ACCG101 Lecture Notes - Lecture 10: Fixed Cost, Variable Cost

30 May 2018

School

Department

Course

Professor

Week 10 Cost Volume Profit Analysis

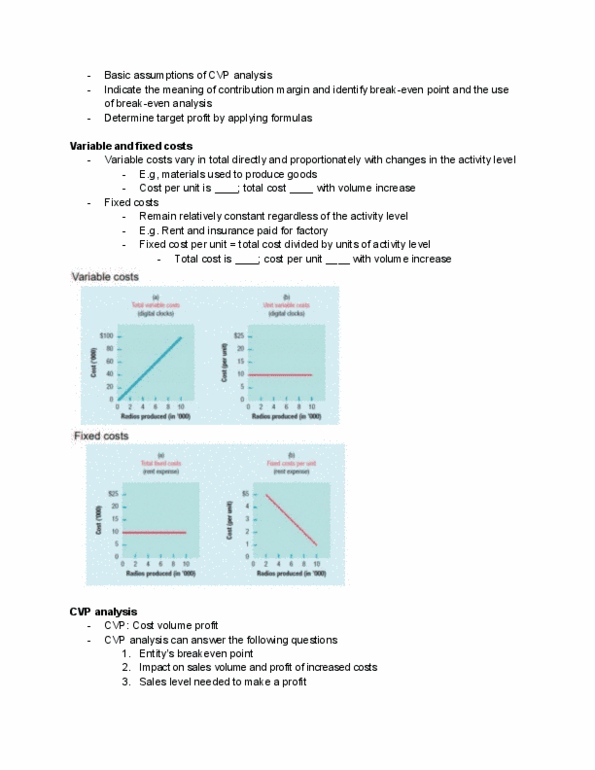

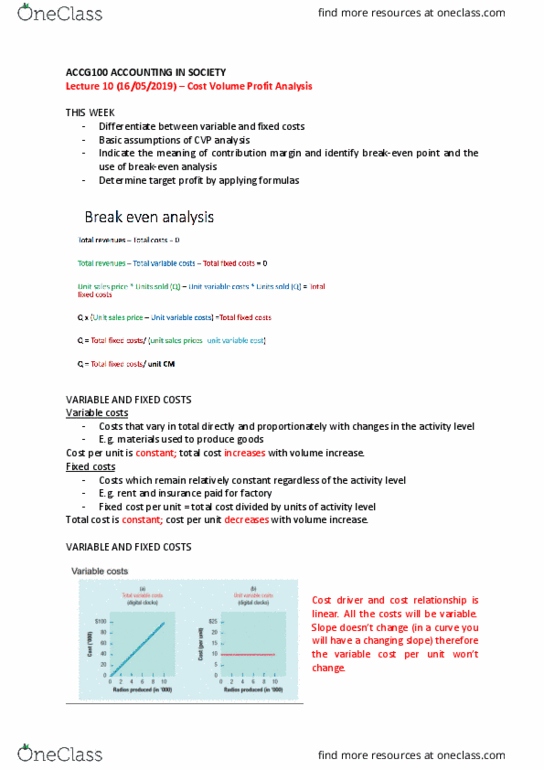

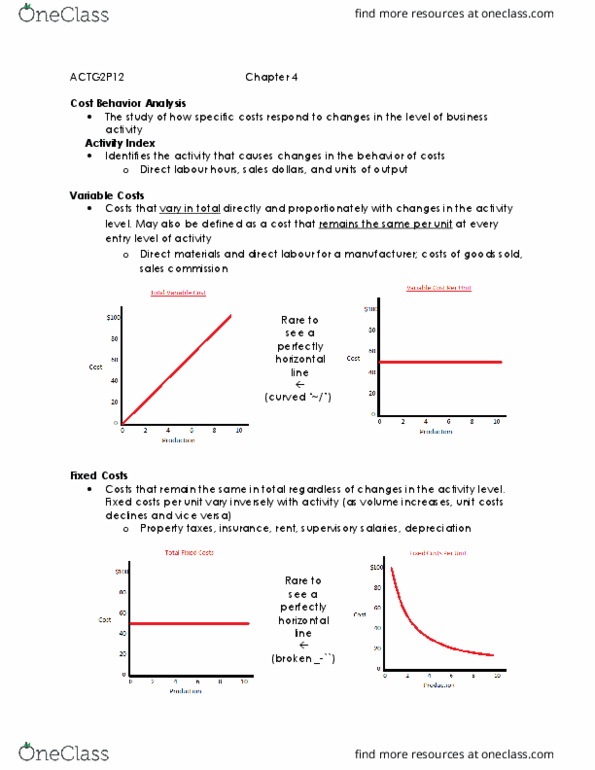

Variable Costs

- Costs that vary in total directly and proportionately with changes in the activity

level

- Includes direct materials, direct labour, cost of sales, commission and fuel

- E.g. materials used to produce goods

- Cost per unit is constant; total cost increases with volume increase

Fixed Costs

- Costs which remain relatively constant regardless of the activity level

- Includes rates of taxes, insurance, salaries, depreciation

- E.g. rent and insurance paid

- Fixed cost per unit = total cost divided by units of activity level

- Total cost is constant’ cost per unit decreases with volume increase

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Costs that vary in total directly and proportionately with changes in the activity level. Includes direct materials, direct labour, cost of sales, commission and fuel. Cost per unit is constant; total cost increases with volume increase. Costs which remain relatively constant regardless of the activity level. Fixed cost per unit = total cost divided by units of activity level. Total cost is constant" cost per unit decreases with volume increase. Cost volume profit can answer: the entity"s breakeven point, impact on sales volume and profit of increased costs, sales level needed to make a profit, impact of changes in selling price. Basic assumptions: costs and revenue are linear within the relevant range, all costs are identifiable as variable or fixed, costs are affected only be changes in activity level, all units produced are sold. Cm = the amount of revenue remaining after deducting variable costs. Can be expressed as a total amount or an a per-unit basis.