ACCG101 Lecture 7: ACCOUNTING 100 - financial statements

30 May 2018

School

Department

Course

Professor

Week 7 Preparing Financial Statements

Users of Financial Statements

1. Financial performance

- Information about the ability of the entity to utilise its assets effectively and

efficiently e.g. profitable?

2. Financial position

- Information about the financial resources controlled by the entity

- Information about the entity’s financial structure

- E.g. liability?

3. Cash movements

- Information about the entity’s ability to generate cash flows

- E.g. cash inflow vs outflow

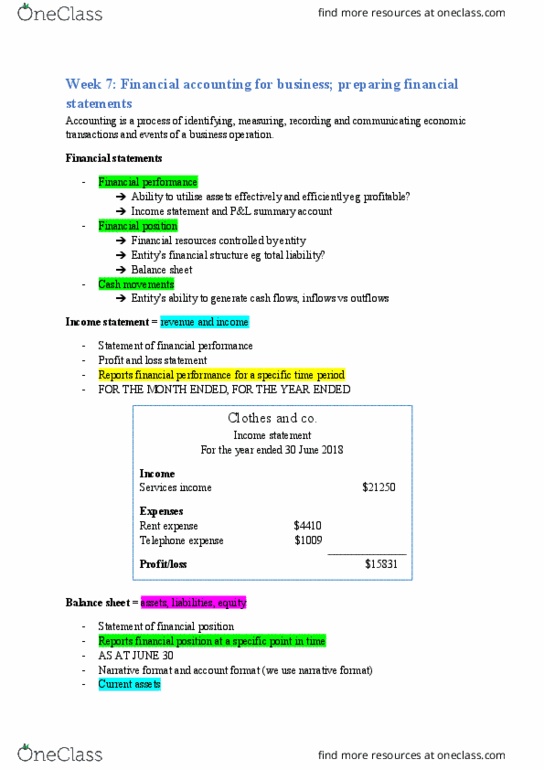

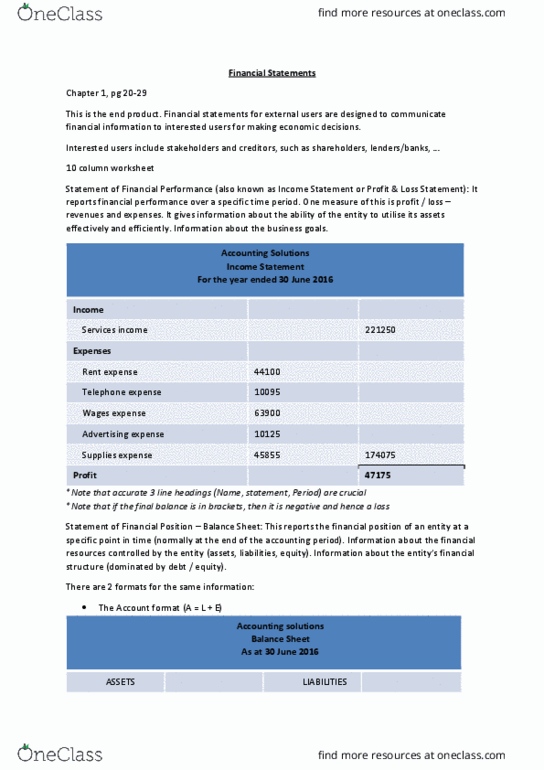

Income Statement

As known as:

- Statement of financial performance

- Profit and loss statement

- Reports financial performance for a specific time period e.g. monthly, yearly

- Shows income and expenses

- Income > expenses = profit

- Income < expenses = loss

Balance Sheet

Also known as:

- Statement of financial position

- Reports financial position at a specific point in time

- Shows assets, liabilities and equities

- Represents the accounting equation (assets = liabilities + equity)

- Two alternatives are

- Narrative format (vertical) and account format (horizontal)

Document Summary

Information about the financial resources controlled by the entity. Information about the entity"s financial structure: financial position. Information about the entity"s ability to generate cash flows. Reports financial performance for a specific time period e. g. monthly, yearly. Reports financial position at a specific point in time. Represents the accounting equation (assets = liabilities + equity) Narrative format (vertical) and account format (horizontal) Assets and liabilities are classified as current and non-current. Current assets: expected to be sold, converted to cash or consumed. Non-current assets: expected to last longer than 12 months. Current liabilities: obligations that are expected to be settled within 12 months. E. g. accounts payable, salary payable, rent payable. Non-current liabilities: all liabilities that aren"t needed now. Reports the changes that took place in equity during the period. Shows the opening balance, the movement and the ending balance. The opening balance should match with the ending balance of equity.