ACF2100 Lecture Notes - Lecture 10: Classification Rule, Financial Instrument, Interest Expense

3 Aug 2018

School

Department

Course

Professor

Document Summary

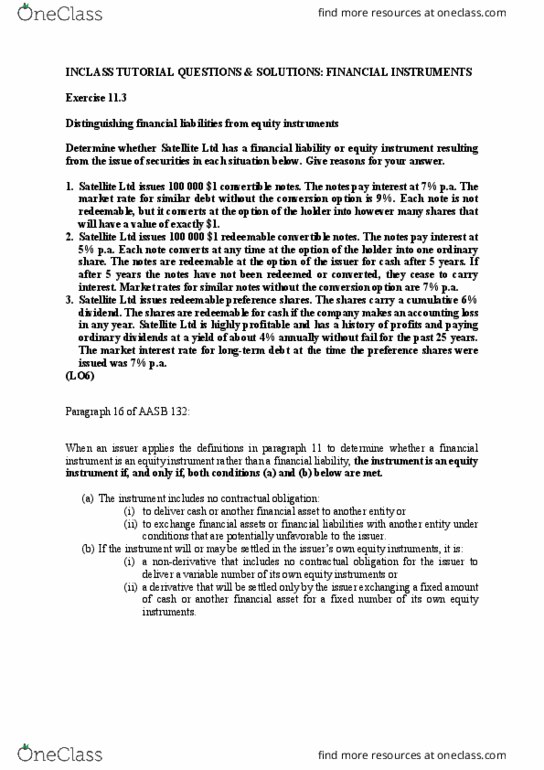

A financial instruments is any contract that gives rise to financial asset of one entity and a financial liability or equity instrument of another entity. Aasb 9 financial instruments (1 january 2018) Aasb 121 the effect of changes in foreign exchanges rates. Issuer of instrument determines to recognise the instrument as a liability or equity (i. e preference shares) in some cases may be partly debt & partly equity (i. e convertible notes) Holding everything equal, managers prefer to disclose financial instruments as equity rather than debt: Critical questions in differentiating a liability from equity: The value of primary financial instruments is determined directly by markets (i. e share). A derivative financial instrument derives its value from the value of some other financial asset or variable. E. g. , share options derives its value from the value of a share. A derivative could be used for hedging or speclation purposes. Derivative vaalues rises and falls in accordance with the value of the underlying asset.