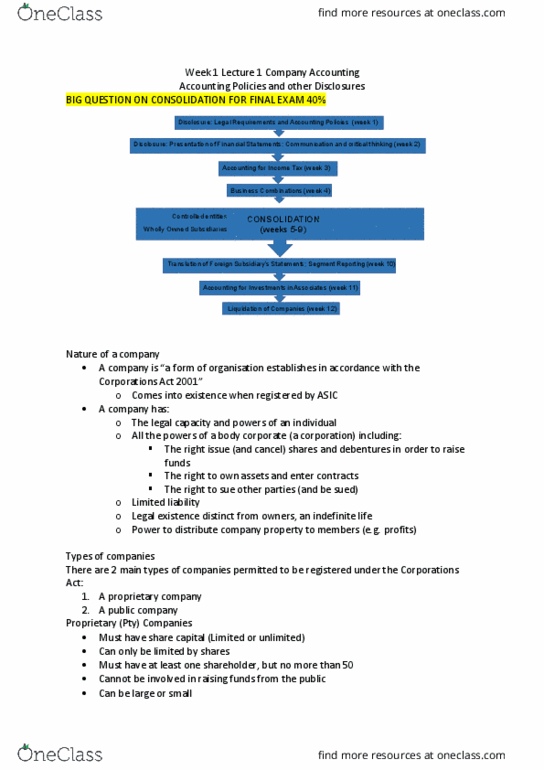

Translation of a foreign subsidiary"s financial statements & segment reporting. Learning objective 1 purpose of translating: many companies in australia have operations in australia as well as in overseas locations, two issues that such companies have to face are, 1. What currency will be used for accounting in the overseas location itself: 2. Aasb 121 the effects of changes in foreign exchange. In order to understand these processes, it is necessary to distinguish between three different types of currency: 1. Local currency: the currency of the country in which the foreign operation is based, 2. Functional currency: the currency of the primary economic environment in which the entity operates, note: a foreign currency is a currency other than the functional currency of an entity, 3. Presentation currency: the currency in which the financial statements are presented, note: financial statements may be presented in any currency.